Chiến lược giao dịch RSI MA Crossover Swing với hệ thống Trailing Stop

2

Follow

480

Followers

Tổng quan

Chiến lược này là một chiến lược giao dịch dao động dựa trên RSI (chỉ số tương đối mạnh) và đường trung bình di chuyển của nó (MA), được thiết kế cho biểu đồ 4 giờ. Chiến lược này tạo ra tín hiệu giao dịch thông qua RSI và MA và kết hợp với nhiều công cụ quản lý rủi ro, bao gồm thiết lập dừng / dừng, theo dõi dừng và đảo ngược cơ chế thoát.

Nguyên tắc chiến lược

- Hạn chế khung thời gianChiến lược chỉ hoạt động trên biểu đồ 4 giờ, đảm bảo tín hiệu giao dịch phù hợp với chu kỳ thời gian được thiết kế.

- Tính toán chỉ số: Sử dụng RSI ((đường dài mặc định 14) và đường trung bình di chuyển của nó ((SMA hoặc EMA, chiều dài mặc định 14) để tạo tín hiệu.

- Gold Forks (MA trên RSI) kích hoạt tín hiệu mua (thực hiện nhiều hơn).

- Đĩa chết ((RSI dưới MA) kích hoạt tín hiệu bán ((đóng trống) }}.

- Quản lý vị tríKích thước của vị thế dựa trên phân bổ vốn cho mỗi giao dịch và giá hiện tại.

- Cơ chế rút lui:

- Đặt dừng / dừngLưu ý: Stop Loss (bằng mặc định là 1.5%) và Stop Loss (bằng mặc định là 2.5%) dựa trên phần trăm.

- Theo dõi lỗ hổng: Khi giá từ điểm cao nhất quay trở lại một số điểm đã chỉ định (mặc định là 10 điểm) thì kích hoạt thoát.

- Quay lạiCác nhà đầu tư khác cũng đã đưa ra các thông báo về việc có thể xảy ra sự cố.

- Kiểm soát rủi ro:

- Sau hai lần thua lỗ liên tiếp, tạm dừng giao dịch và đặt lại số lỗ mỗi ngày vào lúc 9:15.

Phân tích lợi thế

- Xác nhận tín hiệu đa chiều: Kết hợp RSI và MA để giảm tín hiệu giả.

- Quản lý rủi ro động: Theo dõi dừng lỗ khóa lợi nhuận, dừng lỗ cố định hạn chế lỗ.

- Quản lý tài chính nghiêm ngặtLưu ý: Không sử dụng quá nhiều đòn bẩy dựa trên vị trí phân bổ vốn.

- Kiểm soát kỷ luậtCác nhà giao dịch đã đưa ra một kế hoạch để ngăn chặn các giao dịch cảm xúc.

- Hình ảnh đánh dấu: Biểu đồ đánh dấu rõ ràng giúp nhận ra nhanh chóng các tín hiệu và điểm thoát.

Phân tích rủi ro

- Độ nhạy tham số: RSI và MA có ảnh hưởng lớn đến chất lượng tín hiệu, cần tối ưu hóa để thích ứng với biến động của thị trường.

- Xu hướng thị trườngTrong một xu hướng mạnh, RSI có thể bị quá mua / quá bán trong một thời gian dài, dẫn đến tín hiệu bị tụt hậu.

- Hạn chế khung thời gian: Chỉ áp dụng cho biểu đồ 4 giờ, các chu kỳ khác cần xác nhận lại.

- Rủi ro mất mát liên tụcMột số nhà đầu tư cho rằng, nếu các nhà đầu tư có thể bỏ lỡ cơ hội kiếm lợi nhuận tiềm năng trước khi đặt lại kế toán lỗ.

Giải pháp:

- Các tham số tối ưu hóa thông qua lịch sử.

- Kết hợp các chỉ số xu hướng (ví dụ như ADX) để lọc tín hiệu.

- Thiết lập giá trị giảm số lỗ động.

Hướng tối ưu hóa

- Tích hợp đa chỉ sốGhi chú: Ghi chú MACD hoặc Brin Band tăng cường tín hiệu xác nhận.

- Điều chỉnh tham số động: Điều chỉnh độ dài RSI và tỷ lệ dừng lỗ tùy theo biến động của thị trường.

- Mở rộng khung thời gian: Chiến lược thử nghiệm hoạt động trong chu kỳ cao hơn hoặc thấp hơn (như mặt trời / 1 giờ).

- Tối ưu hóa học máy: Sử dụng mô hình đào tạo dữ liệu lịch sử để tối ưu hóa điều kiện nhập học và xuất học.

- Tăng cường quản lý tài chính: Điều chỉnh tỷ lệ vốn mỗi giao dịch theo giá trị ròng của tài khoản.

Tóm tắt

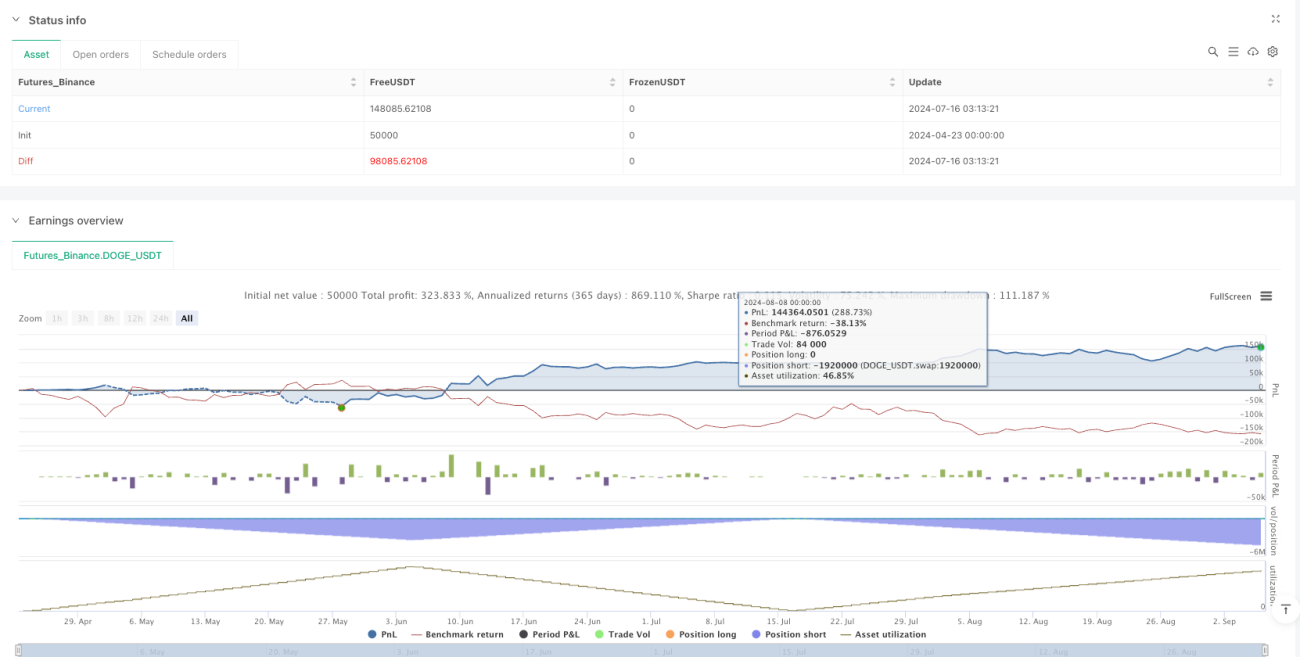

Chiến lược này cho phép giao dịch dao động thông qua tín hiệu chéo giữa RSI và MA, kết hợp với các công cụ quản lý rủi ro nhiều cấp, cân bằng tiềm năng lợi nhuận và kiểm soát rủi ro. Ưu điểm của nó là logic rõ ràng và kỷ luật nghiêm ngặt, nhưng cần được tối ưu hóa hơn nữa để thích ứng với các môi trường thị trường khác nhau.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1