ZVWAP Strategy Based on Z-Distance from VWAP

Overview

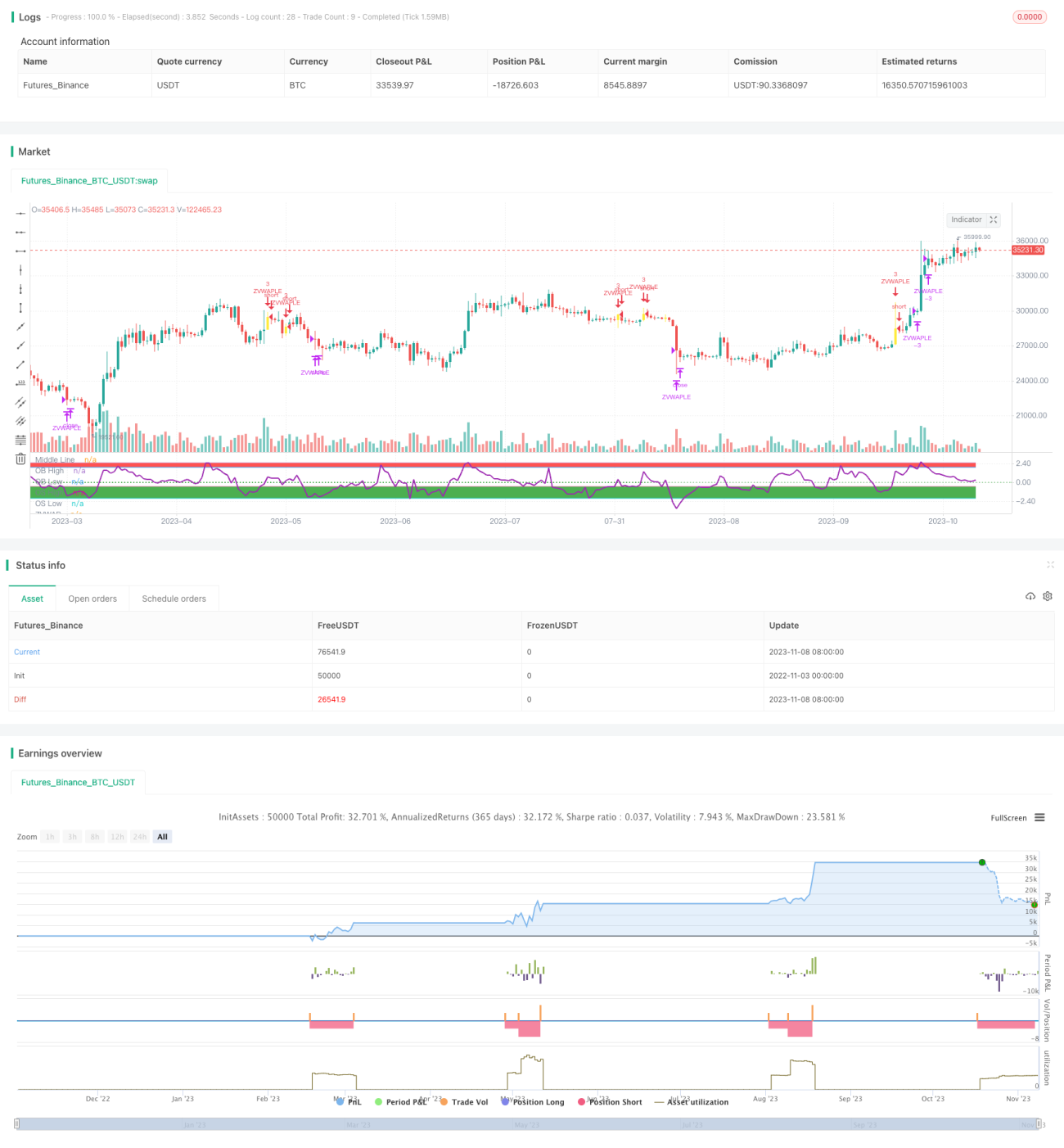

This strategy is based on the Z-distance from VWAP indicator by LazyBear. It uses the Z-distance between price and VWAP to determine overbought and oversold conditions, as well as entries and exits. The strategy incorporates EMA lines and Z-distance crossing 0 level to filter out some noise.

Strategy Logic

- Calculate VWAP value

- Calculate Z-distance between price and VWAP

- Set overbought line (2.5) and oversold line (-0.5)

- Go long when fast EMA > slow EMA, Z-distance < oversold line and Z-distance crosses above 0

- Close position when Z-distance > overbought line

- Incorporate stop loss logic

Key Functions:

- calc_zvwap: Calculate Z-distance between price and VWAP

- VWAP value: vwap(hlc3)

- Fast EMA: ema(close,fastEma)

- Slow EMA: ema(close,slowEma)

Advantage Analysis

- Z-distance intuitively shows overbought/oversold levels

- EMA filters out false breakouts

- Allows pyramiding to capitalize on trends

- Has stop loss logic to control risk

Risk Analysis

- Need to ensure parameters like lines, EMA periods are set properly

- Z-distance indicator lags, may miss key turning points

- Pyramiding can increase loss if trend reverses

- Stop loss needs to be set reasonably

Solutions:

- Optimize parameters via backtesting

- Add other indicators to filter signals

- Set proper conditions for pyramiding

- Use dynamic stop loss

Optimization Directions

- Optimize EMA periods

- Test different overbought/oversold criteria

- Add other indicators to filter noise

- Test different stop loss techniques

- Optimize entry, pyramiding and stop loss logic

Summary

The strategy uses Z-distance to determine price-VWAP relationship and adds EMA to filter signals, aiming to capture trend opportunities. It allows pyramiding to follow trends and has a stop loss to control risk. Optimization and adding other indicators can improve robustness. However, lagging issue of Z-distance should be considered during optimization. Overall, this is a trend-following strategy with simple, clear logic. When fully optimized, it can be an efficient tool to trade trends.

- 1