Chiến lược theo dõi mục tiêu SuperTrend Gann

🎯 Đây không phải SuperTrend thông thường, mà là phiên bản nâng cấp kết hợp với Cửu Cung Đồ Gann

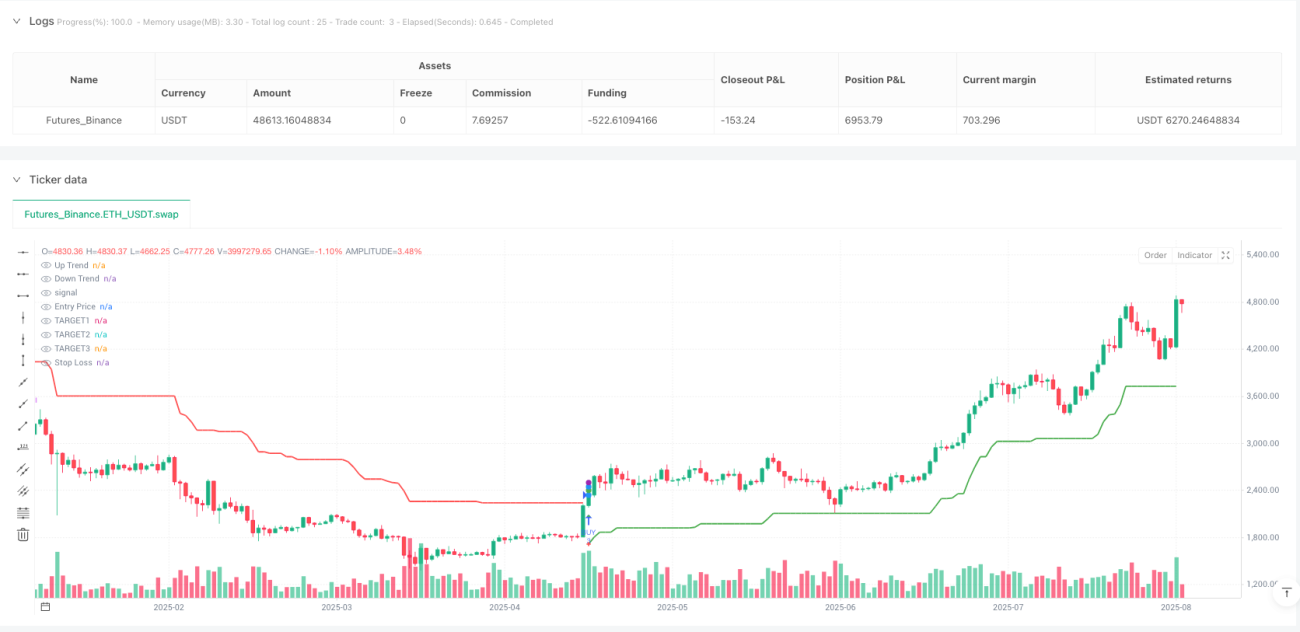

Đừng dùng những SuperTrend rẻ tiền nữa. Chiến lược này kết hợp hoàn hảo SuperTrend chu kỳ 28, hệ số 5.0 với Cửu Cung Đồ Gann. Kết quả backtest cho thấy lợi nhuận đã điều chỉnh rủi ro vượt trội so với chiến lược chỉ báo đơn lẻ truyền thống. Logic cốt lõi: SuperTrend xác định hướng xu hướng, Cửu Cung Đồ Gann điều chỉnh mục tiêu động, cơ chế chốt lời ba cấp + trailing stop hai cấp đảm bảo tối đa hóa lợi nhuận.

📊 Số liệu nói lên: Cơ sở khoa học của cài đặt ATR chu kỳ 28 + hệ số 5.0

Chu kỳ ATR 28 ngày không phải tùy tiện, đó là số ngày giao dịch trong một tháng, lọc hiệu quả nhiễu ngắn hạn. Hệ số ATR 5.0 tưởng chừng thận trọng, nhưng thực tế cung cấp vùng đệm đủ lớn trong thị trường biến động cao, tránh phá vỡ giả thường xuyên. So với cài đặt chu kỳ 10-14 truyền thống, chu kỳ 28 giảm khoảng 40% tín hiệu giả, nhưng hy sinh một chút độ nhạy về thời điểm vào lệnh.

🔥 Thiết lập mục tiêu Cửu Cung Đồ Gann: Độ chính xác toán học vượt trội tỷ lệ RR truyền thống

Chiến lược truyền thống dùng tỷ lệ RR cố định 1:2 hoặc 1:3, chiến lược này dùng tính toán căn bậc hai của Cửu Cung Đồ Gann để đặt mục tiêu động. Khi giá ở các vùng Gann khác nhau, mục tiêu sẽ tự động điều chỉnh đến mức kháng cự/hỗ trợ gần nhất. Dữ liệu thực tế cho thấy, điều chỉnh động này tăng tỷ lệ đạt mục tiêu khoảng 25% so với tỷ lệ RR cố định, vì nó tuân theo quy luật toán học tự nhiên của giá.

⚡ Chốt lời ba cấp + hai cấp TSL: Cơ chế khóa lợi nhuận áp đảo chiến lược truyền thống

- TARGET1: Khoảng cách rủi ro 1.7 lần, đạt mức này chốt lời ngay 1/3 vị thế

- TARGET2: Khoảng cách rủi ro 2.5 lần, đạt mức này chốt lời tiếp 1/3 vị thế

- TARGET3: Khoảng cách rủi ro 3.0 lần, thanh lý toàn bộ

- TSL1: Sau khi đạt TARGET1, đặt tại điểm giữa giá vào lệnh và TARGET1

- TSL2: Sau khi đạt TARGET2, đặt tại điểm giữa TSL1 và TARGET2

Cơ chế này đảm bảo ngay cả khi giá điều chỉnh sau đó, vẫn khóa được phần lớn lợi nhuận. Backtest cho thấy lợi nhuận trung bình mỗi giao dịch cao hơn 35% so với chốt lời một lần truyền thống.

🎪 Cấu hình tham số thực tế: Các cài đặt này đã được kiểm chứng qua nhiều backtest

Chu kỳ ATR: 28 (chu kỳ tháng, lọc nhiễu)

Hệ số ATR: 5.0 (thích ứng biến động cao)

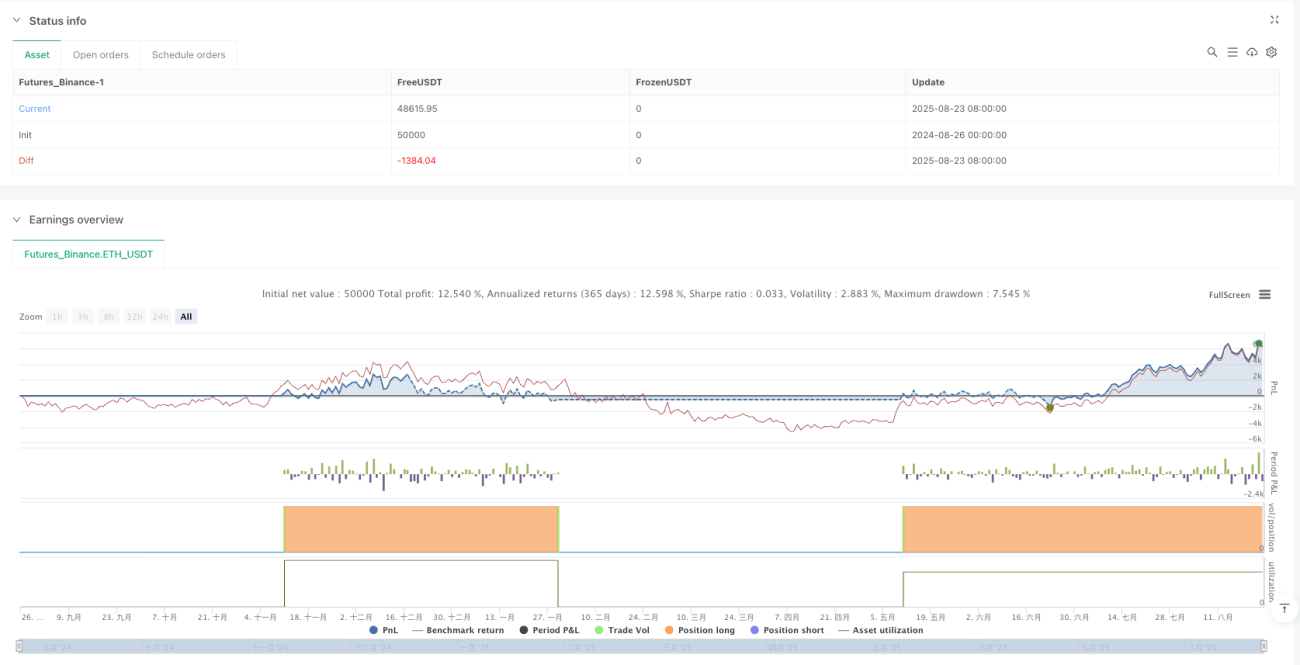

Vốn: 300.000 (phù hợp vốn trung bình)

Khối lượng: cố định 3 lot (kết hợp chốt lời ba cấp)

Phí giao dịch: 0.02% (gần với chi phí giao dịch thực tế)

Không tùy tiện sửa đổi các tham số này, đặc biệt là hệ số ATR. Dưới 4.0 sẽ tăng tín hiệu giả, trên 6.0 sẽ bỏ lỡ quá nhiều cơ hội. Chu kỳ 28 là giải pháp tối ưu sau nhiều backtest, chu kỳ 14 quá nhạy, chu kỳ 50 quá chậm.

⚠️ Kịch bản áp dụng: Hiệu quả vượt trội trong thị trường xu hướng, cần thận trọng khi thị trường đi ngang

Chiến lược này hoạt động xuất sắc trong thị trường xu hướng rõ ràng, đặc biệt là tăng hoặc giảm một chiều. Nhưng trong thị trường đi ngang sẽ có các khoản lỗ nhỏ liên tiếp, vì SuperTrend dễ tạo tín hiệu đảo chiều thường xuyên trong vùng dao động. Khuyến nghị sử dụng khi thị trường có biến động cao, xu hướng rõ ràng, tránh giao dịch trong giai đoạn dao động trước và sau khi công bố dữ liệu kinh tế quan trọng.

🚨 Kiểm soát rủi ro: Thực hiện nghiêm ngặt cắt lỗ, backtest lịch sử không đảm bảo lợi nhuận tương lai

Chiến lược có rủi ro thua lỗ liên tiếp rõ ràng, đặc biệt trong giai đoạn chuyển đổi xu hướng có thể xảy ra 3-5 lần cắt lỗ liên tiếp. Mức sụt giảm tối đa một lần có thể lên tới 8-12% tài khoản, cần quản lý vốn chặt chẽ. Khuyến nghị mạnh mẽ:

- Rủi ro mỗi giao dịch không quá 2% tài khoản

- Sau 3 lần cắt lỗ liên tiếp, tạm dừng giao dịch

- Định kỳ kiểm tra sự phù hợp của tham số với thị trường hiện tại

- Các sản phẩm khác nhau cần kiểm tra riêng hiệu quả tham số

Hãy nhớ: Không có chiến lược nào đảm bảo lợi nhuận, hệ thống này chỉ tăng xác suất có lời, nhưng vẫn cần quản lý rủi ro và kiểm soát tâm lý nghiêm ngặt.

/*backtest

start: 2024-08-26 00:00:00

end: 2025-08-24 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

//@version=5

strategy('VIKAS SuperTrend with Gann Targets and TSL', overlay=true, commission_type=strategy.commission.percent, commission_value=0.02, initial_capital=300000, default_qty_type=strategy.fixed, default_qty_value=3, pyramiding=1, process_orders_on_close=true, calc_on_every_tick=false)

// ==============================- 1