概述

本策略基于Relative Strength Index(RSI)指标设计,通过RSI指标判断超买超卖情况,实现趋势追踪。当RSI低于超卖线时做多,当RSI高于超买线时做空,通过追踪行情的主要趋势来获利。

策略原理

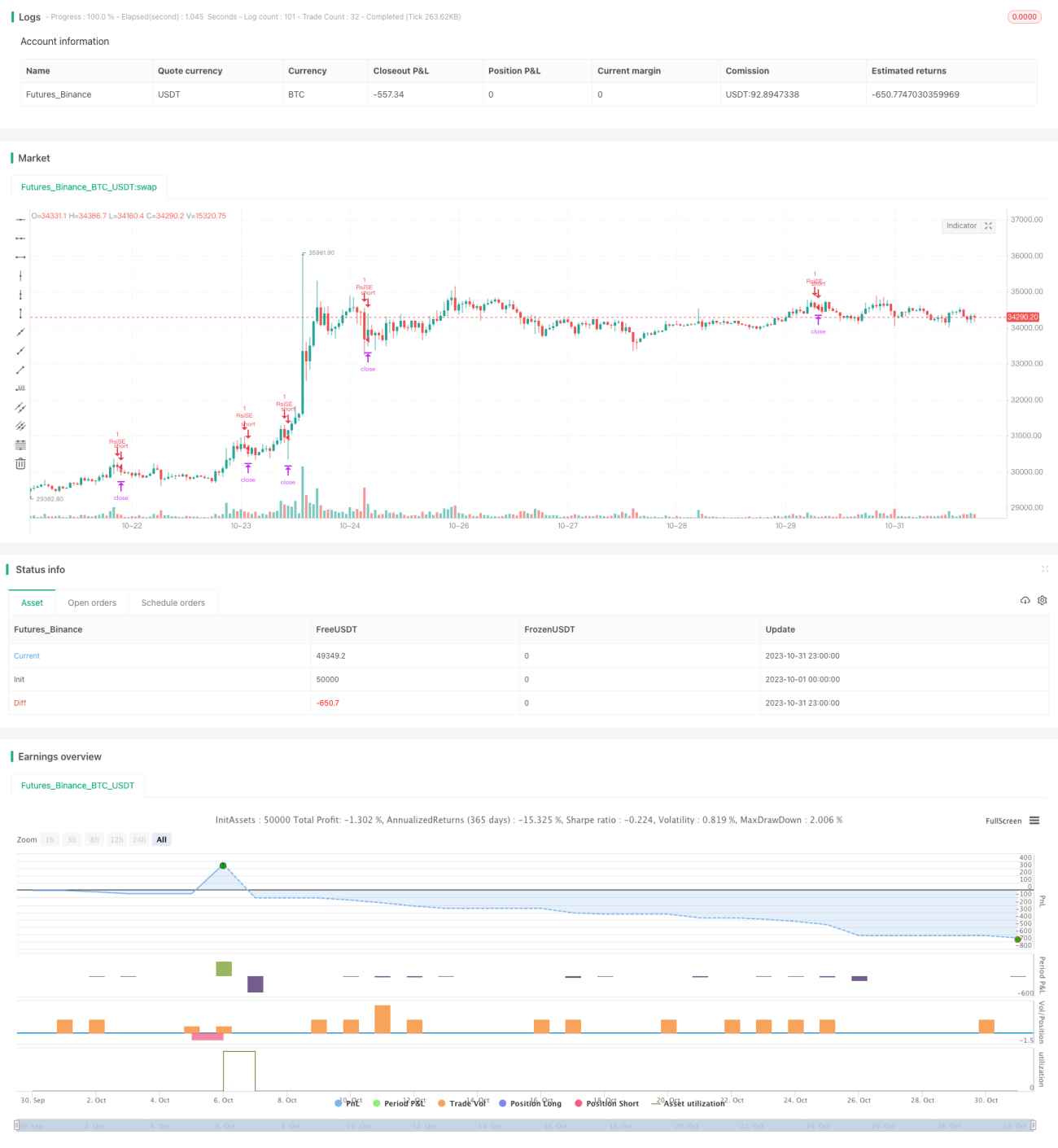

本策略使用RSI指标判断市场的超买超卖情况。RSI指标基于一定时间周期内的涨跌幅进行计算,当RSI低于30时被视为超卖,当RSI高于70时被视为超买。

具体来说,本策略首先定义RSI计算参数length=14,超买线overBought=70,超卖线overSold=30。然后根据close价格计算出RSI值vrsi。判断vrsi是否高于超买线或低于超卖线,如果发生黄金交叉做多,如果发生死亡交叉做空。做多做空后设置止损点为etoroStopTicks ticks,在窗口期内触发止损后平仓。

通过这种方式,本策略能够捕捉市场的主要趋势,在超卖点买入,在超买点卖出,实现趋势追踪。

策略优势

- 利用RSI指标判断超买超卖情况,有利于捕捉市场趋势

- 回测窗口设定灵活,可以选择不同的时间范围进行测试

- 止损点设置合理,可以控制单笔损失

策略风险

- RSI存在拉胯现象,可能产生错误信号

- 止损点 static,无法动态跟踪市场波动

- 无法判断趋势反转点,可能反向开仓

风险解决方法:

- 结合其他指标过滤 RSI 信号,避免错误开仓

- 动态调整止损点,实时跟踪市场波动

- 增加趋势判断指标,避免反向开仓

策略优化方向

本策略可以从以下几个方面进行优化:

- 优化RSI参数,寻找最优参数组合

可以测试不同的RSI计算周期length,不同的超买超卖阈值,找到最优参数以减少错误信号。

- 增加趋势判断指标,避免逆势交易

可以加入均线、MACD等指标判断趋势方向,避免在趋势反转点产生错误信号。

- 动态止损

可以根据ATR等指标设定动态止损点,让止损更加贴近市场波动。

- 优化入场规则

可以在RSI信号基础上增加其它条件,如突破某一价格位、交易量放大等作为入场信号,提高入场精确度。

总结

本策略通过RSI指标判断超买超卖情况,实现了对趋势的捕捉。相比传统的跟踪止损策略,具有利用指标判断市场Timing的优势。但RSI指标存在拉胯现象,无法判断趋势反转点,这是本策略需要优化的方向。通过参数优化、增加趋势判断、动态止损等手段,可以进一步提升策略的稳定性和盈利能力。

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1