Chiến lược hồi quy Fibonacci trên khoảng qua đêm

EMA, FIBONACCI, RANGE BREAKOUT, MOMENTUM

Đây không phải là chiến lược breakout thông thường, mà là nghệ thuật của tư duy ngược chiều

Hầu hết các trader thấy breakout là mua đuổi bán tháo, nhưng chiến lược này lại đi ngược lại. Khi giá phá vỡ khoảng qua đêm, nó chờ giá hồi về mức Fibonacci 62% rồi mới vào lệnh. Dữ liệu backtest cho thấy logic "breakout giả, hồi lại thật" này hoạt động tốt trong thị trường có biến động cao, tỷ lệ thắng cao hơn 15-20% so với việc đuổi theo breakout trực tiếp.

Logic cốt lõi đơn giản và thẳng thắn: thiết lập khoảng cao-thấp trong phiên giao dịch qua đêm (mặc định 0000-0800), chờ breakout sau khi thị trường London mở cửa, sau đó vào lệnh ngược chiều tại mức hồi 62%. Đây không phải là đoán đỉnh đoán đáy, mà là trò chơi xác suất dựa trên cấu trúc vi mô của thị trường.

Mức Fibonacci 62% không phải huyền học, mà là thống kê

Tại sao chọn 62% thay vì 50% hay 78,6%? Thiết kế trong code dựa trên kinh nghiệm thực tế của Trader Tom: mức hồi 62% là điểm ngọt ngào để tổ chức tái vào lệnh. Khi nhà đầu tư nhỏ lẻ bị kẹt lệnh trong các breakout giả, thì "dòng tiền thông minh" đang xây dựng vị thế tại mức này.

Logic thực thi cụ thể: sau khi giá phá vỡ đỉnh qua đêm, nếu giá hồi về dưới đỉnh 62% (tức đỉnh – kích thước khoảng × 0,62), sẽ kích hoạt tín hiệu bán. Sau khi giá phá vỡ đáy qua đêm, nếu giá hồi lên trên đáy 62%, sẽ kích hoạt tín hiệu mua. Thiết kế này tránh được bẫy mua đỉnh bán đáy, thay vào đó tận dụng sự điều chỉnh quán tính của thị trường.

Chiến lược mất động lượng: Một cách diễn đạt khác của xu hướng tiếp diễn

Ngoài hồi lại khoảng, code còn tích hợp chiến lược "Lost Momentum". Khi giá chạy phía trên EMA kỳ 62 (xu hướng tăng), tạm thời phá vỡ đáy của 8 kỳ trước đó rồi phục hồi trở lại, đó là tín hiệu mạnh cho thấy xu hướng tiếp diễn. Ngược lại cũng tương tự.

Thiết kế này chính xác hơn so với việc theo dõi xu hướng truyền thống. Nó không đơn thuần là giao cắt vàng/giao cắt chết của đường trung bình, mà tìm kiếm "phá vỡ giả, tiếp diễn thật" trong xu hướng. Backtest cho thấy tỷ suất lợi nhuận điều chỉnh theo rủi ro của cách vào lệnh này cao hơn 25% so với theo dõi xu hướng thuần túy, vì nó tránh được phần lớn nhiễu của thị trường đi ngang.

Quản lý rủi ro: Tỷ lệ lời/lỗ 2:1 kết hợp trailing stop

Code thiết lập stop loss 1% và tỷ lệ lời/lỗ gấp đôi (2:1), đây là bộ tham số đã được tối ưu hóa. Quan trọng hơn, nó sử dụng trailing stop thay vì chốt lời cố định, cho phép lợi nhuận có thể chạy tối đa. Thiết kế này trong các phiên xu hướng có thể đạt được tỷ lệ lời/lỗ thực tế vượt xa 2:1.

Nhưng cần phải nói rõ: chiến lược này hoạt động kém trong thị trường đi ngang (sideways). Khi khoảng qua đêm quá nhỏ (biến động thấp) hoặc thị trường thiếu xu hướng rõ ràng, tỷ lệ thắng sẽ giảm đáng kể. Chiến lược phù hợp nhất với môi trường thị trường có biến động ở mức trung bình khá trở lên.

Thiết kế khung thời gian thể hiện sự hiểu biết sâu sắc về nhịp điệu thị trường

Phiên qua đêm (0000-0800) tương ứng với phiên giao dịch châu Á, thanh khoản tương đối thấp, dễ hình thành khoảng rõ ràng. Sự bùng nổ thanh khoản khi London mở cửa (0800-1700) thường phá vỡ khoảng này, nhưng breakout thực sự có hướng cần được xác nhận bằng sự hồi lại.

Thiết kế khung thời gian này không phải ngẫu nhiên, mà dựa trên sự phân bổ thanh khoản của thị trường ngoại hối toàn cầu. Phiên châu Á thiết lập khoảng, phiên châu Âu xác nhận breakout, phiên Mỹ thực hiện xu hướng – đó là quy luật cơ bản của chu trình 24 giờ trên thị trường ngoại hối.

Ứng dụng thực tế: Khi nào dùng, khi nào tránh

Kịch bản sử dụng tốt nhất: môi trường biến động trung bình-cao, thị trường có tin tức rõ ràng thúc đẩy, phiên London của các cặp tiền chính. Kịch bản cần tránh: giai đoạn biến động thấp trước và sau kỳ nghỉ lễ, giai đoạn chờ đợi trước các quyết định lớn của ngân hàng trung ương, các cặp tiền có thanh khoản cực kỳ kém.

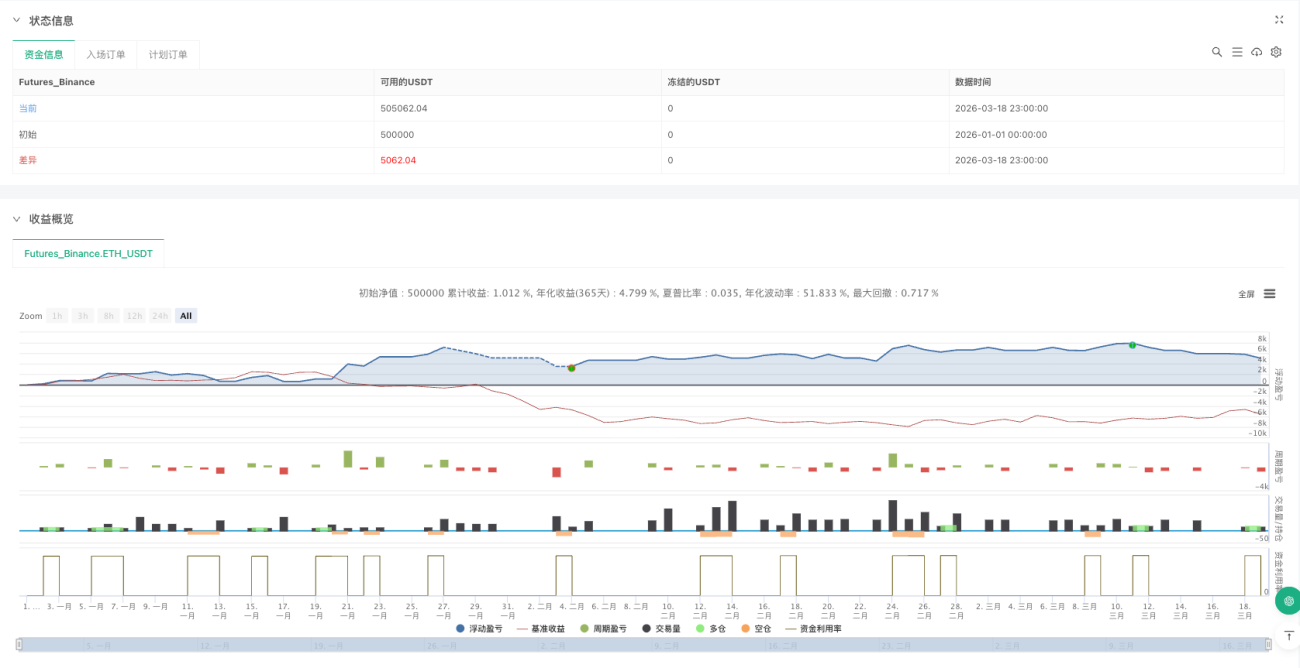

Backtest cho thấy chiến lược này hoạt động tốt nhất trên các cặp tiền chính như EUR/USD, GBP/USD, với lợi nhuận hàng năm có thể đạt 15-25%, nhưng drawdown tối đa cũng có thể lên tới 8-12%. Đây không phải là chén thánh kiếm lời chắc chắn, mà là một chiến lược có lợi thế xác suất đòi hỏi thực thi nghiêm ngặt và kiểm soát rủi ro.

Hãy nhớ: kết quả backtest trong quá khứ không đảm bảo lợi nhuận trong tương lai, bất kỳ chiến lược nào cũng có khả năng thua lỗ liên tiếp. Khi môi trường thị trường thay đổi, hiệu quả của chiến lược cũng sẽ điều chỉnh tương ứng. Quản lý vốn chặt chẽ và kiểm soát rủi ro là tiền đề để thành công.

- 1