SMA Crossover Strategy

Overview

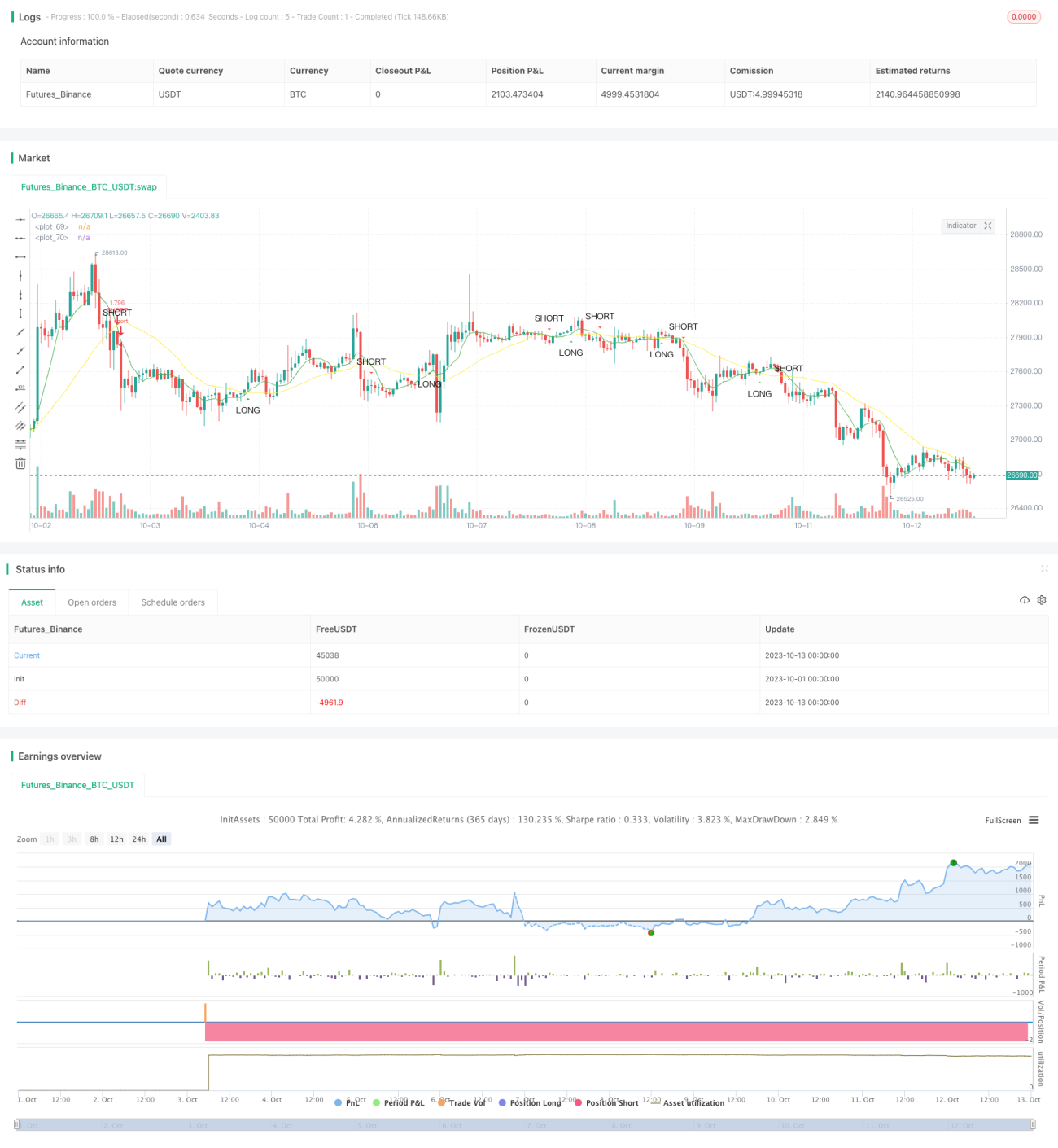

This strategy generates trading signals based on the crossover between fast and slow moving averages. It produces buy signals when the fast moving average crosses above the slow moving average from below. It produces sell signals when the fast moving average crosses below the slow moving average from above.

Principles

This strategy uses the sma function to calculate the fast and slow moving averages. The fast_SMA is the fast moving average with period length fast_SMA_input. The slow_SMA is the slow moving average with period length slow_SMA_input.

The strategy uses the cross and crossunder functions to determine the crossover between the fast and slow moving averages. When the fast moving average crosses above the slow moving average, the LONG variable is true and a buy signal is generated. When the fast moving average crosses below the slow moving average, the SHORT variable is true and a sell signal is generated.

Advantages

This strategy has the following advantages:

- Simple principle, easy to understand and implement.

- Customizable moving average periods, adaptable to different market environments.

- Filters out some market noise and generates relatively reliable trading signals.

- Captures both the start and turning points of trends.

Risks

This strategy also has the following risks:

- Can generate excessive trading signals if the settings are improper, leading to overtrading.

- May produce many false signals in sideways markets.

- Cannot determine the duration of a trend, may reverse prematurely.

Risk management:

- Set appropriate moving average parameters to balance filtering effect and sensitivity.

- Add trend indicator filters to avoid false signals.

- Set stop loss points to control loss per trade.

Optimization

This strategy can be optimized from the following aspects:

- Add filtering conditions on volume or volatility when the breakout happens to avoid false breakouts.

- Incorporate trend indicators to identify trend direction and strength.

- Add machine learning models to auto-optimize the moving average parameters.

- Combine with support/resistance and Bollinger Bands to define trading ranges and improve entry accuracy.

Summary

This strategy effectively generates trading signals by leveraging the advantages of moving averages. Although there are some risks, they can be improved by parameter optimization, adding filters etc. The moving average crossover strategy is worth further research and application.

- 1