Gaussian Detrended Reversion Trading Strategy

Overview

This is a strategy that identifies potential price reversals using a customized Gaussian Detrended Price Oscillator (GDPO) combined with smoothed price cycles. It uses the detrended oscillator with Gaussian smoothing and sets specific entry and exit rules to capture reversal opportunities.

Strategy Logic

The strategy first calculates the Detrended Price Oscillator (DPO) by comparing the close price to an Exponential Moving Average (EMA) over a specified period to identify short-term price cycles. The DPO values are then smoothed using the Arnaud Legoux Moving Average (ALMA) with Gaussian smoothing technique to filter out noise.

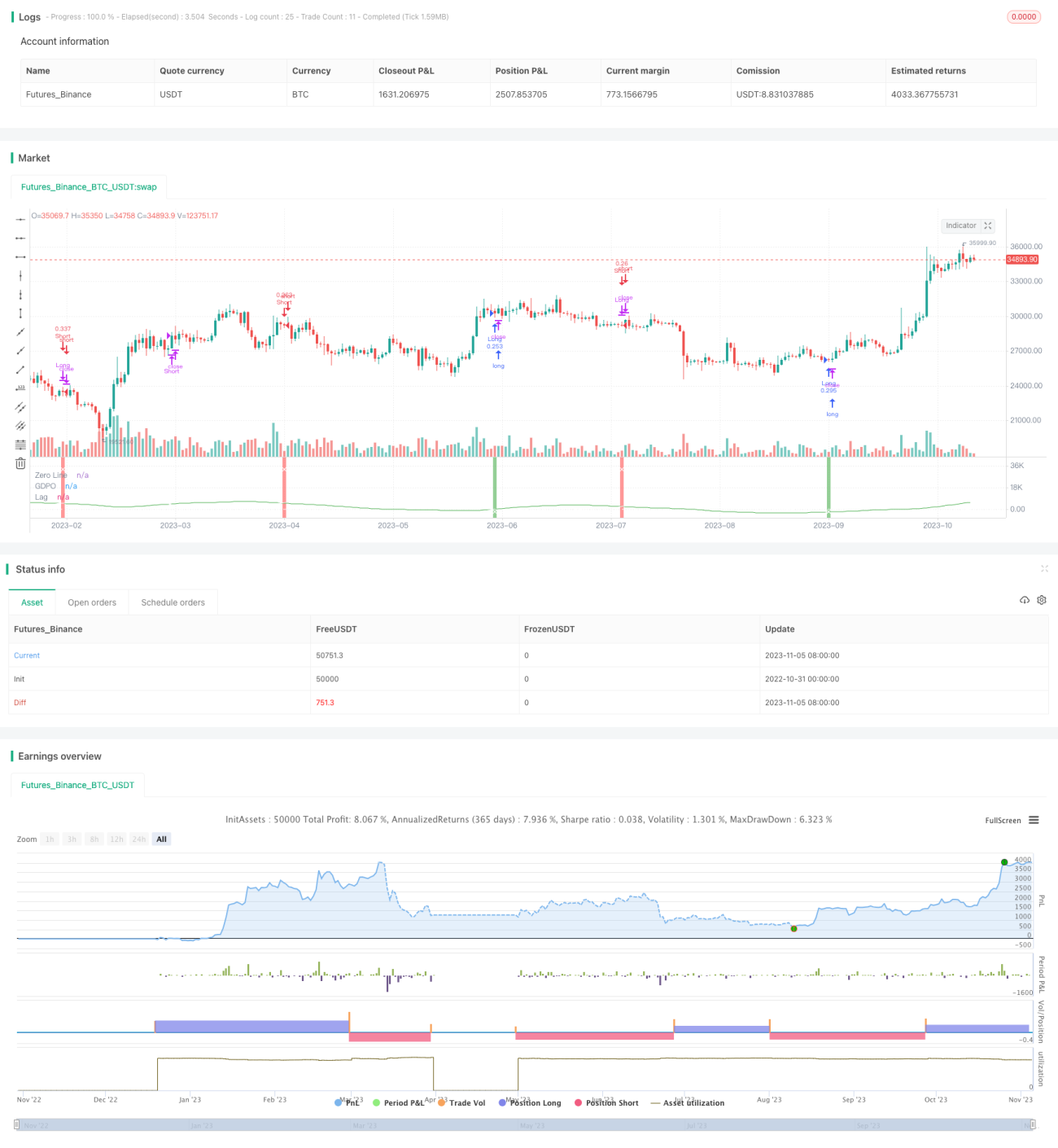

The entry and exit rules are defined based on crossover events between the smoothed GDPO and its lagged version. A long position is entered when the smoothed GDPO crosses above the lag and is negative. The long position is exited when the smoothed GDPO crosses below the lag or the zero line. A short position is entered when the smoothed GDPO crosses below the lag and is positive. The short position is exited when the smoothed GDPO crosses above the lag or the zero line.

The smoothed GDPO and its lag are plotted in distinct colors. The zero line is also displayed as a reference. The chart background color changes when the strategy enters a position. Cross markers are plotted at the crossover points as exit signals.

Advantage Analysis

The strategy combines detrending techniques and Gaussian smoothing to more clearly identify reversal opportunities compared to other oscillators. The GDPO improves accuracy by incorporating cycle analysis with detrending. Gaussian smoothing eliminates noise for clearer signals. The specific entry and exit rules effectively control losses.

Risk Analysis

The strategy is sensitive to parameter tuning like the period lengths and smoothing parameters. Extensive backtesting is required to determine optimal parameters, otherwise excessive false signals may occur. The strategy may produce consecutive losses in trending markets. Stop loss should be used to control single trade loss. Failed reversals are also a major risk. Reversal probability should be confirmed using chart patterns and trend strength.

Optimization can be done by dynamically adjusting parameters and incorporating trend indicators to improve robustness. Dynamic stops can also control risks.

Optimization Directions

The strategy can be optimized in several aspects:

-

Dynamically adjust smoothing parameters to increase smoothing in trends and reduce false signals.

-

Incorporate trend indicators like ADX to avoid losses in trending markets.

-

Add stop loss mechanisms like dynamic or trailing stops.

-

Optimize entry conditions using additional indicators or patterns for higher entry accuracy.

-

Optimize capital management by adjusting position sizing and stops based on market conditions.

-

Test the strategy across different timeframes like daily or weekly data.

Summary

The Gaussian Detrended Reversion strategy identifies short-term cycles using the GDPO and extracts signals with Gaussian filtering to capture reversals under defined entry and exit rules. It effectively controls the risks of reversal trading but requires parameter optimization and trend validation. Further improvements in robustness can be made through dynamic adjustments, confirming indicators and stop loss strategies.

- 1