Dual Timeframe DI Trend Following Strategy

Overview

This strategy uses Average Directional Index (DI+) and Negative Directional Index (DI-) on two timeframes to determine the trend direction for long and short trades. When DI+ is higher than DI- on both larger and smaller timeframes, it indicates an upward trend and a long signal is triggered. When DI- is higher than DI+ on both frames, it indicates a downward trend and a short signal is triggered.

How it Works

The strategy is based on several principles:

-

Calculate DI+ and DI-. Get DI+ and DI- by using high, close and low prices.

-

Compare DI+ and DI- on two timeframes. Calculate DI+ and DI- respectively on the main chart timeframe (e.g. 1 hour) and a larger timeframe (e.g. daily). Compare the values between the two timeframes.

-

Determine trend direction. When DI+ is greater than DI- on both larger and smaller timeframes, it indicates an upward trend. When DI- is greater than DI+ on both frames, it indicates a downward trend.

-

Trigger trading signals. DI+>DI- on both frames gives long signal. DI->DI+ on both frames gives short signal.

-

Set stop loss. Use ATR to calculate dynamic stop loss for trend following.

-

Exit conditions. Exit when stop loss is hit or price reverses.

Advantages

The strategy has the following advantages:

-

Using dual timeframe DI filters out some false breakouts.

-

ATR trailing stop maximizes profit protection and avoids stops being too tight.

-

Timely stop loss controls loss on single trades.

-

Trading with the trend allows continuously catching trends.

-

Simple and clear rules, easy to implement for live trading.

Risks and Solutions

There are also several risks:

-

DI has lagging effect, may miss entry timing. Can optimize parameters or add other indicators.

-

Dual timeframe may have divergence between larger and smaller TF. Add more timeframe validation.

-

Stop loss too aggressive may cause over-trading. Loosen ATR multiplier.

-

Whipsaw in sideways market can cause frequent trades. Add filters to reduce trading frequency.

-

Parameter optimization relies on historical data and may be overfitted. Evaluate parameter robustness prudently.

Optimization Directions

The strategy can be improved in the following aspects:

-

Optimize DI calculation parameters for best parameter set.

-

Add other indicator filters to improve signal accuracy, e.g. MACD, KDJ etc.

-

Enhance stop loss strategy to adapt more market conditions, such as trailing stop or pending orders.

-

Add trading session filters to avoid significant news events.

-

Test parameter robustness on different products to improve adaptiveness.

-

Introduce machine learning to train model on historical data.

Conclusion

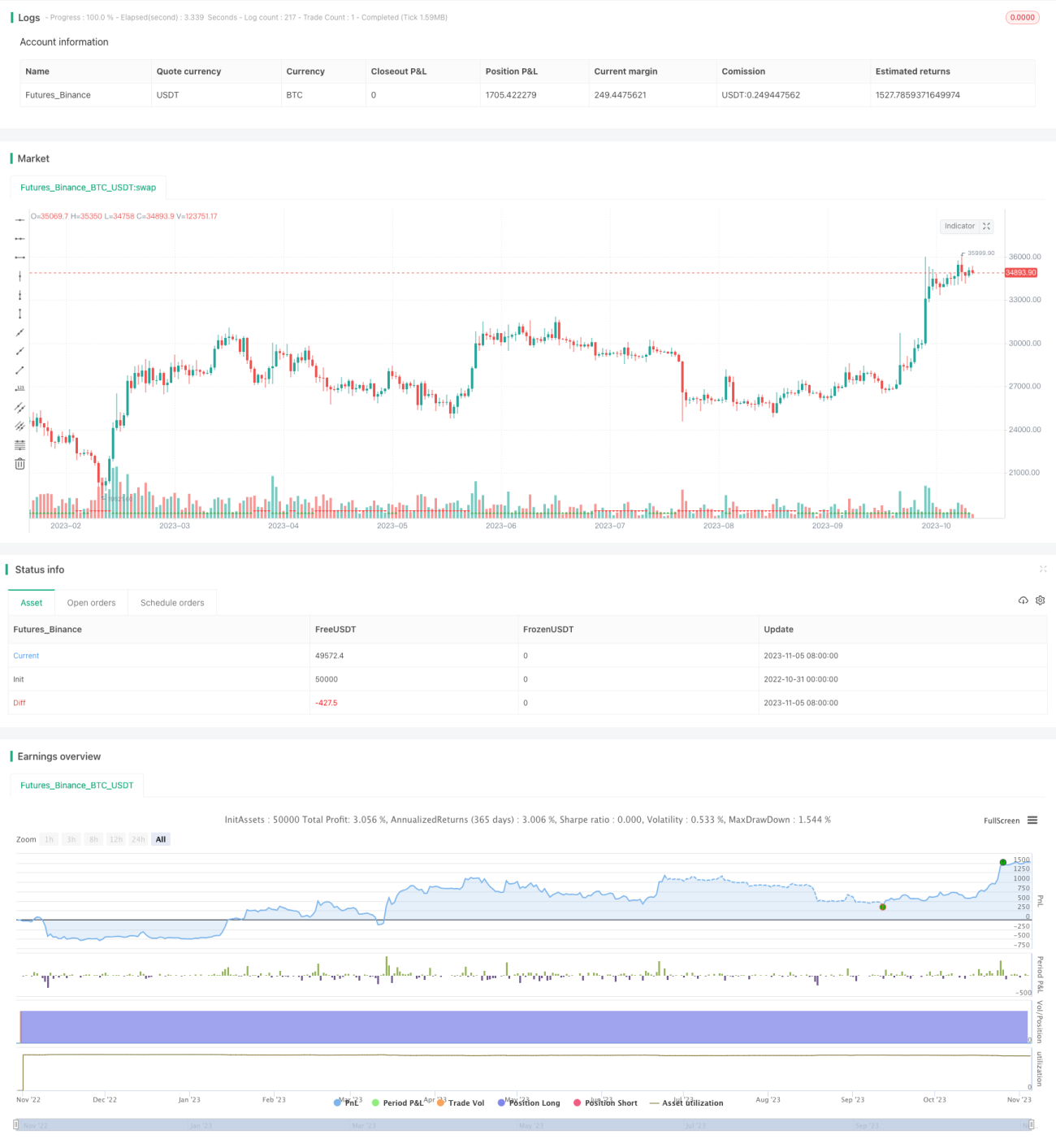

In summary, this is a typical trend following strategy that uses DI to determine trend direction and set stop loss to lock in profits along the trend. The advantage lies in its clear logic and ease of implementation for live trading. There are also rooms for improvement via parameter optimization, adding filters etc. With further optimization and robustness test, it can become a very practical trend following strategy.

- 1