🎯 Cốt lõi chiến lược: Săn tiền thông minh trên thị trường cuối tuần

Bạn có biết? Khi các ông lớn Phố Wall đi nghỉ cuối tuần, thị trường crypto lại ẩn chứa cơ hội! Chiến lược này giống như một nhân viên bảo vệ ca đêm, chuyên đi nhặt nhạnh những món hời khi các nhà đầu tư tổ chức "tan ca".

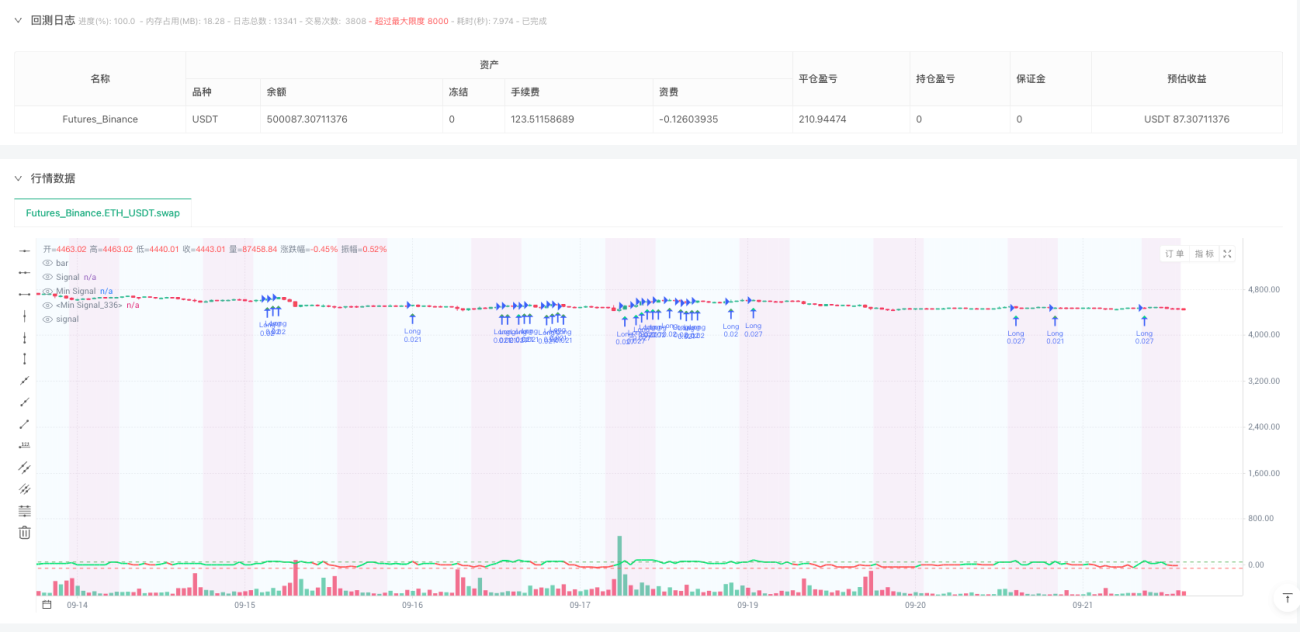

Lưu ý quan trọng! Chiến lược này chỉ giao dịch vào Thứ Bảy và Chủ Nhật, đặc biệt là khung giờ 0-8h UTC Chủ Nhật. Tại sao? Vì lúc này thanh khoản tương đối thấp, hiệu quả của phân tích kỹ thuật lại càng cao, giống như trong một thư viện yên tĩnh, bạn dễ dàng nghe thấy những âm thanh nhỏ nhất.

📊 Tổng hợp đa chỉ báo: Không phải đánh một mình

Chiến lược này giống như lắp ráp một Biệt đội báo thù:

- RSI(8 chu kỳ): Nhanh chóng nắm bắt tín hiệu quá mua/quá bán

- MACD(8,17,9): Xác nhận động lượng xu hướng

- Dải Bollinger (20,2.5): Nhận diện vùng giá cực trị

- Phân kỳ CVD: Phát hiện ý đồ thực sự của dòng tiền thông minh

Hướng dẫn tránh bẫy: Chỉ báo đơn lẻ giống như xem phim một mình, dễ bị cốt truyện dẫn dắt sai lầm. Đa chỉ báo xác nhận giống như xem phim cùng bạn bè, có thể nghe được nhiều quan điểm khác nhau!

💰 Quản lý vốn thông minh: Chỉ 500 đô la cũng có thể chơi

Phần thú vị nhất đây! Hệ thống này được thiết kế riêng cho vốn nhỏ:

- Tối thiểu 120 đô la một lệnh: Không bắt bạn all-in

- Tối đa 4 vị thế đồng thời: Phân tán rủi ro, không bỏ hết trứng vào một rổ

- Đòn bẩy động 5-20 lần: Tự động điều chỉnh theo biến động thị trường

Giống như lái xe vậy, trên đường cao tốc có thể chạy nhanh, nhưng trong hẻm nhỏ phải đi chậm lại. Hệ thống sẽ điều chỉnh kích thước vị thế dựa trên đặc điểm rủi ro của từng đồng coin.

🛡️ Kiểm soát rủi ro: Còn cẩn thận hơn cả mẹ bạn

Cơ chế bảo vệ ba lớp:

- Giới hạn thua lỗ hàng ngày 5%: Hôm nay lỗ quá nhiều? Ngày mai quay lại

- Giới hạn thua lỗ cuối tuần 15%: Chơi quá đà cuối tuần cũng có giới hạn

- Dừng sau 4 lần thua liên tiếp: Ngăn chặn giao dịch theo cảm xúc

Hệ thống phanh khẩn cấp: Nếu tài khoản lỗ vượt quá 30%, lập tức dừng mọi giao dịch. Giống như hệ thống ABS trên ô tô, có thể cứu mạng trong thời khắc then chốt!

- 1