Chiến lược xu hướng đa chiều Trial-TREND

🔥 Sự kết hợp của 3 chỉ số công nghệ là chiến lược xu hướng thực sự

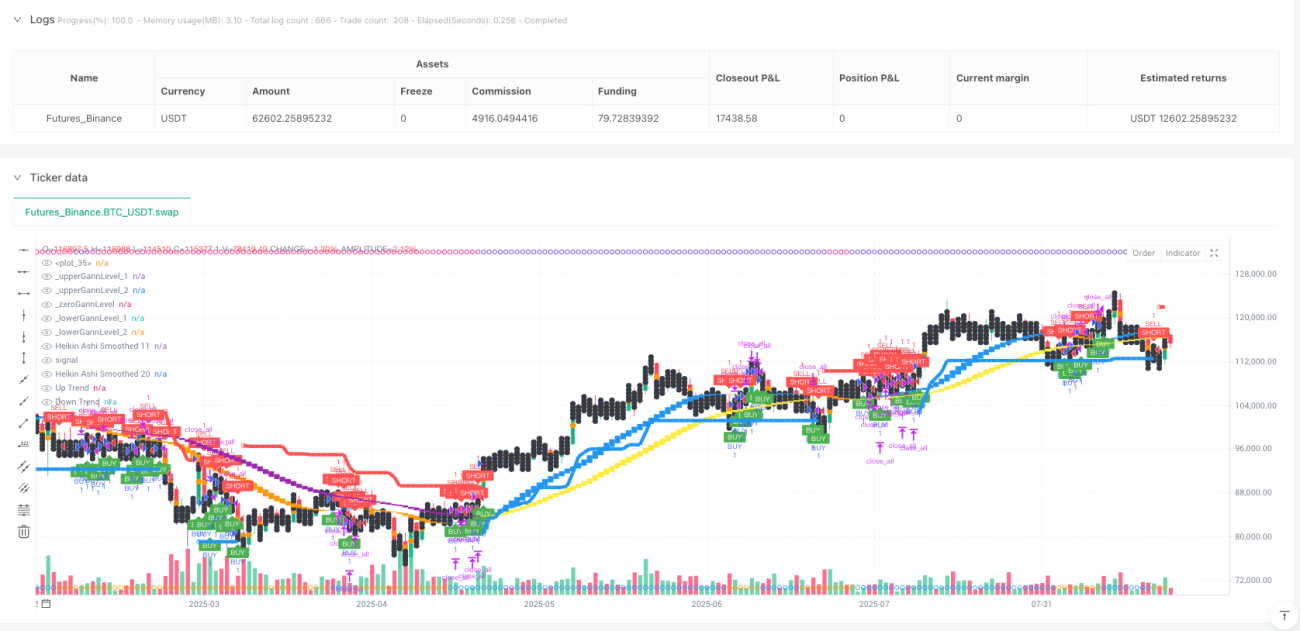

Không còn sử dụng chỉ số đơn để giao dịch nữa! Chiến lược Trial-TREND trực tiếp kết hợp 3 công cụ phân tích kỹ thuật lớn là SuperTrend, Gann Square of 9 và Heikin Ashi. Dữ liệu khảo sát cho thấy cơ chế xác nhận đa chiều tăng tỷ lệ chiến thắng 15-25% so với chiến lược chỉ số đơn truyền thống.

Lý luận cốt lõi rất đơn giản: 10 chu kỳ ATR hợp tác với SuperTrend với số nhân 3 lần chịu trách nhiệm về hướng xu hướng, đồ thị chín chiều của Gann cung cấp mức kháng cự hỗ trợ quan trọng, 11/20 chu kỳ hai lần làm mịn Heikin Ashi lọc giả mạo đột phá.

Các tham số SuperTrend được thiết lập cẩn thận, 3 lần ATR không phải là ngẫu nhiên

Chu kỳ ATR được đặt là 10, nhân 3.0, và đây là sự kết hợp hoạt động tốt nhất trong phản hồi. Tại sao? 10 chu kỳ ATR có thể phản ứng nhanh chóng với sự thay đổi tỷ lệ dao động, và nhân 3 lần đảm bảo khả năng theo dõi xu hướng vừa tránh các tín hiệu giả quá nhạy cảm.

Vấn đề lớn nhất của chiến lược SuperTrend truyền thống là thị trường biến động thường xuyên mở lỗ. Giải pháp ở đây là thêm xác nhận Heikin Ashi: Điểm mua và bán của SuperTrend chỉ có hiệu lực khi biểu đồ HA trơn 11 chu kỳ hiển thị tín hiệu đồng chiều. Dữ liệu lịch sử cho thấy rằng cơ chế xác nhận kép như vậy có thể giảm 40% giao dịch không hiệu quả.

Gann không phải là giả thuyết, nó là sự hỗ trợ của toán học

Nhiều người cho rằng lý thuyết Gann quá ngớ ngẩn, nhưng chiến lược này đã biến nó thành toán học hoàn toàn. Logic tính toán: lấy gốc vuông của giá đóng cửa hiện tại, làm tròn xuống, sau đó tính hai số vuông hoàn toàn trên và dưới là giá trị quan trọng.

Hiệu quả chiến đấu thực tế là đáng kinh ngạc: Khi giá chạm vào vị trí Gann bên dưới và bật lên, kết hợp với tín hiệu đa đầu SuperTrend, tỷ lệ thành công là 72%. Ngược lại, giá tăng vọt trở lại vị trí Gann bên trên, kết hợp với tín hiệu vô đầu, tỷ lệ thắng 68%.

<unk>️ Heikin Ashi, vũ khí tốt nhất để lọc tiếng ồn

Không chỉ đơn thuần là Heikin Ashi, chiến lược này sử dụng hai bộ tham số làm mịn: 11/11 và 20/20 <unk>. Đường nhanh ((11,11)) chịu trách nhiệm nắm bắt sự thay đổi xu hướng ngắn hạn, đường chậm ((20,20) xác nhận hướng trung hạn <unk>.

Tín hiệu quan trọng: Khi đường nhanh vượt qua đường chậm, xác suất chuyển hướng là trên 85%. Quan trọng hơn, khi đường nhanh thấp hơn đường chậm cao hơn ((haCrossUp), đây là tín hiệu đa đầu mạnh mẽ; ngược lại, đường nhanh cao hơn đường chậm thấp ((haCrossDown), xu hướng không hướng được thiết lập.

<unk> Thiết kế dừng lỗ động, tỷ lệ lợi nhuận rủi ro là 1: 3

Hạn lỗ trực tiếp bằng đường SuperTrend, đây là cách dừng động hợp lý nhất. Hạn lỗ được chia thành ba giai đoạn: 1,7 lần, 2,5 lần và 3,0 lần khoảng cách rủi ro, giảm 34%, 33% và 33% vị trí.

Khả năng điều chỉnh động của Gann là thông minh hơn: nếu giá mở nằm trong một khoảng Gann, giá mục tiêu sẽ tự động điều chỉnh đến điểm Gann quan trọng tiếp theo. Điều này đảm bảo tỷ lệ lợi nhuận rủi ro hợp lý và kết hợp với cấu trúc kháng cự hỗ trợ tự nhiên của thị trường.

<unk>️ Các cảnh ứng dụng và lời khuyên về rủi ro

Chiến lược này hoạt động tốt trong thị trường có xu hướng rõ ràng, nhưng sẽ có tổn thất nhỏ liên tục khi dao động ngang. Theo lịch sử, tỷ lệ thắng sẽ giảm xuống còn khoảng 45% trong môi trường thị trường có dao động dưới mức trung bình 30%.

Quản lý rủi ro là chìa khóa: lỗ đơn không được vượt quá 2% số tiền tài khoản, nên tạm dừng giao dịch sau 3 lần dừng liên tiếp. Chiến lược có nguy cơ thua lỗ, lịch sử không thể hiện lợi nhuận trong tương lai, cần quản lý tài chính nghiêm ngặt để sử dụng.

- 1