21

Follow

122

Followers

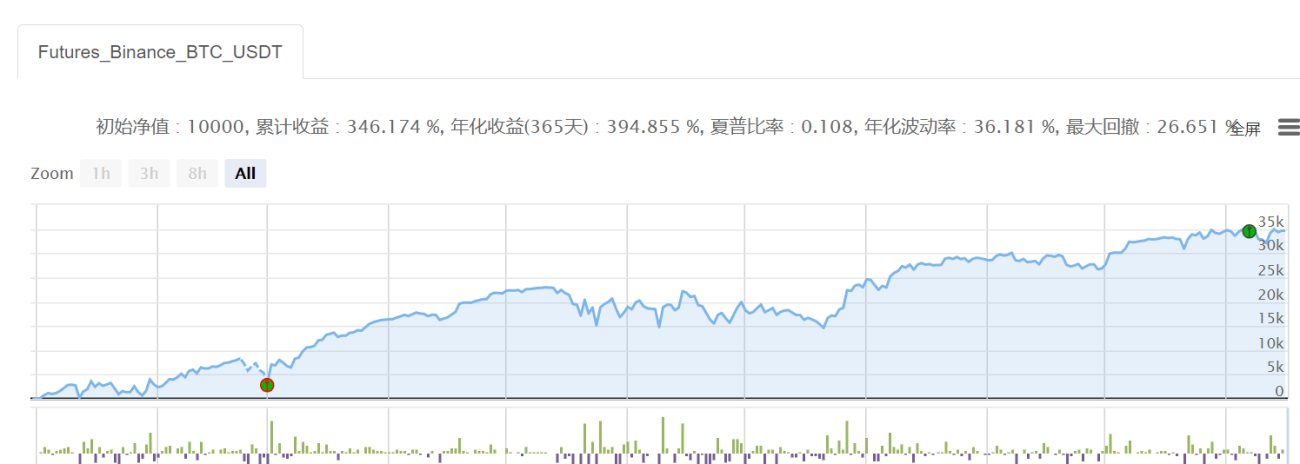

参数非常简单,以BTC为例,到了开多的区域平空买底仓开多,到了开空的区域平多买底仓开空,反复轮回

显然,在币圈,从长期来看,任何复杂模型都跑不过无脑网格

财富密码是无脑网格+无脑梭哈土狗

希望和最早的马丁一样,都是最为简单粗暴但是赚钱的策略

Source

Python

'''backtest

start: 2021-01-01 00:00:00

end: 2021-11-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":2500}]

args: [["H",30],["n1",0.001],["grid",300],["xia",50000]]

'''

def CancelPendingOrders():

orders = _C(exchanges[0].GetOrders)

if len(orders)>0:

for j in range(len(orders)):

exchanges[0].CancelOrder(orders[j].Id, orders[j])

j=j+1

def main():

exchange.SetContractType('swap')

exchange.SetMarginLevel(M)

currency=exchange.GetCurrency()

if _G('buyp') and _G('sellp'):

buyp=_G('buyp')

sellp=_G('sellp')

Log('读取网格价格')

else:

ticker=exchange.GetTicker()

buyp=ticker["Last"]-grid

sellp=ticker["Last"]+grid

_G('buyp',buyp)

_G('sellp',sellp)

Log('网格数据初始化')

while True:

account=exchange.GetAccount()

ticker=exchange.GetTicker()

position=exchange.GetPosition()

orders=exchange.GetOrders()

if len(position)==0:

if ticker["Last"]>shang:

exchange.SetDirection('sell')

exchange.Sell(-1,n1*H)

Log(currency,'到达开空区域,买入空头底仓')

else:

exchange.SetDirection('buy')

exchange.Buy(-1,n1*H)

Log(currency,'到达开多区域,买入多头底仓')

if len(position)==1:

if position[0]["Type"]==1:

if ticker["Last"]<xia:

Log(currency,'空单全部止盈反手')

exchange.SetDirection('closesell')

exchange.Buy(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('sell')

exchange.Sell(sellp,n1)

exchange.SetDirection('closesell')

exchange.Buy(buyp,n1)

if len(orders)==1:

if orders[0]["Type"]==1: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

if orders[0]["Type"]==0:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if position[0]["Type"]==0:

if ticker["Last"]>float(shang):

Log(currency,'多单全部止盈反手')

exchange.SetDirection('closebuy')

exchange.Sell(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('buy')

exchange.Buy(buyp,n1)

exchange.SetDirection('closebuy')

exchange.Sell(sellp,n1)

if len(orders)==1:

if orders[0]["Type"]==0: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if orders[0]["Type"]==1:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

Strategy parameters

Related strategies

Comment

All comments (5)

- 1