RSI Rising Crypto Trending Strategy

Overview

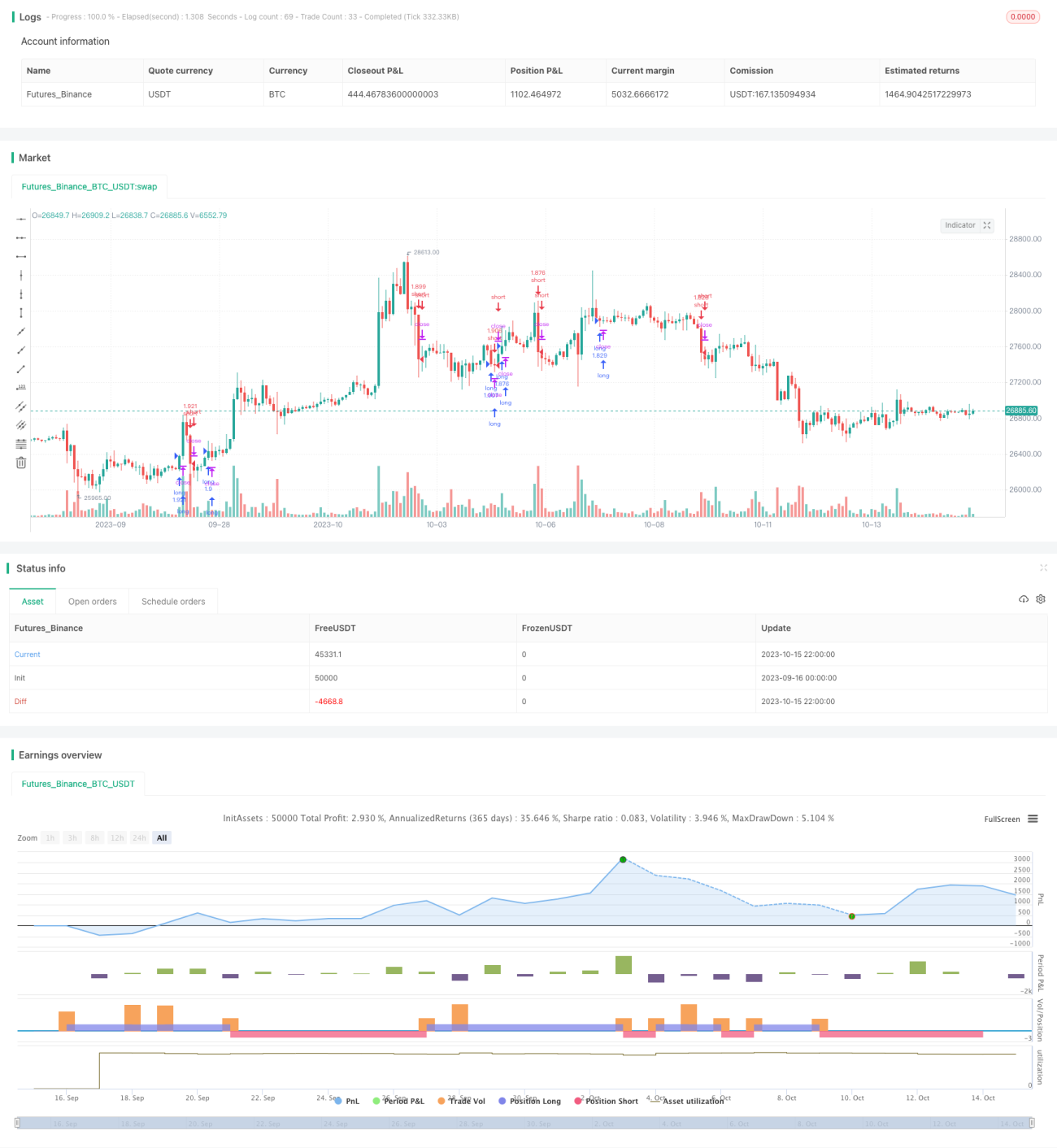

The RSI Rising Crypto Trending Strategy is a trend trading strategy designed for longer timeframes (4h+) in crypto and stock markets.

It utilizes RSI to identify rising and falling trends combined with Bollinger Bands and ROC to avoid trading in sideways markets. From tests, it appears to work better trading crypto against crypto rather than against fiat.

Strategy Logic

The strategy uses the following indicators:

- RSI - To identify rising/falling trends

- Bollinger Bands - To identify sideways markets

- ROC - To confirm trend direction

The specific trading rules are:

Entry Rules

Long entry: RSI rising AND not sideways market per BB and ROC

Short entry: RSI falling AND not sideways market per BB and ROC

Exit Rules

Exit when opposite signal is triggered

Advantage Analysis

- Captures trend turning points early using RSI

- Avoids getting trapped in sideways markets using BB

- ROC confirms trend direction for more robust signals

- Good for longer timeframe trades and capturing trends

- Better for crypto/crypto pairs to avoid fiat exposure

Risk Analysis

- No stop loss so high risk of large losses

- Poor BB and ROC parameters could lead to missed trades or bad signals

- Purely technical so misses major black swan events

Increase stop loss, optimize BB/ROC parameters, and incorporate fundamental analysis.

Enhancement Opportunities

Some ways this strategy could be improved:

-

Add stop loss for risk management and setting maximum loss per trade.

-

Optimize BB and ROC parameters through backtesting to find best settings.

-

Incorporate additional indicators like MACD, KD for multi-indicator signal reliability.

-

Build a liquidity model to pause trading during volatility spikes to avoid traps.

-

Use machine learning to automatically optimize parameters and signal weighting.

-

Incorporate on-chain data like exchange liquidity and fund flows for greater adaptability.

Summary

The RSI Rising Crypto Trend Strategy captures longer timeframe crypto trends using RSI plus BB and ROC. The advantage is quickly catching trend reversals and avoiding traps. The weaknesses are no stop loss and parameter dependency. Enhancements like stop loss, optimization, machine learning can make it more robust.

- 1