Multi-indicator Decision Based Short Term Trend Strategy

Overview

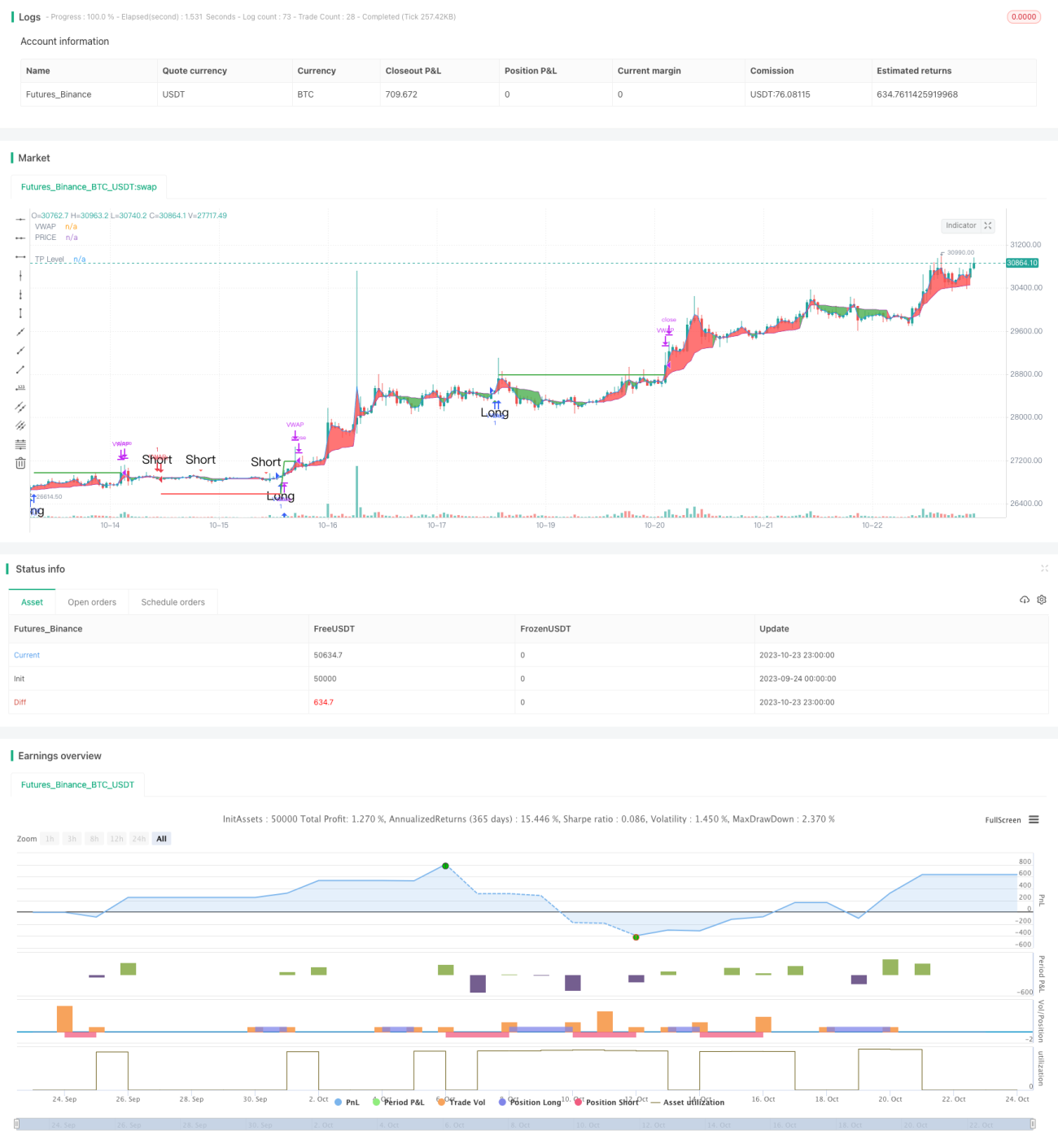

This strategy incorporates three technical indicators across different dimensions, including support/resistance levels, moving average system, and oscillator indicators, to determine short-term trend direction for higher win rate.

Strategy Logic

The code first calculates the support/resistance levels of the price, including the standard pivot points and Fibonacci retracement levels, and plots them on the chart. Breaking these key levels signals important trend signals.

Then it calculates the Volume Weighted Average Price (VWAP) and Average Price for golden cross and death cross signals. This belongs to medium-long term trend judgment.

Finally it calculates the Stochastic RSI oscillator for overbought and oversold signals. This belongs to the overbought/oversold indicator.

By combining signals across these three dimensions, if the support/resistance, VWAP, and Stochastic RSI all give buy signals, it will open long position. If all give sell signals, it will open short position.

Advantage Analysis

The biggest advantage of this strategy is the combination of indicators across different dimensions, making the judgment more comprehensive and accurate with higher win rate. First the support/resistance levels define the major trend. Then VWAP determines the medium-long term trend. Finally the Stochastic RSI judges the overbought/oversold condition. With all three indicators firing at the same time, it can effectively filter out false signals and improve entry accuracy.

In addition, the take profit function helps lock in certain percentage of profits, aiding risk management.

Risk Analysis

The main risk of this strategy is its reliance on simultaneous signals from all indicators for decision making. If some indicators give out faulty signals, it may lead to wrong decisions. For example, when Stochastic RSI shows overbought but VWAP and support/resistance still indicate bullish, it may miss the buying opportunity by not entering.

Also, improper parameter tuning of the indicators could lead to wrong signal judgments that requires iterative backtesting for optimization.

Additionally, black swan events in the short-term market may invalidate signals from the indicators. To guard against this risk, stop loss strategies could be implemented to limit downside on individual trades.

Improvement Opportunities

The strategy can be further improved in the following aspects:

-

Incorporate more indicator signals like volume to gauge trend strength for better accuracy.

-

Add machine learning models to train on the multidimensional indicators and automatically discover optimal strategies.

-

Optimize parameters based on different products for adaptive tuning.

-

Introduce stop loss and position sizing based on drawdown to better control risks.

-

Perform portfolio optimization to find low-correlation products for diversity.

Conclusion

Overall this strategy is well suited for short-term trend trading. By combining signals across dimensions, it can filter out significant noise for higher win rate. But risks of erroneous signals remain that can be improved on through further enhancements. With continued optimization, this strategy has the potential to become an efficient and robust short-term system.

- 1