Momentum Reversal Combo Strategy

Overview

This strategy combines two momentum indicators to uncover more trading opportunities. The first indicator is a stochastic oscillator reversal strategy proposed in Ulf Jensen's book. The second indicator is John Ehlers' detrended synthetic price. The strategy takes positions when both indicators give concurring buy or sell signals.

Strategy Logic

The logic behind the stochastic oscillator reversal is: go long when close is lower than previous close for 2 straight days and fast line is above slow line; go short when close is higher than previous close for 2 straight days and fast line is below slow line.

The detrended synthetic price (DSP) is calculated as:

DSP = EMA(HL/2, 0.25 cycle) - EMA(HL/2, 0.5 cycle)

where HL/2 is the midpoint of high and low, 0.25 cycle EMA represents short-term trend and 0.5 cycle EMA represents long-term trend. DSP shows the price deviation from its dominant cycle. Buy when DSP crosses above threshold and sell when crossing below.

This strategy combines the signals from both indicators. It only enters positions when both indicators give concurring signals.

Advantage Analysis

- Filtering uncertain signals with two indicators reduces wrong trades

- Validation between indicators enhances signal reliability

- Stochastic reversal catches short-term reversal opportunities

- DSP identifies medium to long term trends

- Combining two indicators provides flexibility to catch reversals and follow trends

Risk Analysis

- Stochastic performs poorly in ranging markets

- DSP may give wrong signals near trend turning points

- Missing some opportunities by only trading on concurring signals

- Needs proper parameter tuning to achieve combinatorial effect

Enhancement Directions

- Test different parameters to optimize indicator performance

- Try different indicator weighting, e.g. delay DSP signals

- Add stop loss to control risks

- Incorporate more indicators to build multi-factor model

Conclusion

The strategy combines two different momentum indicators and improves signal quality through double filtering while maintaining trade frequency and controlling risks. But the limitations of the individual indicators need to be noted and parameters properly tuned. With continuous optimizations, the strategy has the potential to generate alpha over the broad market.

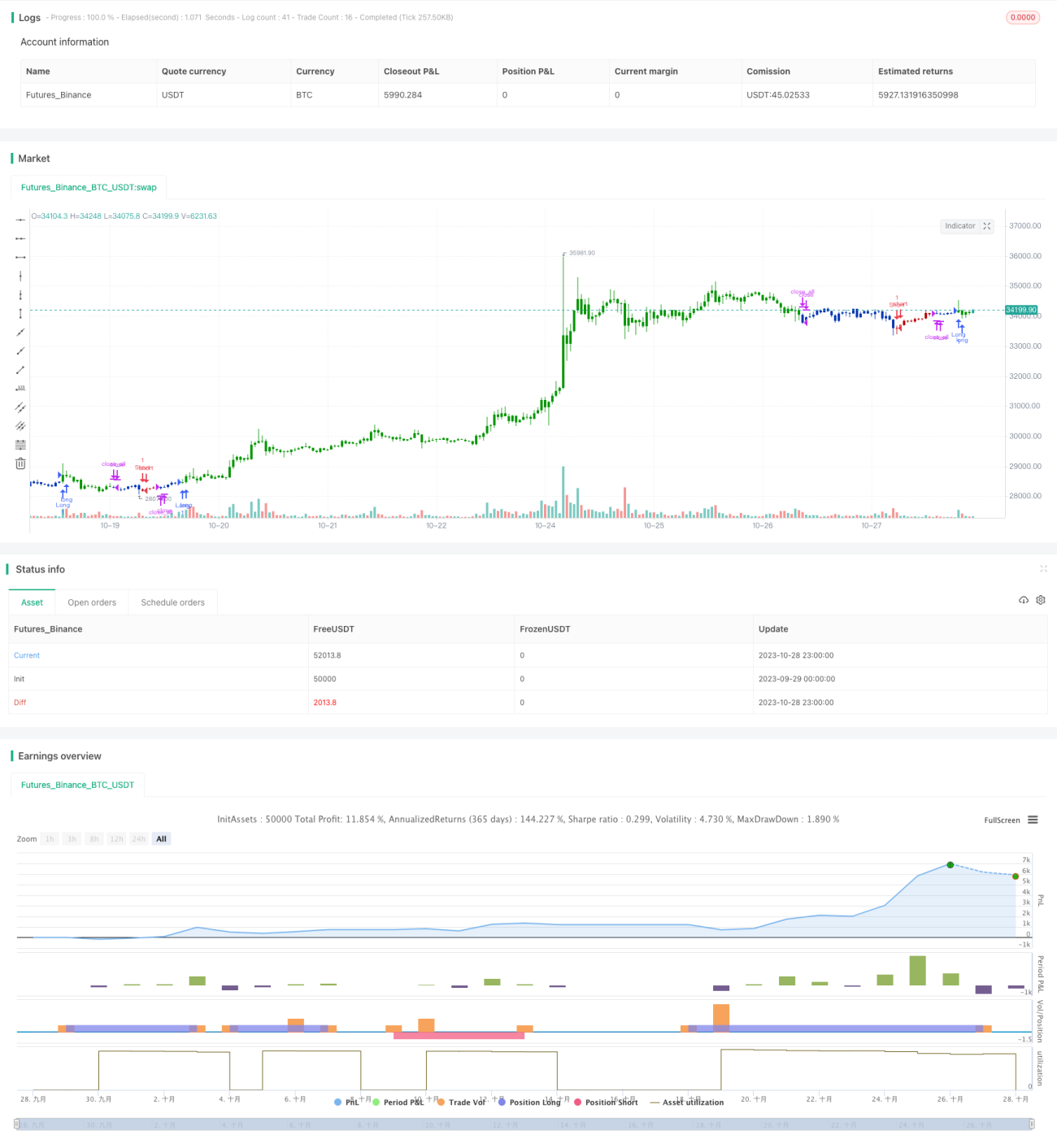

/*backtest

start: 2023-09-29 00:00:00

end: 2023-10-29 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/11/2019

// This is combo strategies for get a cumulative signal. - 1