RSI Momentum Long Short Strategy

Overview

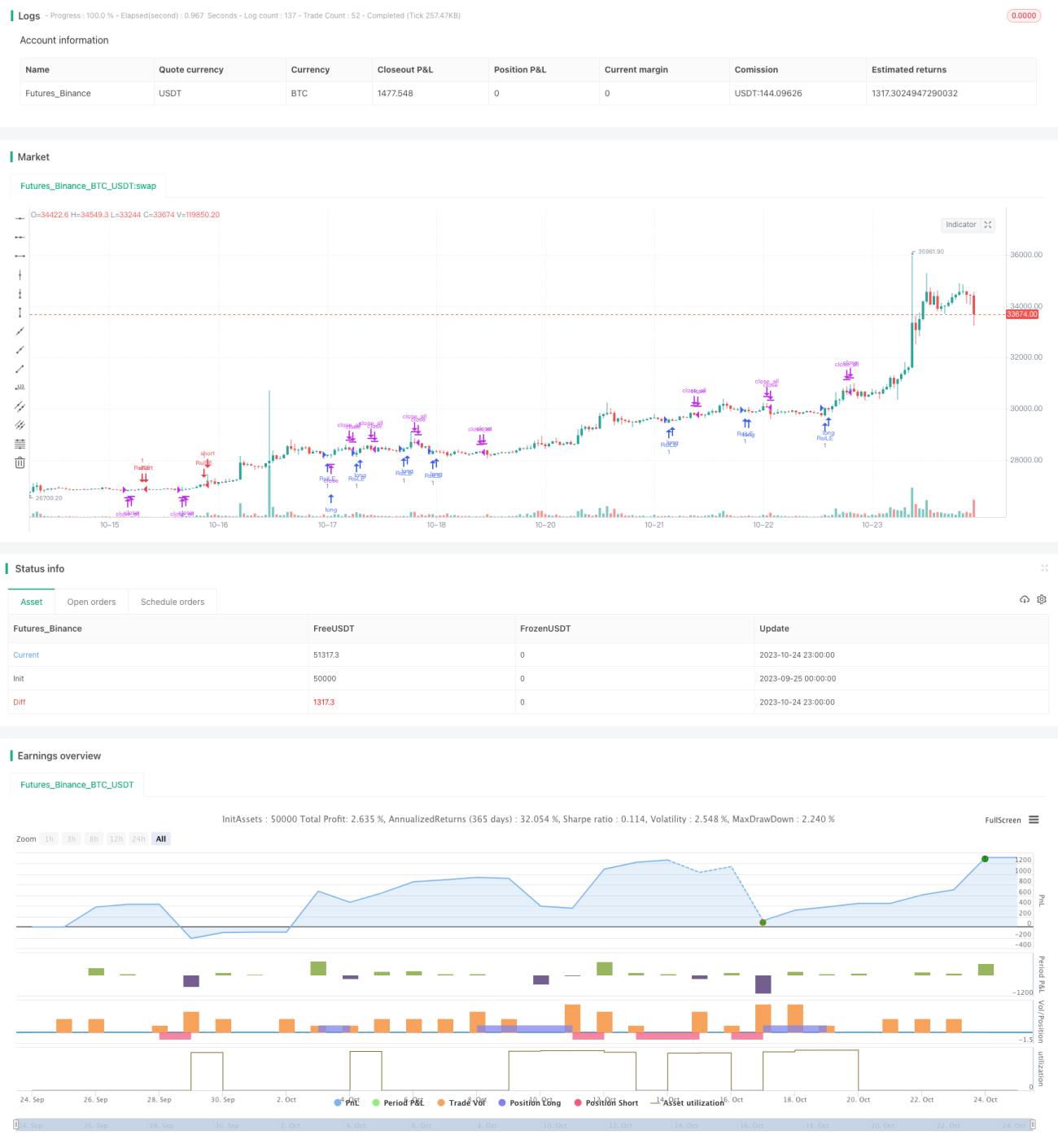

The RSI Momentum Long Short strategy is a typical momentum strategy based on the Larry Connors RSI indicator, using the overbought and oversold signals from RSI to determine entries and exits. The key is to identify whether the price is in overbought or oversold status and use that as trading signals.

Strategy Logic

The strategy constructs RSI indicator by calculating the upside momentum and downside momentum of prices over a lookback period. RSI below oversold line 10 is considered oversold, while RSI above overbought line 90 is considered overbought. The strategy generates long signals when RSI crosses oversold line from below, and generates short signals when RSI crosses overbought line from above.

Additional moving average filters are added - only allowing long signals when 5day MA is above 200day MA, and short signals when 5day MA is below 200day MA. This helps filter out false signals from short-term rebounds.

Profit taking mechanisms are also introduced. Existing long positions will be closed out when RSI crosses above overbought line 90. Existing short positions will be closed out when RSI crosses below oversold line 10. This locks in profits and avoids increasing losses.

Advantages of the Strategy

-

Using RSI to identify overbought/oversold levels catches price reversal moments.

-

Adding MA filters reduces false signals from short-term noise.

-

Profit-taking mechanics help control risks and limit losses.

-

Simple and clear rules, easy to understand and implement.

-

RSI is a widely used and practical indicator, suitable for many instruments.

Risks of the Strategy

-

RSI overbought/oversold may not always result in reversal.

-

MA filters could also filter out good trading opportunities.

-

Improper profit-taking settings give up trends too early.

-

Parameters like RSI lookback, overbought/oversold levels, MA settings need tuning.

Risks can be reduced via parameter optimization, combining other indicators, flexible profit-taking, etc.

Enhancement Opportunities

-

Test RSI with different lookback periods.

-

Add other indicators like KDJ, MACD to supplement RSI.

-

Adjust overbought/oversold levels based on market regimes.

-

Fine tune profit-taking RSI levels based on holding period.

-

Incorporate stop loss strategies based on max loss percentage.

-

Optimize MA system, use dynamic trailing stop loss.

Conclusion

The RSI Momentum Long Short Strategy catches short-term reversal opportunities by using RSI to identify overbought/oversold levels, filtered by MAs and profit-taking rules. The strategy is simple and practical, worth further testing and enhancement to adapt to diverse markets. Overall it provides a good framework that can serve as a reference for quantitative trading strategy development.

/*backtest

start: 2023-09-25 00:00:00

end: 2023-10-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//authour: SudeepBisht

//@version=3

//Based on Larry Connors RSI-2 Strategy - Lower RSI

strategy("SB_CM_RSI_2_Strategy_Version 2.0", overlay=true)- 1