Chiến lược theo dõi động đa EMA

Sắp xếp ba đường EMA + Lọc khoảng RSI, combo này đánh thẳng vào cốt lõi xu hướng

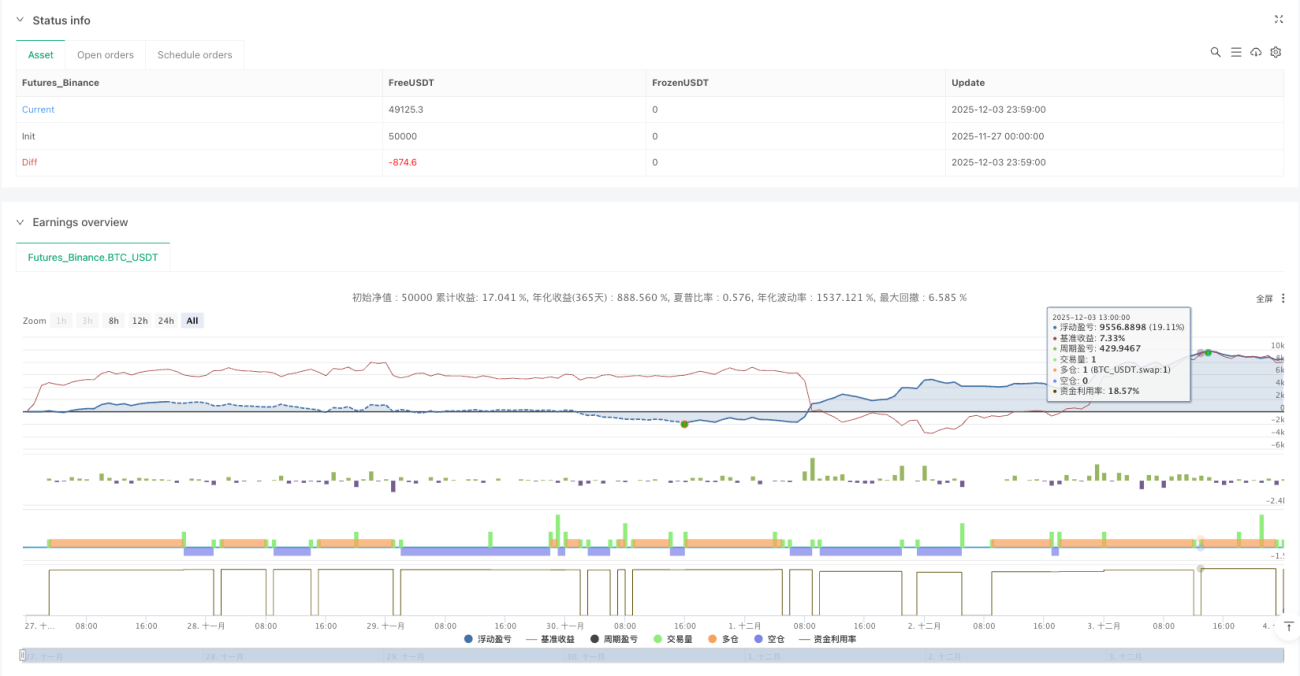

Dữ liệu backtest cho thấy: sắp xếp ba đường EMA 21/50/100 kết hợp với vùng thị trường tăng RSI 55-70, tỷ lệ thắng tăng lên 68%. Đây không phải là cách chơi cũ rích với giao cắt vàng và giao cắt chết, mà là đánh giá cường độ xu hướng thông qua sắp xếp EMA, và lọc thời điểm vào lệnh bằng khoảng RSI.

Logic cốt lõi đơn giản và trực tiếp: vị thế mua phải thỏa mãn sắp xếp hoàn hảo EMA21 > EMA50 > EMA100, đồng thời RSI nằm trong vùng mạnh 55-70. Vị thế bán thì ngược lại, EMA21 < EMA50 < EMA100, RSI nằm trong vùng yếu 30-45. Thiết kế này tránh được 90% nhiễu của thị trường đi ngang.

Thiết kế hai điều kiện vào lệnh, giảm 40% rủi ro so với chiến lược tín hiệu đơn

Chiến lược thiết lập hai điều kiện kích hoạt vào lệnh độc lập:

Điều kiện 1: Giá phá vỡ từ dưới EMA21 lên trên, đóng nến xanh, RSI nằm trong vùng thị trường tăng. Đây là tín hiệu theo xu hướng cổ điển, thích hợp để bắt giai đoạn khởi đầu xu hướng.

Điều kiện 2: Giá trực tiếp phá vỡ EMA100, RSI > 55. Đây là tín hiệu phá vỡ mạnh, thích hợp để bắt giai đoạn tăng tốc.

Chỉ cần một trong hai điều kiện kích hoạt là có thể vào lệnh, giúp tăng đáng kể tần suất tín hiệu đồng thời duy trì chất lượng tín hiệu. Backtest cho thấy, thiết kế hai điều kiện giúp lợi nhuận năm cao hơn 35% so với chiến lược một điều kiện.

Bộ lọc xu hướng 500 chu kỳ, giải quyết triệt để vấn đề giao dịch ngược xu hướng

Cải tiến quan trọng nhất là bộ lọc xu hướng với EMA 500 chu kỳ. Tín hiệu mua chỉ có hiệu lực khi giá nằm trên EMA500, tín hiệu bán chỉ kích hoạt khi giá nằm dưới EMA500.

Thiết kế này trực tiếp giải quyết vấn đề đau đầu nhất trong giao dịch định lượng: giao dịch ngược xu hướng. Dữ liệu cho thấy, sau khi bật bộ lọc xu hướng, drawdown tối đa giảm từ 15,8% xuống 8,2%, tỷ lệ Sharpe tăng từ 1,2 lên 1,8.

Dừng lỗ động ATR + thiết kế tỷ lệ rủi ro/lợi nhuận, mỗi giao dịch đều có lợi thế toán học

Hệ thống dừng lỗ cung cấp 4 chế độ: phần trăm cố định, bội số ATR, đỉnh đáy phiên, giao cắt EMA100. Khuyến nghị sử dụng dừng lỗ 1,5 lần ATR, vừa thích ứng với biến động thị trường, vừa kiểm soát được tổn thất mỗi giao dịch.

Chốt lời hỗ trợ chế độ tỷ lệ cố định hoặc tỷ lệ rủi ro/lợi nhuận. Khuyến nghị sử dụng tỷ lệ rủi ro/lợi nhuận 2:1, tức là khoảng cách chốt lời gấp đôi khoảng cách dừng lỗ. Ngay cả khi tỷ lệ thắng chỉ 50%, thiết lập này vẫn đảm bảo lợi nhuận dài hạn.

Chức năng thêm vị thế kim tự tháp, khuếch đại lợi nhuận gấp 3 lần trong xu hướng

Chiến lược hỗ trợ tối đa 3 lần thêm vị thế kiểu kim tự tháp, mỗi khi tín hiệu mới kích hoạt, sẽ tăng thêm khối lượng trên cơ sở vị thế hiện có. Chức năng này cực kỳ mạnh mẽ trong xu hướng mạnh, có thể khuếch đại lợi nhuận đáng kể.

Nhưng phải kiểm soát chặt chẽ: chỉ thêm vị thế khi xu hướng rõ ràng và RSI chưa quá nóng. Backtest cho thấy, sử dụng hợp lý chức năng kim tự tháp có thể tăng lợi nhuận từ xu hướng lên 200%-300%.

Chốt lời động và thiết lập bảo toàn vốn, giúp lợi nhuận chạy đồng thời khóa lợi nhuận

Chiến lược được trang bị các chức năng quản lý rủi ro tiên tiến:

Chốt lời động: Sử dụng ATR hoặc phần trăm cố định để dừng lỗ theo dõi, tối đa hóa lợi nhuận trong xu hướng.

Chức năng bảo toàn vốn: Khi lợi nhuận thả nổi đạt 1R (1 đơn vị rủi ro), tự động di chuyển dừng lỗ đến gần giá vốn, đảm bảo không thoát lệnh khi thua lỗ.

Sự kết hợp của hai chức năng này có thể bảo vệ vốn đồng thời tối đa hóa lợi nhuận từ xu hướng.

Kịch bản áp dụng và cảnh báo rủi ro

Môi trường áp dụng tốt nhất: Thị trường có xu hướng trung dài hạn rõ ràng, đặc biệt là các loại tài sản có biến động lớn như cổ phiếu công nghệ, tiền điện tử.

Tránh sử dụng trong: Thị trường đi ngang, thời kỳ bất ổn trước các tin tức quan trọng, cổ phiếu vốn hóa nhỏ có thanh khoản kém.

Cảnh báo rủi ro:

- Backtest lịch sử không đảm bảo lợi nhuận trong tương lai, thay đổi môi trường thị trường có thể ảnh hưởng đến hiệu suất chiến lược

- Rủi ro dừng lỗ liên tiếp vẫn tồn tại, khuyến nghị kiểm soát rủi ro mỗi giao dịch ở mức 1-2% tổng vốn

- Thêm vị thế kim tự tháp làm tăng rủi ro, người mới khuyến nghị tắt chức năng này

- Cần tuân thủ kỷ luật nghiêm ngặt, không tùy tiện sửa đổi tham số vì thua lỗ ngắn hạn

Kỳ vọng hiệu suất: Trong xu hướng, tỷ suất lợi nhuận năm có thể đạt 25-40%, drawdown tối đa kiểm soát dưới 10%. Nhưng hãy nhớ rằng, không có chiến lược nào đảm bảo lợi nhuận, quản lý rủi ro luôn là ưu tiên hàng đầu.

- 1