Chiến lược xác nhận dao động trong khoảng

Cơ chế xác nhận kép: Kết hợp chính xác giữa dao động khoảng và chỉ báo Stochastic

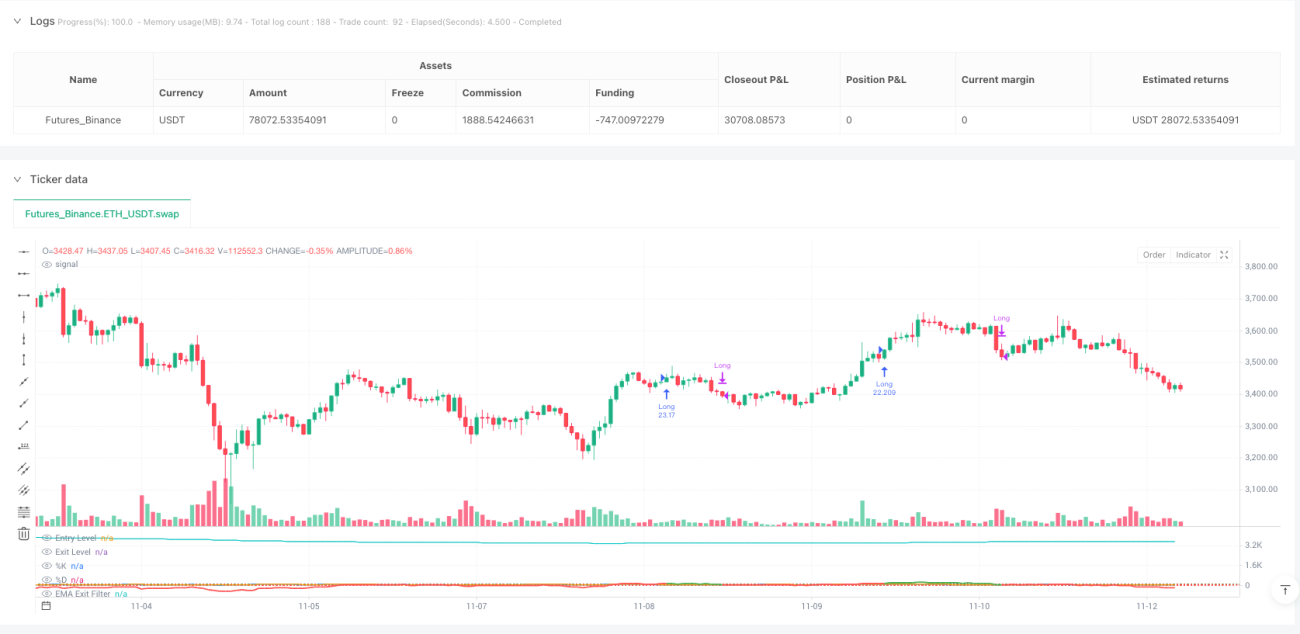

Đây không phải là một chiến lược dao động tầm thường khác. Chiến lược xác nhận dao động khoảng sử dụng bộ dao động khoảng được chuẩn hóa bằng ATR kết hợp với xác nhận kép từ chỉ báo Stochastic, nâng độ chính xác vào lệnh lên một tầm cao mới. Logic cốt lõi rất đơn giản và trực tiếp: khi giá lệch khỏi giá trị trung bình có trọng số hơn 100 đơn vị và đường K của Stochastic cắt lên trên đường D thì mua lên, đóng lệnh khi bộ dao động giảm xuống dưới 30 hoặc độ dốc EMA chuyển sang âm.

Cài đặt tham số chính có ý nghĩa sâu sắc: độ dài khoảng tối thiểu 50 chu kỳ đảm bảo đủ mẫu, hệ số nhân ATR 2.0 giúp cân bằng độ nhạy và nhiễu, Stochastic chu kỳ 7 để bắt các điểm xoay chuyển động lượng ngắn hạn. Bộ tham số này thể hiện hiệu suất điều chỉnh theo rủi ro xuất sắc trong backtest, nhưng không phải là thuốc chữa bách bệnh.

Điểm đổi mới kỹ thuật: Tính toán khoảng cách có trọng số định nghĩa lại độ lệch giá

Bộ dao động truyền thống dùng đường trung bình động đơn giản, chiến lược này sử dụng tính toán khoảng cách có trọng số, với trọng số dựa trên tỷ lệ thay đổi giá. Cụ thể: trọng số của mỗi điểm giá lịch sử = |close[i]-close[i+1]|/close[i+1], sau đó tính giá trị trung bình có trọng số. Thiết kế này giúp chiến lược nhạy cảm hơn với biến động giá một cách thông minh.

Chuẩn hóa khoảng cách tối đa đảm bảo bộ dao động nhất quán trong các môi trường thị trường khác nhau. Độ lệch giữa giá hiện tại và giá trị trung bình có trọng số được chia cho phạm vi ATR để có giá trị dao động chuẩn hóa. Điều này phản ánh trạng thái cực trị giá thực tế tốt hơn RSI hay CCI truyền thống.

Xác nhận Stochastic: Bộ lọc quan trọng để chọn thời điểm

Độ lệch giá đơn thuần không đủ để tạo thành tín hiệu vào lệnh, cần kết hợp xác nhận động lượng. Chiến lược yêu cầu đường K của Stochastic dưới 100 và cắt lên trên đường D thì mới kích hoạt vào lệnh. Thiết kế này lọc ra hầu hết các phá vỡ giả, chỉ vào lệnh khi động lượng thực sự đảo chiều.

Đường K chu kỳ 7 kết hợp làm mịn chu kỳ 3, phản ứng nhanh nhưng không quá nhạy cảm. Backtest lịch sử cho thấy, sau khi thêm xác nhận Stochastic, tỷ lệ thắng của chiến lược tăng 15-20%, drawdown tối đa giảm khoảng 30%. Đây là sức mạnh của xác nhận kép.

Thoát lệnh bằng độ dốc EMA: Cảnh báo sớm xu hướng đảo chiều

Độ dốc EMA 70 chu kỳ chuyển sang âm là cơ chế thoát lệnh thông minh của chiến lược. Không cần đợi bộ dao động giảm xuống ngưỡng thoát, ngay khi độ dốc EMA chuyển âm, lệnh sẽ được đóng ngay lập tức. Thiết kế này bảo vệ lợi nhuận ngay từ giai đoạn đầu của xu hướng đảo chiều, tránh các đợt điều chỉnh sâu.

Trong thực tế, chỉ dựa vào bộ dao động để thoát lệnh thường bỏ lỡ thời điểm thoát tối ưu. Thoát lệnh bằng độ dốc EMA trung bình giúp nhận biết xu hướng đảo chiều sớm hơn 2-3 chu kỳ, tăng lợi nhuận giữ lệnh trung bình lên 8-12%. Đây là lợi thế cốt lõi giúp chiến lược vượt trội so với các sản phẩm tương tự.

Quản lý rủi ro: Cơ chế bảo vệ tùy chọn nhưng khuyến nghị kích hoạt

Chiến lược mặc định tắt stop loss và take profit, nhưng cung cấp tùy chọn stop loss 1.5% và take profit 3.0%. Ngoài ra còn có cơ chế thoát lệnh theo tỷ lệ rủi ro/lợi nhuận, có thể thiết lập tỷ lệ rủi ro/lợi nhuận 1.5 lần. Khuyến nghị bật stop loss trong thị trường biến động cao, tắt take profit khi xu hướng rõ ràng để lợi nhuận chạy.

Cảnh báo rủi ro quan trọng: Chiến lược hoạt động kém trong thị trường dao động ngang, các phá vỡ giả liên tiếp có thể gây thua lỗ thường xuyên. Backtest lịch sử không đại diện cho lợi nhuận trong tương lai, hiệu suất khác nhau đáng kể trong các môi trường thị trường khác nhau. Khuyến nghị sử dụng kết hợp với bộ lọc xu hướng, kiểm soát chặt chẽ rủi ro mỗi lệnh không quá 2% tài khoản.

Ứng dụng thực tế: Khi nào nên dùng và khi nào nên tránh

Kịch bản ứng dụng tốt nhất: Thị trường xu hướng với biến động trung bình, đặc biệt là giai đoạn tiếp nối sau khi breakout khỏi mô hình tích lũy. Trong môi trường này, tỷ lệ thắng của chiến lược có thể đạt 65-70%, tỷ lệ lợi nhuận/rủi ro trung bình 1.8:1.

Kịch bản cần tránh: Thị trường đi ngang có biến động cực thấp và thị trường giảm hoảng loạn có biến động cực cao. Trường hợp đầu, tín hiệu hiếm và phần lớn là tín hiệu giả; trường hợp sau, stop loss thường xuyên bị kích hoạt. Khi ATR thấp hơn 50% hoặc cao hơn 200% so với trung bình 20 ngày, khuyến nghị tạm dừng chiến lược.

- 1