Gap Trading Moving Average Strategy

This article provides an in-depth analysis of the moving average gap trading strategy coded by Noro. The strategy identifies trend reversals by calculating the deviation between closing price and simple moving average, and achieves buy low and sell high.

Strategy Logic

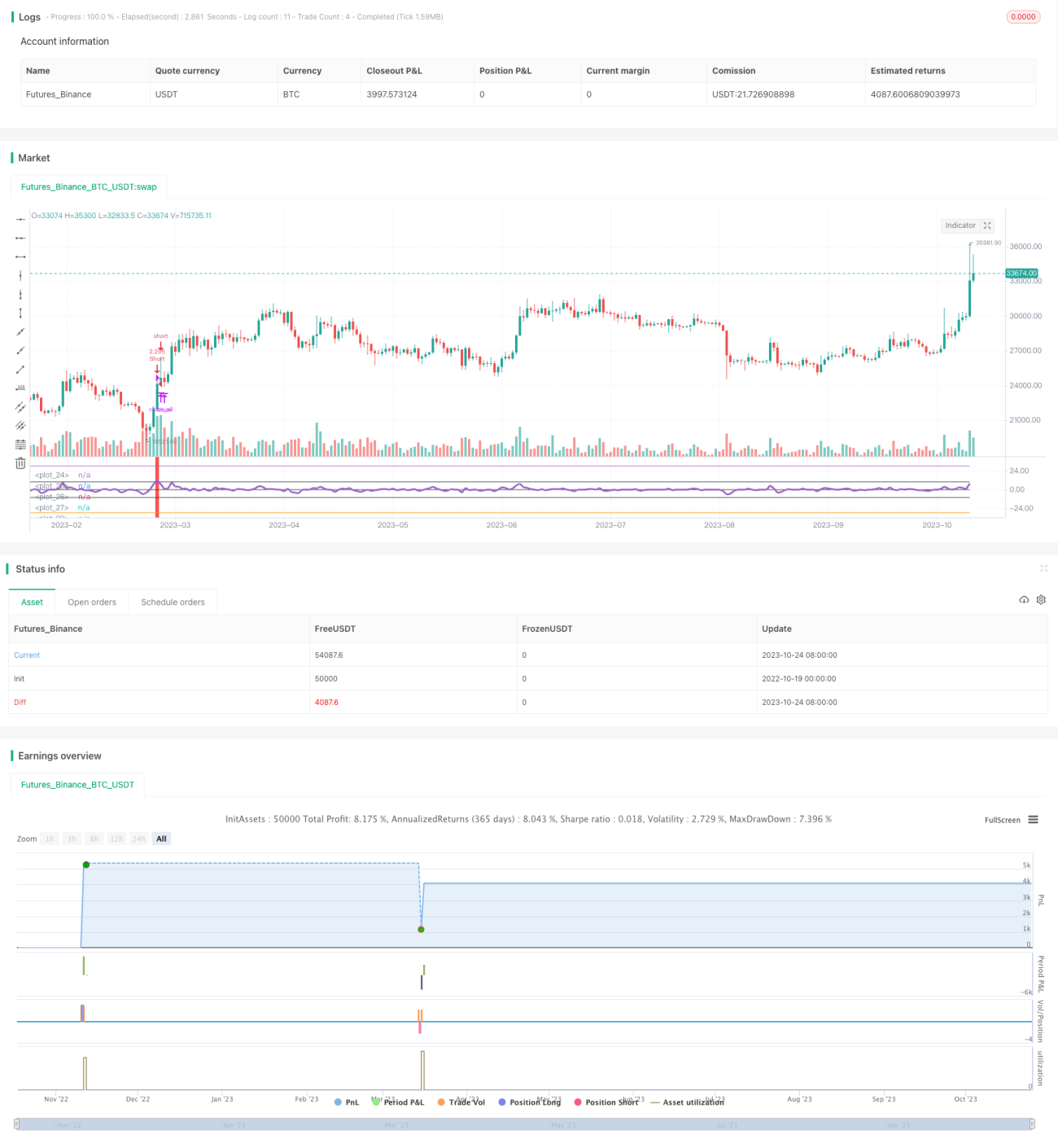

The strategy first calculates the 3-day simple moving average (SMA). Then it computes the ratio of closing price (close) to SMA minus one as an indicator (ind). When ind crosses above the preset parameter limit, it means the closing price has surpassed SMA significantly and long position is considered. When ind crosses below -limit, it means the closing price has fallen far below SMA and short position is considered.

The strategy also plots the 0 axis, limit axis and -limit axis. The ind indicator is colored differently in separate areas to assist judgement. When ind crosses over limit or -limit, it signals long or short entry.

Upon long/short signal, the strategy will close opposite position first, then open long/short position. When ind returns between 0 axes, all positions will be closed.

Advantages

-

Adopting gap trading principle to catch trend reversals, unlike trend following strategies.

-

Plotting indicator axes for intuitive judgment of indicator position and crossover.

-

Optimized close logic, closing existing position before reversing direction. Avoid unnecessary opposite positions.

-

Defined trading time range to avoid unnecessary overnight positions.

-

Flexibility to enable/disable long/short trading.

Risks

-

Moving average strategies tend to generate multiple losing trades, requiring patience in holding.

-

Moving averages lack flexibility in capturing real-time price changes.

-

Preset limit parameter is static, requiring adjustments for different products and market environments.

-

Unable to identify fluctuations within trends, requiring combining with volatility indicators.

-

Need to optimize holding rules e.g. stop loss, take profit; or only catch initial gaps.

Enhancement Directions

-

Test different parameter settings e.g. SMA period, or adaptive moving averages like EMA.

-

Add moving average direction and slope validation to avoid meaningless trades.

-

Consider combining with volatility indicators like Bollinger Bands to pause trading when volatility rises.

-

Implement position sizing rules e.g. fixed quantity, incremental pyramiding, money management.

-

Set stop loss/take profit lines, or pause new orders when fixed percentage stop loss triggered, to control per trade risk.

Summary

This article comprehensively analyzed Noro's moving average gap trading strategy. It utilizes the price gap from moving average feature and implements indicator axes and colors for entry timing. It also optimizes the close logic and defines trading time range. However, inherent weaknesses of moving average tracking remains, requiring further optimizations in parameters, stop loss rules, combining indicators etc. to improve robustness.

- 1