Chiến thuật trì hoãn thoát: Nghệ thuật chờ đợi trước khi rời đi

🎯 Chiến lược này thực sự đang làm gì?

Bạn có biết không? Hầu hết các trader đều mắc một tật: thấy tín hiệu bất lợi là lập tức thoát lệnh! 😱 Nhưng chiến lược này lại đi ngược lại, nó bảo bạn: "Đừng vội, chờ xem thêm đã!"

Giống như yêu đương vậy, đối phương nói một câu giận dữ là bạn chia tay ngay? Quá bốc đồng rồi! Chiến lược này sẽ đợi 3 cây nến (có thể điều chỉnh) để xem có thực sự "chia tay" hay chỉ là biểu hiện cảm xúc nhất thời.

📊 Logic cốt lõi: Không đưa ra quyết định bốc đồng

Điều kiện vào lệnh:

- Phát hiện mô hình phá vỡ đỉnh/đáy (Higher Low / Lower High)

- Kết hợp xác nhận của nến (giá đóng cửa đúng hướng)

- Hệ thống chấm điểm đa chiều: Động lượng RSI + Xác nhận khối lượng + Phân tích biến động

- Điểm tối thiểu 3.0 mới được vào lệnh (thang điểm 5.0)

Nhấn mạnh! Hệ thống chấm điểm ở đây cực kỳ thông minh, tổng hợp xem xét:

- Sức mạnh của nến (tỷ lệ thân nến)

- Khối lượng giao dịch có tăng hay không

- RSI ở trong vùng hợp lý

- Mức biến động hiện tại

⏰ Trí tuệ của việc thoát lệnh trì hoãn

Chiến lược truyền thống: Thấy tín hiệu thất bại → Thoát ngay lập tức

Chiến lược này: Thấy tín hiệu thất bại → Đợi 3 cây nến → Xác nhận lại → Thoát lệnh hợp lý

Tại sao phải trì hoãn?

- Tránh bẫy phá vỡ giả: Thị trường thường "giả chết", trì hoãn có thể lọc nhiễu

- Giảm giao dịch thường xuyên: Tiết kiệm chi phí hoa hồng

- Tăng tỷ lệ thắng: Cho xu hướng thêm thời gian phát triển

🛡️ Quản lý rủi ro: Nghiêm ngặt khi cần thiết

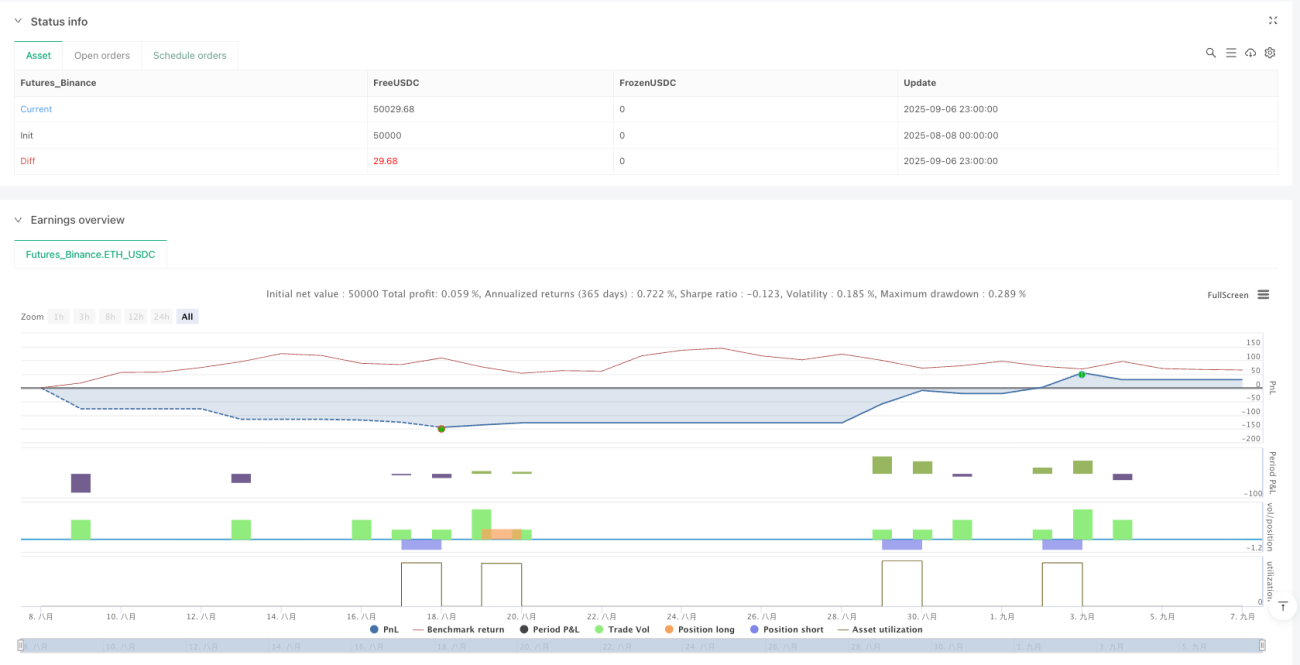

Mặc dù thoát lệnh khá "phật giáo", nhưng kiểm soát rủi ro tuyệt đối nghiêm ngặt:

- Cắt lỗ: 1.5 lần ATR (có thể điều chỉnh)

- Chốt lời: 2.5 lần ATR (có thể điều chỉnh)

- Thời gian giao dịch: Chỉ giao dịch trong giờ giao dịch chứng khoán Mỹ

- Đóng lệnh cuối phiên: Tuyệt đối không giữ qua đêm

🎨 Thiết kế trực quan: Nhìn là thấy ngay

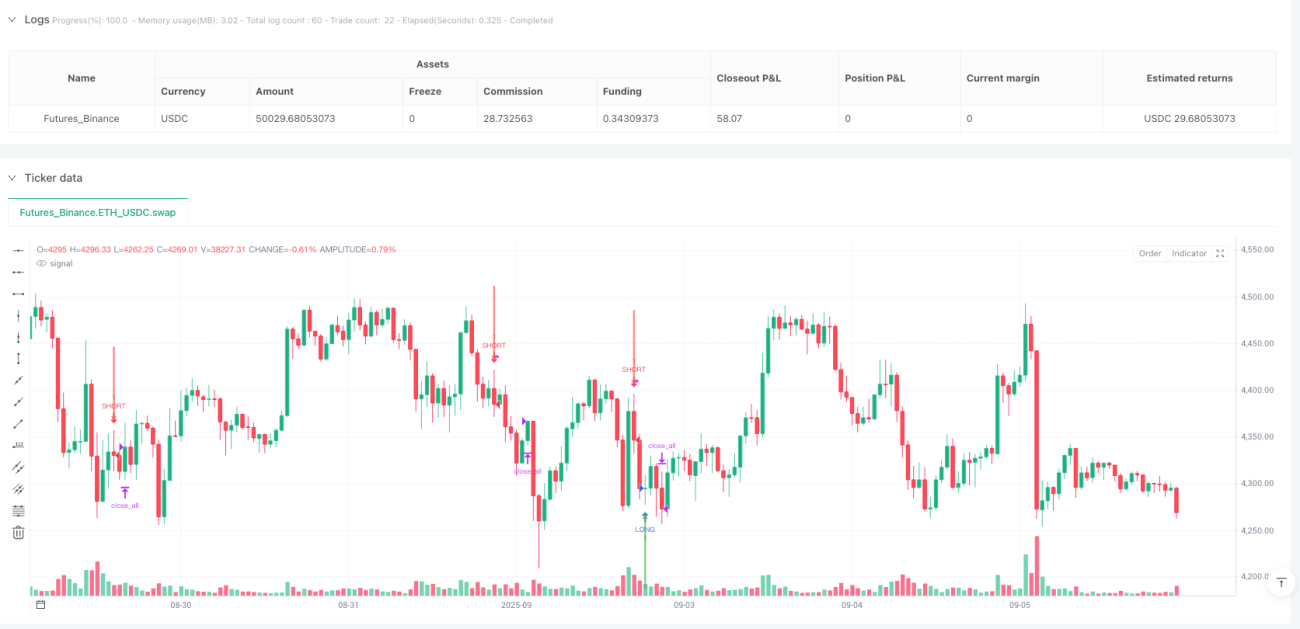

- 🟢 Tam giác xanh: Tín hiệu mua thông thường

- 🔴 Tam giác đỏ: Tín hiệu bán thông thường

- 🏁 Cờ đánh dấu: Tín hiệu chất lượng cao (điểm ≥ 4.5)

- 🟠 Chữ X màu cam: Tín hiệu thất bại sớm (bỏ qua)

- 🔴 Chữ X màu đỏ: Tín hiệu thất bại trì hoãn (thực hiện thoát lệnh)

Hướng dẫn tránh bẫy: Khi thấy chữ X màu cam đừng hoảng, đây là "báo động giả" mà chiến lược cố tình bỏ qua!

💡 Tình huống áp dụng

Chiến lược này đặc biệt phù hợp với:

- Bắt đảo chiều trong thị trường đi ngang

- Trader không muốn bị hành hạ bởi cắt lỗ thường xuyên

- Nhà đầu tư muốn cải thiện chất lượng tín hiệu

- Người yêu thích giao dịch trong ngày trên thị trường chứng khoán Mỹ

Hãy nhớ: Kiên nhẫn là vũ khí lớn nhất của trader, đôi khi "chờ rồi hãy đi" còn khôn ngoan hơn "hành động ngay lập tức"! 🚀

- 1