🎯 Đây là chiến lược thần thánh gì? 20 chỉ báo cùng lên sàn!

Bạn có biết không? Chiến lược này giống như trang bị cho giao dịch của bạn một trợ lý AI siêu thông minh! Nó đồng thời giám sát 20 tín hiệu thị trường khác nhau, chỉ khi phần lớn các chỉ báo đều nói "có thể" thì mới đưa ra đề xuất giao dịch. Giống như mua nhà phải xem vị trí, giá cả, kiểu dáng, giao thông... chỉ khi hài lòng về mọi mặt mới xuống tiền vậy!

Nhấn mạnh! Đây không phải là chiến lược đơn chỉ báo thông thường, mà là một "hệ thống cộng hưởng đa chiều". Hãy tưởng tượng, nếu chỉ có một người bạn nói cổ phiếu nào đó tốt, bạn có thể bán tín bán nghi; nhưng nếu 20 người bạn chuyên nghiệp đều nói tốt, bạn có tự tin hơn không?

📊 Tiết lộ kho vũ khí cốt lõi

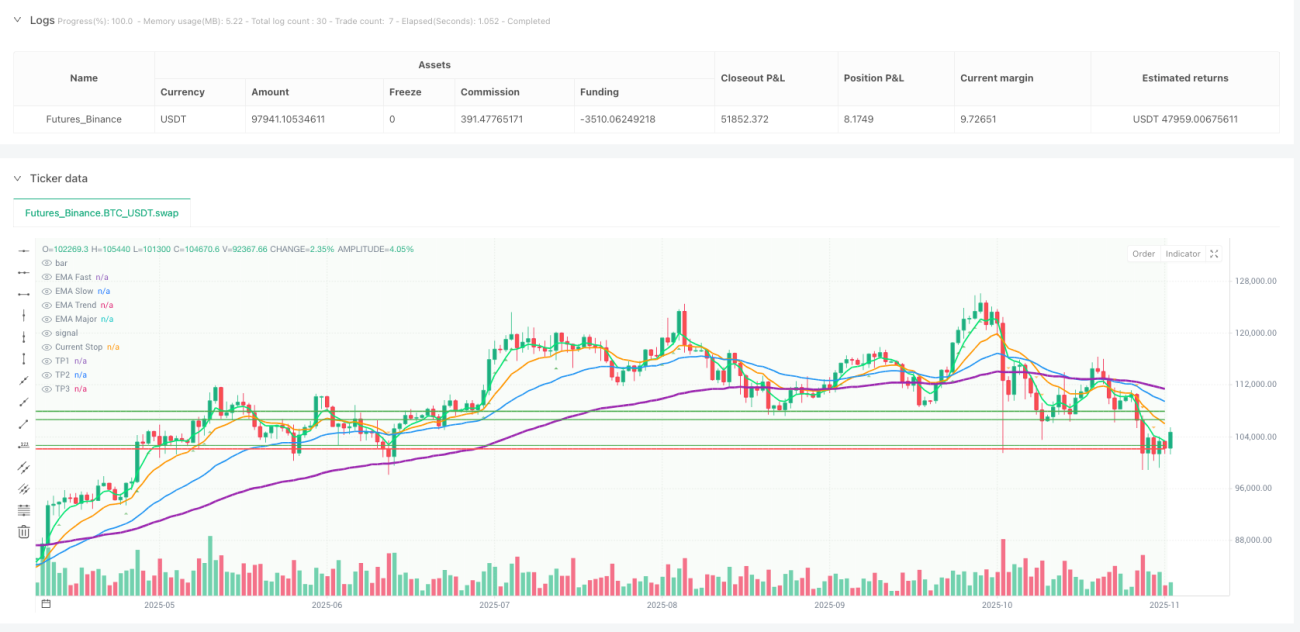

Ba kiếm sĩ nhận diện xu hướng 🗡️

- EMA nhanh (5) vs EMA chậm (13): Nắm bắt điểm đảo chiều xu hướng ngắn hạn

- EMA lọc xu hướng (34): Xác nhận hướng trung hạn

- EMA xu hướng chính (89): Nắm bắt hướng lớn, không bị nhiễu động nhỏ làm mê hoặc

Phân tích đa khung thời gian ⏰

Chức năng này quá tuyệt! Chiến lược đồng thời xem xét xu hướng 1 giờ và 4 giờ, giống như khi lái xe bạn vừa phải nhìn đường phía trước, vừa phải xem lộ trình tổng thể trên bản đồ. Tránh được tình huống khó xử "khung thời gian nhỏ tăng, khung thời gian lớn giảm"!

Quản lý rủi ro thông minh 🛡️

- Điều chỉnh vị thế động: Tự động điều chỉnh kích thước đặt cược theo biến động thị trường

- Chốt lời theo đợt: Không tham lam, thấy ngon là chốt một phần

- Stop loss di động: Vũ khí bảo vệ lợi nhuận

🔥 Logic giao dịch với 20 lớp bảo hiểm

Tín hiệu mua cần thỏa mãn:

- Xu hướng lên: Tất cả EMA sắp xếp theo hướng tăng

- Động lượng đủ: RSI, MACD, Stochastic RSI đều bật đèn xanh

- Khối lượng hỗ trợ: Tăng kèm khối lượng lớn mới là tăng thật

- Cấu trúc thị trường lành mạnh: Các đỉnh liên tục nâng cao

- Hỗ trợ thanh khoản: Các ngưỡng hỗ trợ quan trọng còn nguyên vẹn

Tín hiệu bán thì ngược lại!

Hướng dẫn tránh bẫy ⚠️: Chiến lược còn có "phát hiện nén Bollinger", khi thị trường quá yên tĩnh sẽ tạm dừng giao dịch, tránh bị vả mặt qua lại trong thị trường dao động!

💰 Vũ khí bí mật tối đa hóa lợi nhuận

Chiến lược chốt lời theo đợt 📈

- Chốt lời lần 1: Khi tỷ lệ lợi nhuận/rủi ro đạt 2 lần, bán 30% vị thế

- Chốt lời lần 2: Khi đạt 3,5 lần, bán tiếp 40% vị thế

- Vị thế còn lại: Dùng stop loss di động để bảo vệ, để lợi nhuận chạy tiếp

Nâng cấp stop loss thông minh 🎯

Sau khi đạt lợi nhuận 2,5 lần, stop loss tự động chuyển về giá vốn, đảm bảo giao dịch này ít nhất không thua lỗ. Giống như mua bảo hiểm cho lợi nhuận của bạn vậy!

Stop loss động theo dõi 🏃♂️

Khi lợi nhuận đạt đến một mức nhất định, stop loss sẽ đi theo giá như cái bóng, vừa bảo vệ lợi nhuận vừa để lại không gian cho xu hướng tăng.

🚀 Tại sao chiến lược này lại mạnh đến vậy?

- Bao phủ toàn diện: Phân tích kỹ thuật, quản lý vốn, kiểm soát rủi ro – không thiếu một thứ nào

- Lọc thông minh: 20 điều kiện sàng lọc nhiều lớp, nâng cao đáng kể tỷ lệ thành công

- Khả năng thích ứng cao: Phân tích đa khung thời gian, phù hợp với các môi trường thị trường khác nhau

- Thiết kế nhân văn: Thực thi tự động, tránh giao dịch cảm tính

Chiến lược này giống như đóng gói một đội ngũ giao dịch giàu kinh nghiệm vào trong code, hoạt động 24/7 không nghỉ để tìm kiếm cơ hội giao dịch tốt nhất cho bạn!

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1