Ichimoku Kinko Hyo Cross Strategy

Overview

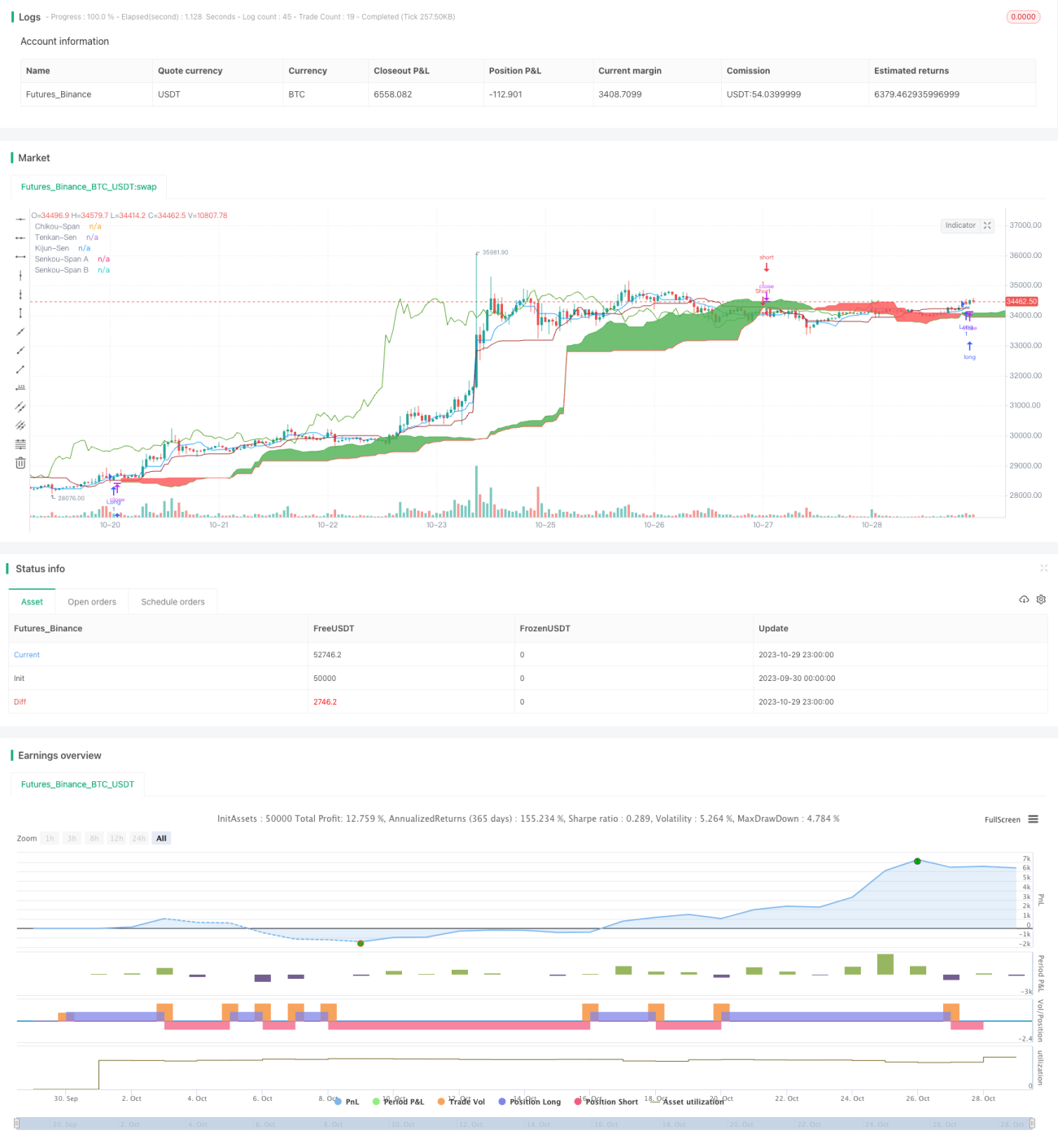

The Ichimoku Kinko Hyo Cross strategy generates trading signals by observing the crossovers between Tenkan-Sen and Kijun-Sen lines of the Ichimoku system, combined with the price level versus the Cloud. This strategy incorporates both trend following and reversal trading, making it a versatile and practical trading strategy.

Strategy Logic

-

Calculate the Ichimoku components:

-

Tenkan-Sen: Midpoint of last 9 bars

-

Kijun-Sen: Midpoint of last 26 bars

-

Senkou Span A: Average of Tenkan-Sen and Kijun-Sen

-

Senkou Span B: Midpoint of last 52 bars

-

-

Observe the combination of following trading signals:

-

Crossover between Tenkan-Sen and Kijun-Sen (Golden Cross and Death Cross)

-

Close price above or below the Cloud (Senkou Span A and B)

-

Chikou Span compared to close price 26 bars ago

-

-

Entry signals:

-

Long: Tenkan-Sen crosses above Kijun-Sen (Golden Cross) and close above Cloud and Chikou Span above close 26 bars ago

-

Short: Tenkan-Sen crosses below Kijun-Sen (Death Cross) and close below Cloud and Chikou Span below close 26 bars ago

-

-

Exit signals when opposite signal occurs.

Advantages

-

Combines trend following and reversal trading.

-

Crossovers ensure signal reliability and avoid false breakouts.

-

Multiple signal confirmation filters out market noise.

-

Chikou Span avoids whipsaws.

-

Cloud provides support and resistance for entries and exits.

Risks

-

Improper parameters may cause overtrading or unclear signals.

-

Trend reversals can lead to large losses.

-

Fewer trading opportunities during range-bound markets.

-

Delayed entry signals if Cloud is too wide.

-

High signal complexity increases implementation difficulty.

Risks can be mitigated through parameter optimization, position sizing, stop losses, liquid products, etc.

Enhancements

-

Optimize moving average periods for ideal frequency and profitability.

-

Add trend filter to avoid trend reversal losses.

-

Add volatility filter to control risk.

-

Optimize entry size and stop loss placement.

-

Add volume filter to ensure liquidity.

-

Test parameters across different products.

-

Employ machine learning to auto-optimize parameters based on backtests.

Conclusion

The Ichimoku Kinko Hyo Cross strategy combines various technical analysis tools like moving average crossovers, delayed lines, and Cloud bands to identify high-probability entries in trending or reversal scenarios. Proper optimization and risk management can further improve its stability and profitability. The strategy is easy to understand and implement, making it worth live testing and application.

- 1