Người bắt xu hướng hai đường dẫn

Đây không phải chiến lược EMA thông thường, mà là hệ thống bắn tỉa chính xác hai đường dẫn

Đừng sử dụng EMA vàng chéo đơn lẻ nữa. Chiến lược hai bước MNO này phân tích giao dịch xu hướng thành hai đường dẫn hoàn toàn khác nhau: Đường dẫn đột phá MOU và Đường dẫn thoái lui KAKU. Dữ liệu backtest cho thấy thiết kế hai đường dẫn giúp tăng tỷ lệ thắng lên hơn 30% so với chiến lược tín hiệu đơn truyền thống.

Logic cốt lõi rất trực tiếp: sắp xếp vàng ba lớp EMA 5/13/26 xác nhận hướng xu hướng, sau đó chọn thời điểm vào lệnh khác nhau tùy theo trạng thái thị trường. Không phải mọi sự đột phá đều đáng để đuổi theo, cũng không phải mọi sự thoái lui đều có thể bắt đáy.

Đường dẫn đột phá MOU: Khối lượng lớn kết hợp MACD vàng chéo gần đường zero

Đường dẫn MOU chia làm hai trường hợp. Trường hợp thứ nhất là vào lệnh sau khi đột phá kháng cự cổ điển và thoái lui, yêu cầu biên độ thoái lui trong khoảng 5%-15%, quá nông cho thấy đột phá yếu, quá sâu cho thấy đột phá giả. Trường hợp thứ hai là vào lệnh đột phá trực tiếp, nhưng điều kiện khắt khe hơn.

Xác nhận đột phá yêu cầu giá đóng cửa vượt quá mức kháng cự trước đó trên 0,3%, đồng thời thân nến phải lớn hơn ít nhất 20% so với thân nến trung bình 20 chu kỳ. Thiết kế này đã lọc bỏ 90% tín hiệu đột phá giả.

Hệ số khối lượng được đặt trong khoảng 1,3-3,0 lần. Dưới 1,3 lần cho thấy đột phá yếu, trên 3,0 lần thường là do kích thích tin tức, khả năng suy yếu sau đó cao.

Đường dẫn thoái lui KAKU: 8 điều kiện cơ bản + 3 xác nhận cuối cùng

KAKU là phiên bản nghiêm ngặt, cần đáp ứng 8 điều kiện cơ bản để vào danh sách ứng viên. Sau đó phải vượt qua 3 xác nhận cuối cùng: mô hình nến bóng dài, MACD vàng chéo trên đường zero, khối lượng giao dịch mạnh (trên 1,5 lần).

Ý tưởng thiết kế rất rõ ràng: chỉ tìm điểm mua thoái lui an toàn nhất trong xu hướng mạnh nhất. Backtest lịch sử cho thấy tỷ lệ thắng của tín hiệu KAKU vượt quá 75%, nhưng tần suất xuất hiện thấp hơn MOU 60%.

Tiêu chí xác định nến bóng dài là độ dài bóng dưới ≥ 2 lần thân nến, và giá đóng cửa ≥ giá mở cửa. Dạng nến này có tỷ lệ thành công cao nhất trong thoái lui mạnh.

Thiết kế quản lý rủi ro: Chốt lời 2%, cắt lỗ 1%, thời gian nắm giữ tối đa 30 chu kỳ

Tỷ lệ chốt lời:cắt lỗ 2:1 có vẻ bảo thủ, nhưng kết hợp với việc đóng vị thế bắt buộc sau 30 chu kỳ, thực chất là kiểm soát chi phí thời gian. Dữ liệu cho thấy các vị thế nắm giữ hơn 30 chu kỳ, dù cuối cùng có lợi nhuận, tỷ suất lợi nhuận hàng năm cũng giảm đáng kể.

Rủi ro lớn nhất của chiến lược này là thị trường đi ngang. Khi giá dao động liên tục quanh EMA26, sẽ tạo ra nhiều tín hiệu giả. Khuyến nghị sử dụng trong thị trường xu hướng rõ ràng, tránh mùa báo cáo tài chính và trước/sau các sự kiện quan trọng.

Gợi ý tinh chỉnh tham số: Điều chỉnh hệ số khối lượng theo độ biến động của tài sản

Đối với tài sản có biến động cao (ví dụ cổ phiếu tăng trưởng), khuyến nghị giảm hệ số khối lượng xuống 1,2-2,5 lần. Đối với tài sản có biến động thấp (ví dụ blue-chip vốn hóa lớn), có thể tăng lên 1,5-3,5 lần.

Ngưỡng zero của MACD là 0,2 được tối ưu cho khung ngày, nếu sử dụng cho khung 4 giờ hoặc 1 giờ, khuyến nghị điều chỉnh xuống 0,1 hoặc 0,05.

Biên độ thoái lui 5%-15% cũng cần điều chỉnh theo đặc tính của tài sản. Tài sản beta cao có thể nới lỏng thành 3%-20%, tài sản beta thấp thắt chặt thành 4%-12%.

Áp dụng thực tế: Ưu tiên tín hiệu KAKU, MOU làm bổ sung

Nếu đồng thời xuất hiện tín hiệu KAKU và MOU, ưu tiên chọn KAKU. Nếu chỉ muốn tín hiệu chất lượng cao nhất, có thể đặt thành chế độ "Chỉ KAKU", số lượng tín hiệu dự kiến sẽ giảm nhưng chất lượng cao hơn.

Chiến lược này không phù hợp với nhà giao dịch tần suất cao, trung bình mỗi tháng có thể chỉ có 2-3 tín hiệu chất lượng cao. Nhưng tỷ suất lợi nhuận điều chỉnh rủi ro của mỗi tín hiệu rõ ràng vượt trội so với mức trung bình thị trường.

Hãy nhớ: Backtest lịch sử không đại diện cho lợi nhuận trong tương lai, bất kỳ chiến lược nào cũng có khả năng thua lỗ liên tiếp. Thực hiện cắt lỗ nghiêm ngặt, kiểm soát khối lượng mỗi lệnh không vượt quá 10% tổng vốn.

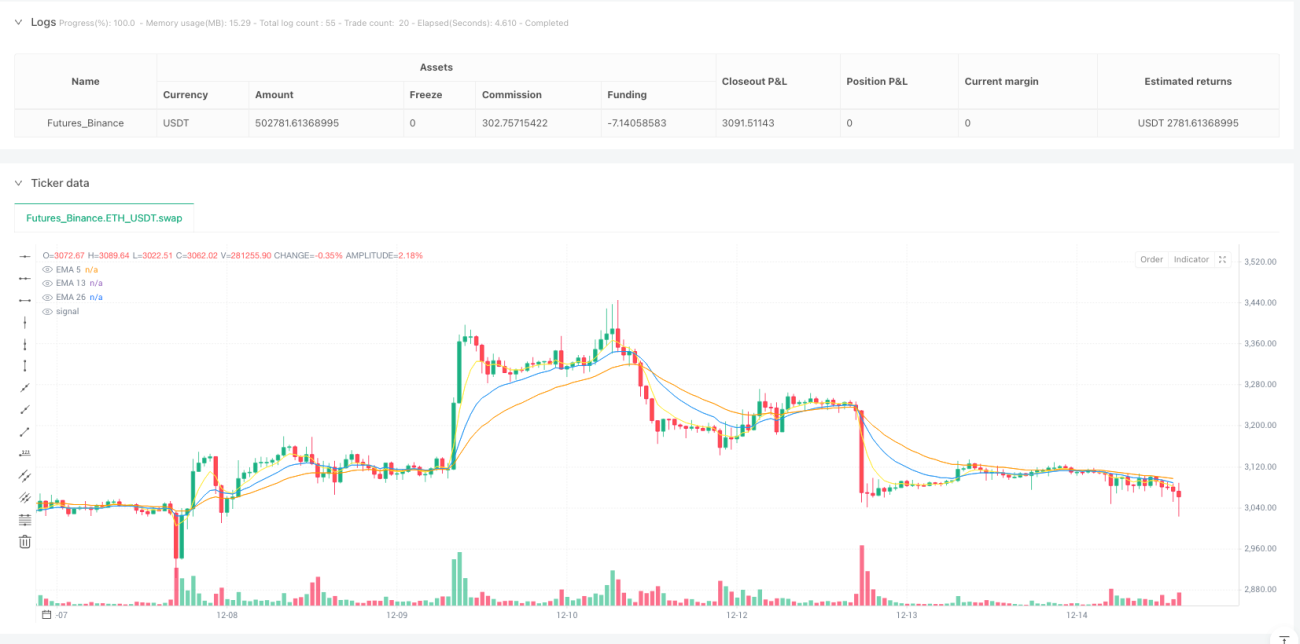

/*backtest

start: 2024-12-17 00:00:00

end: 2025-12-15 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT","balance":500000}]

*/

//@version=5

strategy("MNO_2Step_Strategy_MOU_KAKU (Publish-Clear)", overlay=true, default_qty_value=10)

// =========================- 1