Volatility Adjusted Moving Average Trading Strategy

Overview

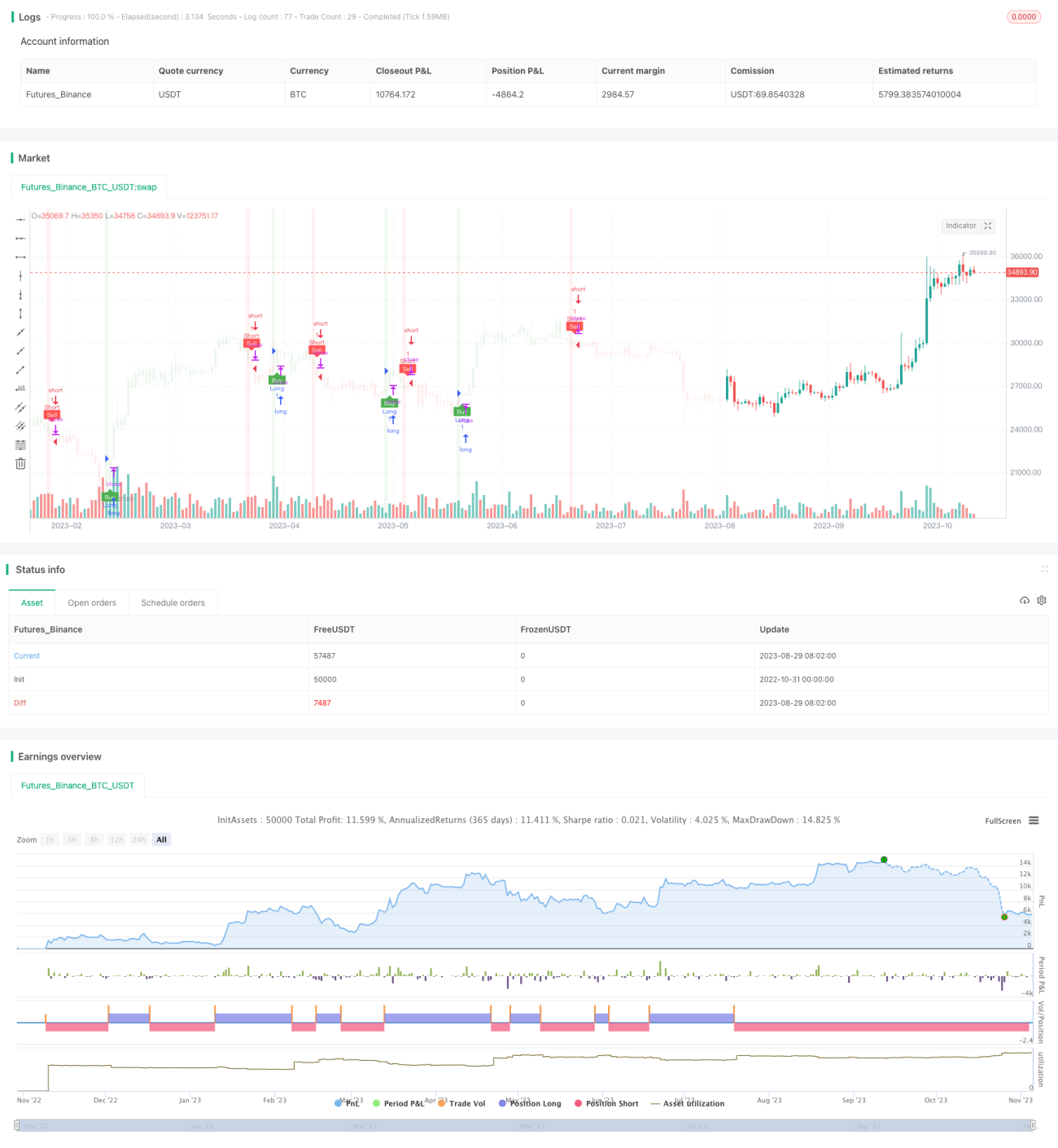

This strategy utilizes a combination of the T3 moving average, ATR indicator and Heikin Ashi to identify buy and sell signals, and uses the ATR to calculate stop loss and take profit levels for trend following trading. The advantage of this strategy is the quick response while controlling trading risk.

Principle Analysis

Indicator Calculations

-

T3 Moving Average: Calculates a smoothed T3 moving average (default period 100) to determine trend direction

-

ATR: Calculates the Average True Range, used to determine stop loss/take profit size

-

ATR Trailing Stop: Calculates a stop loss based on ATR that adjusts based on price movement and volatility

Trade Logic

-

Buy Signal: Triggered when close crosses above ATR trailing stop and is below T3 moving average

-

Sell Signal: Triggered when close crosses below ATR trailing stop and is above T3 moving average

-

Stop Loss/Take Profit: After entry, stop loss and take profit prices calculated based on ATR and user defined risk/reward ratio

Entry and Exit

-

Long Entry: Stop loss is entry price minus ATR, take profit is entry price plus ATR * risk/reward ratio

-

Short Entry: Stop loss is entry price plus ATR, take profit is entry price minus ATR * risk/reward ratio

-

Exit when price hits stop loss or take profit levels

Advantage Analysis

Quick Response

T3 moving average default period is 100, more sensitive than typical moving averages for faster reaction to price changes

Risk Control

ATR trailing stop moves with market volatility to avoid being stopped out. Stop loss/take profit based on ATR controls risk/reward per trade

Trend Following

ATR trailing stop follows the trend, avoids premature exit even during short term pullbacks

Parameter Optimization

Periods for both T3 and ATR can be optimized for different markets to improve robustness

Risk Analysis

Stop Loss Breakeven

Severe price moves could penetrate stop loss causing loss. Can widen ATR period and stop distance.

Trend Reversal

Losses possible if trend reverses and price crosses trailing stop. Can incorporate other indicators to identify reversals.

Optimization Overfitting

Parameter optimization risks overfitting limited historical data. Need robust optimization across markets/timeframes.

Improvement Opportunities

-

Test different T3 moving average periods to find optimal balance of sensitivity and stability

-

Optimize ATR period to find best risk control and trend following balance

-

Incorporate RSI, MACD to avoid wrong trades at turning points

-

Machine learning for optimal automated parameters, reducing manual bias

-

Add position sizing rules to better control risk

Summary

This strategy combines the advantages of the T3 and ATR to enable fast response with risk control. Further enhancements in stability and efficiency possible through parameter optimization and additional filters. But traders should still watch for reversal and breakeven risks, and avoid over-reliance on backtest results.

- 1