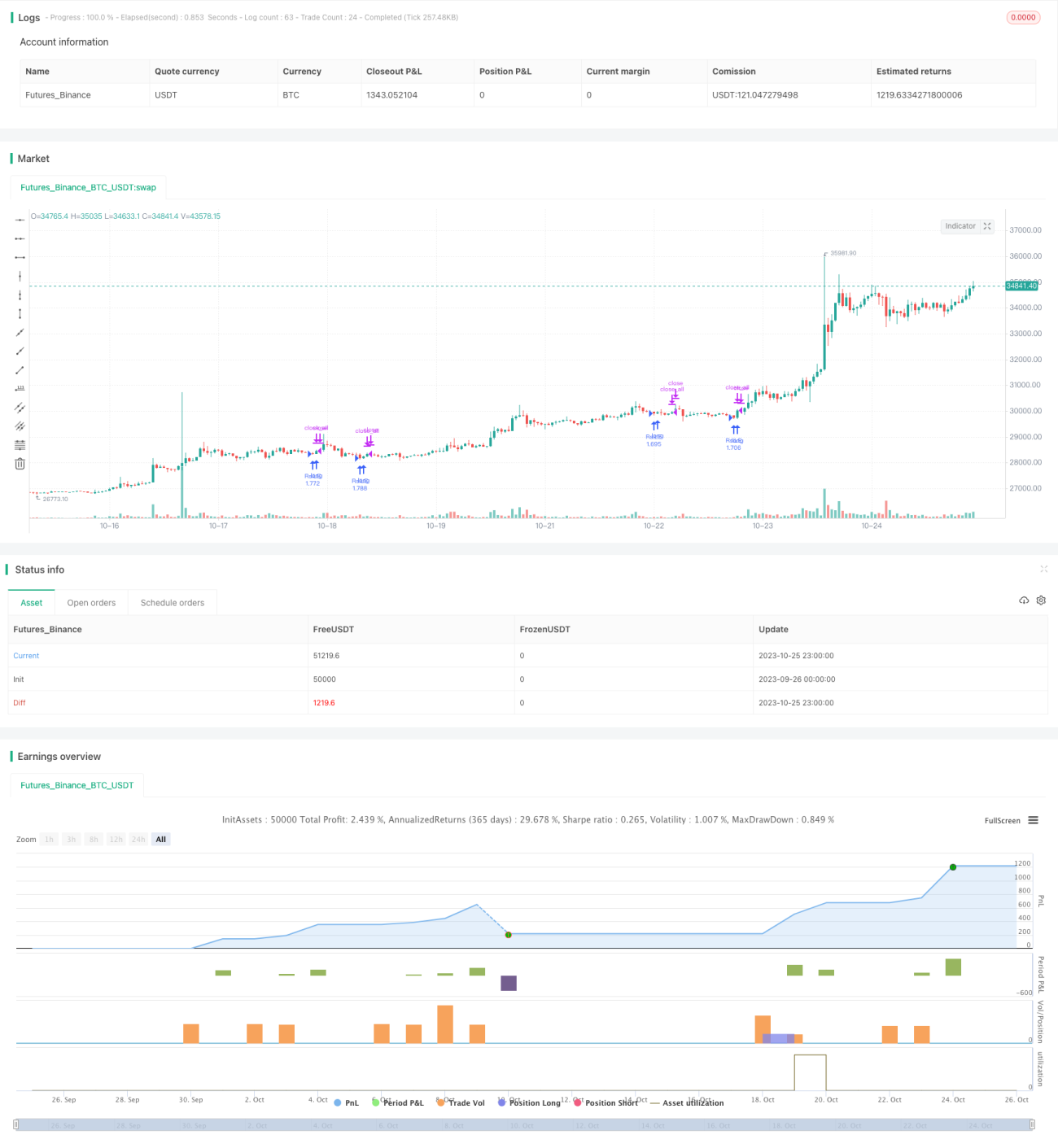

Oscillation Breakthrough Strategy

Overview

This strategy is based on the classic idea of Larry Connors, using double moving average system to capture the medium-term oscillation of the market and take profit when it is overbought or oversold.

Strategy Logic

-

Use 2-period RSI to determine if the price is in oversold region.

-

Use long period moving average (200 periods) to determine the major trend direction. Only consider opening position when price is above the long MA.

-

When price is above long MA and RSI is below oversold line, open long position at market price.

-

When price breaks through short period MA (5 periods) upwards, close long position at market price to take profit.

In addition, the strategy provides the following configurable options:

-

RSI parameters: period length, overbought/oversold levels.

-

MA parameters: long and short period.

-

RSI MA filter: add RSI MA to avoid RSI fluctuation.

-

Stop loss: configurable to add stop loss or not.

Advantage Analysis

-

The double MA system can effectively track medium-long term trends.

-

RSI avoids missing the best entry timing during violent fluctuation.

-

Flexible configuration suitable for parameter optimization.

-

Breakthrough strategy, not likely to miss signals.

Risk Analysis

-

Double MA strategy is sensitive to parameters, requiring optimization to achieve best performance.

-

No stop loss brings risk of expanding losses. Cautious position sizing is needed.

-

False breakout risks losses in oscillating market. Consider optimizing MA periods or adding other filters.

-

Backtest overfitting risk. Requires validation across markets and time periods.

Optimization Directions

-

Test and optimize combinations of RSI and MA parameters to find optimum.

-

Test additional entry filters like volume spike to reduce false signals.

-

Add trailing stop loss to control single trade loss. Assess impact on overall profitability.

-

Evaluate impact of different holding periods to find optimal.

-

Test robustness in longer timeframes like daily.

Summary

This strategy combines double MA trend tracking and RSI overbought/oversold to form a typical breakout system. With parameter optimization, strict risk management and robustness validation, it can become a powerful quantitative trading tool. But traders should beware of backtest overfitting and keep improving the strategy to adapt to changing market conditions.

- 1