Super Momentum Strategy

Overview

The Super Momentum strategy combines multiple momentum indicators. It buys when multiple momentum indicators are bullish concurrently, and sells when they are bearish concurrently. By integrating multiple momentum indicators, it aims to capture price trends more accurately and avoid false signals from individual indicators.

Strategy Logic

The strategy uses 4 RMI indicators by Everget and 1 Chande Momentum Oscillator. RMI measures price momentum to gauge bullish and bearish strength. Chande MO calculates price change to identify overbought and oversold conditions.

It goes long when RMI5 crosses above its buy line, RMI4 crosses below its buy line, RMI3 crosses below its buy line, RMI2 crosses below its buy line, RMI1 crosses below its buy line, and Chande MO crosses above its buy line.

It goes short when RMI5 crosses below its sell line, RMI4 crosses above its sell line, RMI3 crosses above its sell line, RMI2 crosses above its sell line, RMI1 crosses above its sell line, and Chande MO crosses below its sell line.

RMI5 is set opposite to other RMI to better identify trends for pyramid trading.

Advantage Analysis

-

Combining multiple indicators improves trend accuracy and avoids false signals

-

Indicators across timeframes catch larger trends

-

Reverse RMI aids in trend identification and pyramiding

-

Chande MO prevents bad trades in overbought/oversold conditions

Risk Analysis

-

Complex parameters with multiple indicators need thorough optimization

-

Concurrent indicator moves may generate false signals

-

Lower trade frequency with multiple filters

-

Parameters may not suit different products and market regimes

Optimization Directions

-

Test and optimize parameters for strategy robustness

-

Add/remove indicators to evaluate signal quality impact

-

Introduce filters to avoid false signals in certain markets

-

Adjust indicator buy/sell lines to find optimal combinations

-

Consider adding stop loss for risk control

Conclusion

This strategy improves trend judgment by integrating momentum indicators. But parameter optimization is crucial due to complexity. If well-tuned, it can generate quality signals and has an edge in trend following. But traders should watch for risks, find optimal parameters, and incorporate risk controls for steady trading.

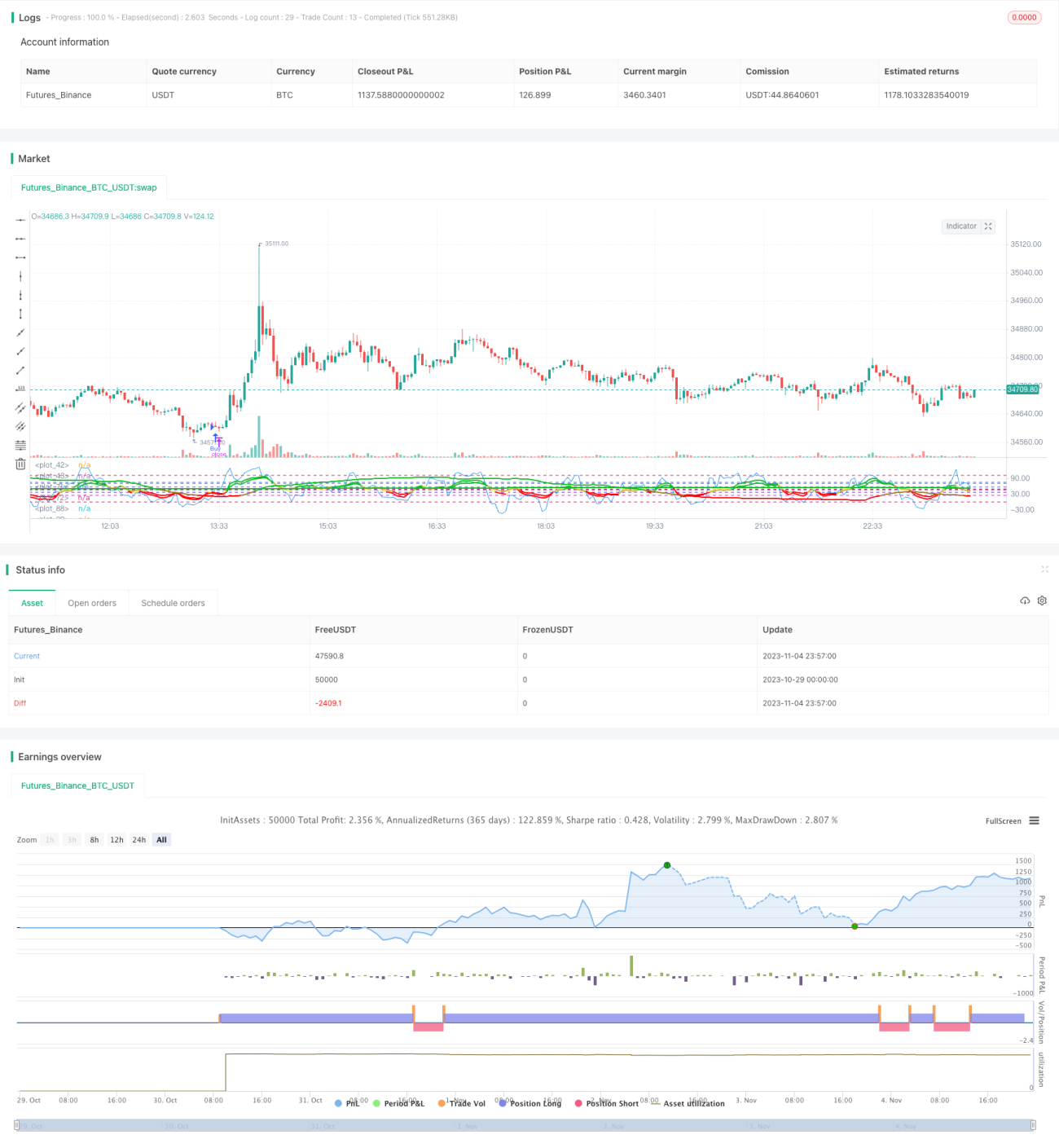

/*backtest

start: 2023-10-29 00:00:00

end: 2023-11-05 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Super Momentum Strat", shorttitle="SMS", format=format.price, precision=2)

//* Backtesting Period Selector | Component *//- 1