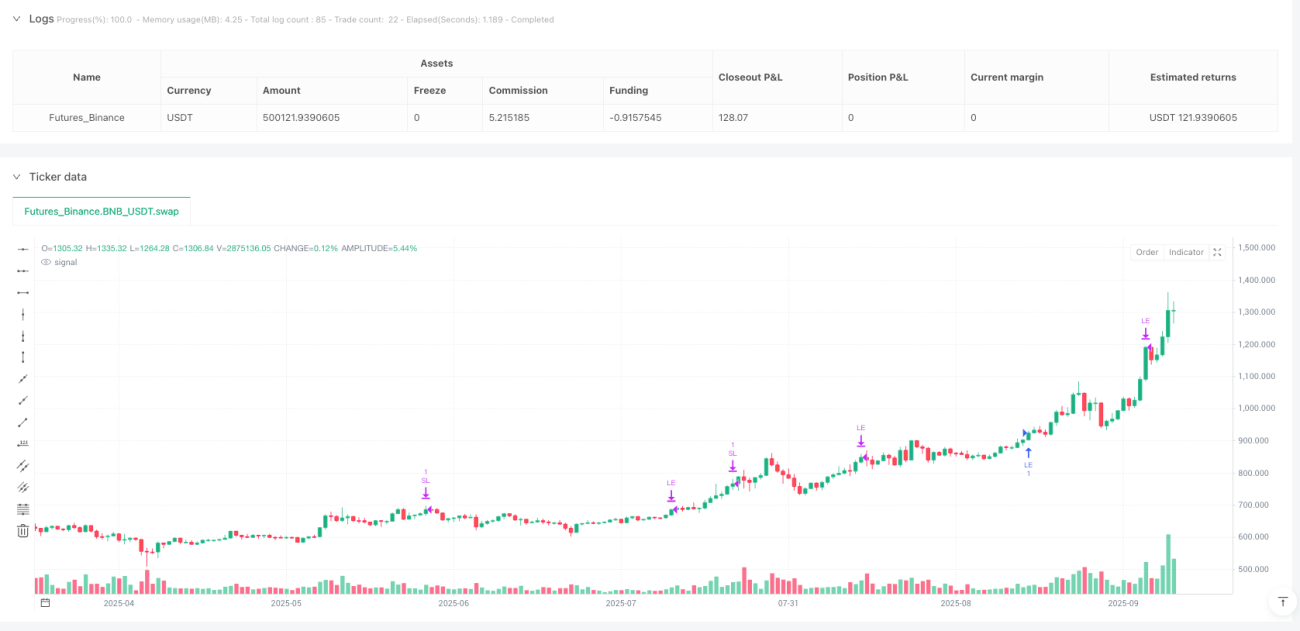

Chiến lược đột phá ngày nội bộ Williams

🎯 Chiến lược này thực sự đang chơi trò gì?

Bạn biết không? Chiến lược này giống như chơi trò "trốn tìm" trên thị trường chứng khoán vậy! 📈 Khi thị trường xuất hiện "ngày nội bộ" (tức biến động hôm nay hoàn toàn nằm trong biên độ hôm qua), giống như thị trường đang nén chặt để chuẩn bị bùng nổ lớn!

Nhấn mạnh! Chiến lược này chuyên săn lùng những khoảnh khắc bứt phá "không thể kìm nén", đặc biệt là vào các "ngày giao dịch vàng" như Thứ Hai, Thứ Năm và Thứ Sáu.

🔍 Logic cốt lõi của chiến lược cực kỳ đơn giản

Hãy tưởng tượng thị trường giống như một lò xo bị nén:

- Hôm qua là "ngày nội bộ" (hoàn toàn nằm trong biên độ hôm kia)

- Hôm kia là cây nến xanh lớn (phe mua rất phấn khích)

- Giá mở cửa hôm nay thấp hơn mức kháng cự quan trọng

Khi giá phá vỡ mức cao nhất của 3 chu kỳ trước, giống như lò xo được giải phóng, chiến lược ngay lập tức vào lệnh mua! 🚀

💡 Quản lý rủi ro: Hai lớp bảo vệ

Lớp bảo vệ thứ nhất: Cắt lỗ cố định

Có thể chọn cắt lỗ theo điểm hoặc theo phần trăm, giống như đặt ra "giới hạn thua lỗ" cho bản thân, tuyệt đối không tham lam!

Lớp bảo vệ thứ hai: Nguyên tắc thoát FPO

Đây là điểm thông minh nhất! Một khi ngày nào đó ngay từ đầu phiên đã có lợi nhuận, lập tức chốt lời. Giống như triết lý "thấy tốt thì thu về", không chờ thị trường đổi ý! ✨

🎪 Tại sao chọn các ngày giao dịch cụ thể?

Chiến lược chỉ giao dịch vào Thứ Hai, Thứ Năm và Thứ Sáu, đây không phải là lựa chọn ngẫu nhiên! Những ngày này thường:

- Thứ Hai: Xác định xu hướng của tuần mới

- Thứ Năm: Ngày công bố dữ liệu quan trọng

- Thứ Sáu: Ngày tái cơ cấu vốn

Tránh các "ngày ảm đạm" như Thứ Ba và Thứ Tư, chỉ hành động vào những ngày có câu chuyện!

🌟 Chiến lược này phù hợp với ai?

Nếu bạn là nhà giao dịch thích "vào nhanh ra nhanh", không muốn theo dõi thị trường cả ngày, thì chiến lược này thực sự được thiết kế dành riêng cho bạn! Nó có tín hiệu vào lệnh rõ ràng, quy tắc cắt lỗ minh bạch, và cơ chế thoát lợi nhuận thông minh.

Hãy nhớ: Thị trường giống như lò xo, càng nén mạnh, càng bật cao! 🎯

- 1