Chiến lược trung bình bậc thang xu hướng: Khi thị trường đi ngang, làm thế nào để "nằm dài" một cách thanh lịch?

Tại sao các chiến lược theo dõi xu hướng truyền thống thường "lật xe" trong thị trường dao động?

Là một người làm trong lĩnh vực giao dịch định lượng, tôi thường xuyên nhận được câu hỏi: Tại sao những chiến lược hoạt động xuất sắc trong thị trường xu hướng, khi gặp thị trường dao động lại bắt đầu sụt giảm mạnh?

Câu trả lời thực ra rất đơn giản: Hầu hết các chiến lược theo dõi xu hướng đều mắc "chứng ám ảnh xu hướng" – chúng luôn cố gắng duy trì giao dịch tần suất cao trong mọi điều kiện thị trường, nhưng lại bỏ qua một thực tế cơ bản: 70% thời gian thị trường nằm trong trạng thái đi ngang (sideways).

Chiến lược "Xu hướng bậc thang trung bình" mà chúng ta phân tích hôm nay lại đưa ra một giải pháp thú vị cho vấn đề này: Tích cực theo dõi trong thị trường xu hướng, "nằm im thanh lịch" trong thị trường dao động.

"Trung bình bậc thang" là gì? Khái niệm này định nghĩa lại việc theo dõi xu hướng như thế nào?

Các chiến lược đường trung bình động truyền thống có một khiếm khuyết chí mạng: Chúng luôn thay đổi. Dù thị trường đang có xu hướng mạnh hay đi ngang, đường trung bình luôn điều chỉnh theo biến động giá, dẫn đến rất nhiều tín hiệu giả.

Ý tưởng cốt lõi của "trung bình bậc thang" là: Làm cho đường trung bình "đóng băng" trong những điều kiện nhất định.

Logic triển khai cụ thể như sau:

-

Phát hiện trạng thái xu hướng: Xác định sức mạnh xu hướng thị trường thông qua chỉ báo ADX

- ADX > 25: Thị trường xu hướng mạnh

- Độ dốc đường trung bình < 0.3%: Thị trường đi ngang

-

Chuyển đổi đường trung bình động:

- Khi xu hướng mạnh: Theo dõi EMA(21) bình thường

- Khi đi ngang: Đường trung bình "đóng băng" ở vị trí nằm ngang, tạo thành hỗ trợ/kháng cự

Sự tinh tế của thiết kế này nằm ở chỗ: Nó giúp chiến lược thể hiện "tính cách" khác nhau trong các môi trường thị trường khác nhau – nhạy bén khi có xu hướng, ổn định khi dao động.

Làm thế nào để triển khai hệ thống "bắt xu hướng"?

Ngoài cơ chế trung bình bậc thang cơ bản, chiến lược này còn tích hợp một module "bắt xu hướng", đây là phần tôi cho là sáng tạo nhất:

Cơ chế đảo chiều nhanh:

- Khi xuất hiện xu hướng mạnh ngược chiều ngay sau khi vừa đóng lệnh

- Thiết lập vị thế mới trong vòng 3 chu kỳ

- Điều kiện: ADX > 30 và chênh lệch DI+ với DI- > 10

Thiết kế này giải quyết một vấn đề quan trọng của các chiến lược truyền thống: Làm thế nào để nhanh chóng điều chỉnh vị thế khi xu hướng đảo chiều ở giai đoạn đầu.

Hãy tưởng tượng một tình huống: Bạn vừa đóng lệnh mua do cắt lỗ, và ngay lập tức thị trường xuất hiện xu hướng giảm mạnh. Chiến lược truyền thống có thể cần chờ tín hiệu mới xác nhận, nhưng hệ thống "bắt xu hướng" này có thể nhanh chóng thiết lập vị thế bán trong vòng 3 chu kỳ.

Quản lý rủi ro: Tại sao cần phân biệt trạng thái thị trường?

Điều đáng học hỏi nhất của chiến lược này là cơ chế quản lý rủi ro phân hóa:

Kiểm soát rủi ro trong thị trường đi ngang:

- Điều chỉnh mức cắt lỗ gần đường trung bình bậc thang

- Giảm bội số ATR, siết chặt cắt lỗ

- Đặt mục tiêu thận trọng hơn

Kiểm soát rủi ro trong thị trường xu hướng:

- Sử dụng cắt lỗ theo bội số ATR tiêu chuẩn

- Kích hoạt cắt lỗ di động dạng bậc thang

- Cho phép biến động giá lớn hơn

Thiết kế này thể hiện một triết lý giao dịch quan trọng: Các môi trường thị trường khác nhau cần mức độ chấp nhận rủi ro khác nhau. Trong thị trường đi ngang, chúng ta nên thận trọng hơn; trong thị trường xu hướng, chúng ta cần cho lợi nhuận có thêm không gian để chạy.

Cắt lỗ di động dạng bậc thang: Làm thế nào cân bằng giữa bảo vệ lợi nhuận và theo dõi xu hướng?

Cắt lỗ di động truyền thống thường quá máy móc, hoặc quá chặt dẫn đến thoát lệnh sớm, hoặc quá lỏng không bảo vệ được lợi nhuận hiệu quả. Cắt lỗ di động dạng bậc thang của chiến lược này đưa ra một giải pháp thông minh hơn:

Logic thiết lập bậc thang:

- Tính toán khoảng cách bậc thang động dựa trên ATR

- Tối đa 5 cấp bậc thang

- Mỗi khi phá vỡ một bậc thang, mức cắt lỗ được nâng lên tương ứng

Ưu điểm của thiết kế này là: Nó có thể bảo vệ lợi nhuận đồng thời cho xu hướng đủ không gian phát triển.

Cần lưu ý gì khi ứng dụng thực tế?

Dựa trên kinh nghiệm giao dịch thực tế của tôi, khi sử dụng các chiến lược loại này cần chú ý những điểm sau:

-

Bẫy tối ưu hóa tham số: Đừng tối ưu hóa quá mức ngưỡng ADX, các giá trị từ 25-30 thường hoạt động ổn định trong hầu hết các thị trường.

-

Khả năng thích ứng thị trường: Chiến lược này phù hợp hơn với các thị trường có độ biến động vừa phải, trong môi trường biến động cực đoan có thể cần điều chỉnh bội số ATR.

-

Quản lý vốn: Khuyến nghị khối lượng mỗi lệnh không vượt quá 10% tổng vốn, đặc biệt khi kích hoạt chức năng bắt xu hướng.

-

Bẫy backtest: Đặc biệt chú ý ảnh hưởng của trượt giá (slippage) và phí giao dịch, nhất là trong các giao dịch tần suất cao ở thị trường dao động.

Giá trị đổi mới của chiến lược này là gì?

Từ góc độ phát triển của chiến lược định lượng, chiến lược này đại diện cho một hướng tiến hóa quan trọng: Chuyển từ logic đơn nhất sang tự thích ứng đa trạng thái.

Các chiến lược truyền thống thường cố gắng đối phó với mọi tình huống thị trường bằng một bộ logic cố định, trong khi chiến lược này thể hiện trí tuệ "tùy cơ ứng biến":

- Trong thị trường xu hướng, nó hành động như một kẻ theo dõi xu hướng mạnh mẽ

- Trong thị trường dao động, nó hành động như một nhà giao dịch trong vùng bảo thủ

Cách tiếp cận này có ý nghĩa khơi gợi quan trọng đối với các nhà phát triển chiến lược: Chúng ta nên trang bị cho chiến lược khả năng "cảm nhận thị trường", thay vì mù quáng thực thi logic cố định.

Cuối cùng, cần nhấn mạnh rằng không có chiến lược nào là vạn năng. Mặc dù chiến lược trung bình bậc thang này rất thanh lịch về mặt lý thuyết, nhưng trong ứng dụng thực tế vẫn cần kết hợp với môi trường thị trường cụ thể và sở thích rủi ro cá nhân để điều chỉnh. Hãy nhớ rằng, chiến lược tốt nhất luôn là chiến lược phù hợp nhất với bạn.

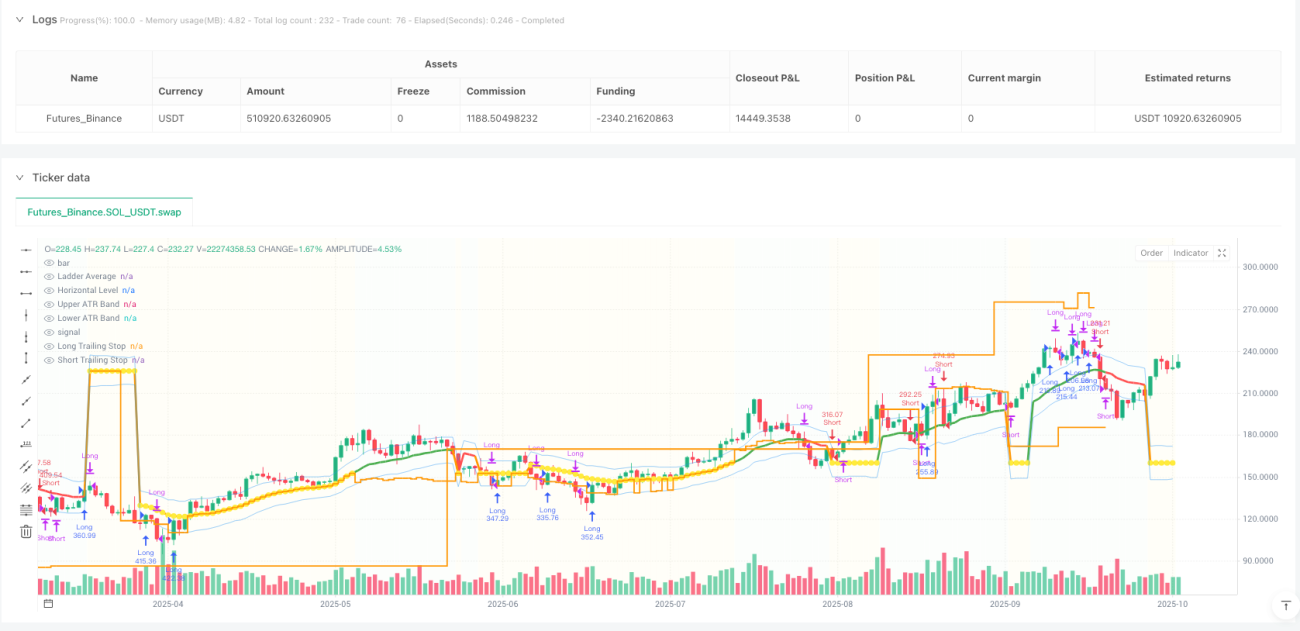

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1