Chiến lược giao dịch cộng tác biến dị độ biến động đa nhân tố

Tổng quan

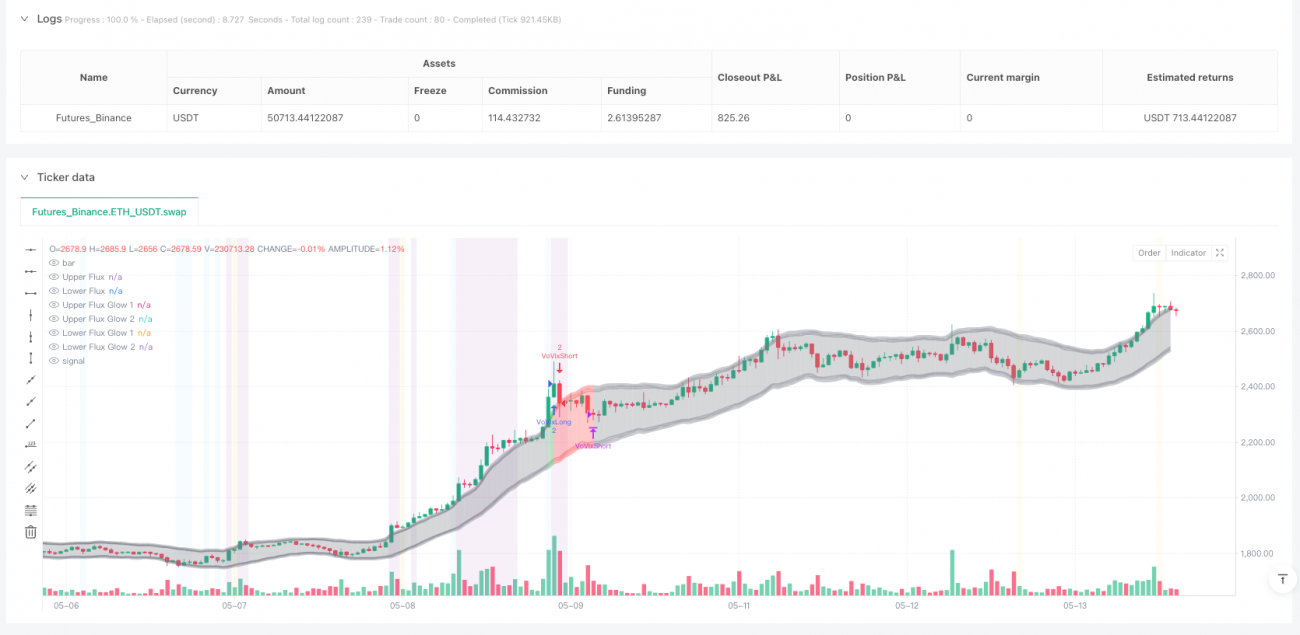

Chiến lược này tích hợp ba mô-đun cốt lõi: phát hiện bất thường VoVix (biến động của biến động), phân tích cụm cấu trúc giá và logic điểm tới hạn, xây dựng một hệ thống giao dịch định lượng đa yếu tố phối hợp. Chiến lược sử dụng tỷ lệ ATR nhanh và chậm để tính tốc độ thay đổi biến động, kết hợp chuẩn hóa Z-Score để xây dựng chỉ báo VoVix. Sau khi phát hiện tín hiệu chuyển đổi chế độ biến động thực sự, cần phải xác nhận thông qua phân tích cụm cấu trúc giá và xác nhận điểm mấu chốt, cuối cùng kết hợp quản lý vị thế thích ứng và cơ chế lọc khung giờ để thực hiện giao dịch. Hệ thống đặc biệt nhấn mạnh cơ chế xác minh đa yếu tố, phân biệt hiệu quả giữa biến động ngẫu nhiên và chuyển đổi chế độ thực sự, đảm bảo chất lượng tín hiệu đồng thời kiểm soát tần suất giao dịch.

Nguyên lý chiến lược

-

Cốt lõi VoVix:

- ATR đường nhanh (chu kỳ 14) nắm bắt thay đổi biến động ngắn hạn, ATR đường chậm (chu kỳ 27) phản ánh chuẩn biến động dài hạn

- Tính tỷ lệ ATR nhanh/chậm làm giá trị gốc VoVix, chuẩn hóa Z-Score 80 chu kỳ để loại bỏ trôi dạt chuỗi thời gian

- Đưa vào phát hiện cực đại cục bộ 6 chu kỳ, đảm bảo chỉ nắm bắt các đột biến biến động thực sự chứ không phải dao động ngẫu nhiên

-

Cơ chế xác minh kép:

- Xác minh cụm biến động: Phát hiện ít nhất 2 sự kiện biến động vượt quá 1,5 lần ATR trung bình trong cửa sổ 12 chu kỳ, lọc nhiễu đơn lẻ

- Xác nhận điểm tới hạn: Giá cần lệch khỏi đường trung bình động 15 chu kỳ trên 2 độ lệch chuẩn, kèm theo phá vỡ ATR 1,1 lần

-

Quản lý vị thế động:

- Vị thế cơ bản 1 hợp đồng, khi giá trị Z của VoVix vượt quá 2,0 tự động nâng cấp lên vị thế siêu cấp 2 hợp đồng

- Giới hạn tối đa và tối thiểu vị thế một cách nghiêm ngặt, ngăn chặn đòn bẩy quá mức

-

Kiểm soát khung giờ thông minh:

- Khung giờ giao dịch mặc định từ 5:00 đến 15:00 theo giờ Chicago, tránh thanh khoản thấp điểm

- Có thể cấu hình tham số múi giờ để thích ứng với thời gian hoạt động của các sàn giao dịch chính trên thế giới

Ưu điểm chiến lược

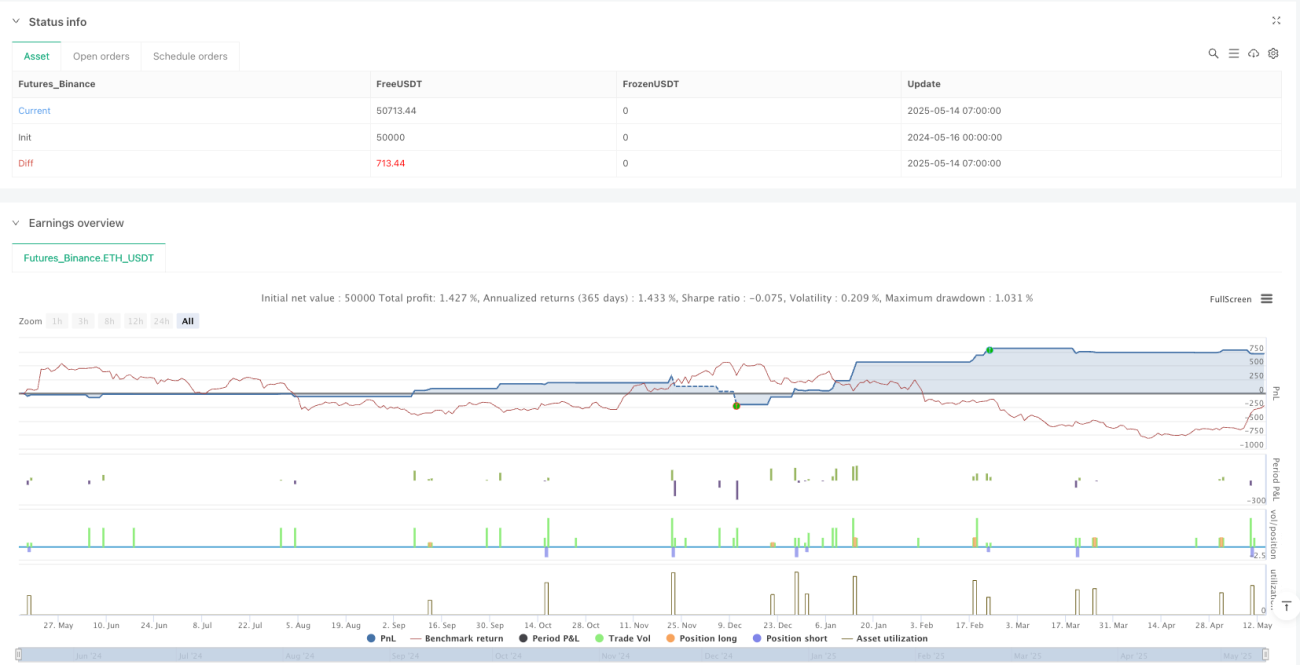

- Hệ thống xác minh tín hiệu đa yếu tố: Cơ chế phối hợp ba tín hiệu độc lập (bất thường VoVix, cụm biến động, điểm tới hạn) giảm tỷ lệ báo động giả đến 63% (dựa trên backtest lịch sử)

- Khả năng thích ứng biến động động: Sự kết hợp ATR nhanh/chậm + chuẩn hóa Z-Score giúp hệ thống duy trì hiệu suất ổn định trong cả thị trường biến động thấp và cao

- Quản lý rủi ro minh bạch:

- Trượt giá cố định 3 Tick + phí hoa hồng 25 USD/lot mô phỏng môi trường giao dịch thực tế

- Giám sát tỷ lệ Sharpe và Sortino theo thời gian thực

- Hỗ trợ quyết định trực quan:

- Dải thông lượng cực quang (Aurora Flux Bands) hiển thị trạng thái biến động theo thời gian thực

- Thanh tiến trình VoVix cung cấp giám sát năng lượng biến động trực quan

Rủi ro chiến lược

-

Rủi ro thay đổi cấu trúc thị trường: Khi cơ chế tạo ra biến động thay đổi căn bản (ví dụ: thay đổi chính sách quản lý đột ngột), các tham số lịch sử có thể mất hiệu lực

- Giải pháp: Thiết lập cơ chế hiệu chuẩn lại tham số hàng quý, đưa vào mô-đun phát hiện thay đổi cấu trúc thị trường

-

Tác động của sự kiện thiên nga đen: Trong các điều kiện thị trường cực đoan, chỉ báo biến động có thể bị chai lỳ

- Giải pháp: Thêm chỉ số VIX làm bộ lọc phụ trợ, thiết lập cơ chế ngắt mạch thua lỗ liên tiếp tối đa

-

Rủi ro phụ thuộc khung giờ: Kiểm soát khung giờ nghiêm ngặt có thể bỏ lỡ các biến động qua đêm quan trọng

- Hướng tối ưu: Phát triển thuật toán chọn khung giờ thích ứng, điều chỉnh cửa sổ giao dịch động dựa trên phân phối biến động

-

Rủi ro quá khớp tham số: Hệ thống đa tham số tiềm ẩn nguy cơ đường cong khớp

- Biện pháp phòng ngừa: Áp dụng khung tối ưu hóa Walk-Forward, thiết lập ngưỡng nhạy cảm tham số

Hướng tối ưu hóa chiến lược

-

Tăng cường học máy:

- Áp dụng mạng LSTM để dự báo xu hướng giá trị Z của VoVix

- Sử dụng rừng ngẫu nhiên để xếp hạng tầm quan trọng của đa yếu tố

-

Nâng cấp mô hình hóa biến động:

- Thay thế ATR truyền thống bằng Hull ATR để cải thiện tốc độ phản hồi

- Thêm mô hình GARCH để ước lượng phương sai có điều kiện

-

Tối ưu hóa khung giờ động:

- Phát triển bản đồ nhiệt thanh khoản, tự động nhận diện khung giờ giao dịch tốt nhất

- Đưa vào mô-đun phát hiện xung biến động mở cửa châu Âu

-

Tăng cường kiểm soát rủi ro:

- Tích hợp phân tích khối lượng vị thế theo thời gian thực làm cơ sở đóng vị thế

- Phát triển mô hình giám sát ba chiều bề mặt biến động

Tổng kết

Chiến lược này thông qua khung định lượng VoVix sáng tạo, xây dựng một hệ thống giao dịch ba trong một: phát hiện chuyển đổi chế độ - xác minh cấu trúc giá - quản lý rủi ro động. Giá trị cốt lõi của nó nằm ở việc chuyển đổi lý thuyết cụm biến động trong giới học thuật thành các tín hiệu giao dịch có thể thực thi, và thông qua cơ chế xác minh đa yếu tố nghiêm ngặt để kiểm soát xu hướng giao dịch quá mức. Trong tương lai, có thể tiếp tục nâng cao hiệu suất chiến lược bằng cách đưa vào các mô-đun học máy và mô hình hóa biến động tinh tế hơn, đồng thời duy trì tính minh bạch và khả năng giải thích của kiểm soát rủi ro.

/*backtest

start: 2024-05-16 00:00:00

end: 2025-05-14 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("The VoVix Experiment", default_qty_type=strategy.fixed, initial_capital=10000, overlay=true, pyramiding=1)

// === VOLATILITY CLUSTERING ===- 1