Bollinger Band Breakout Strategy

Overview

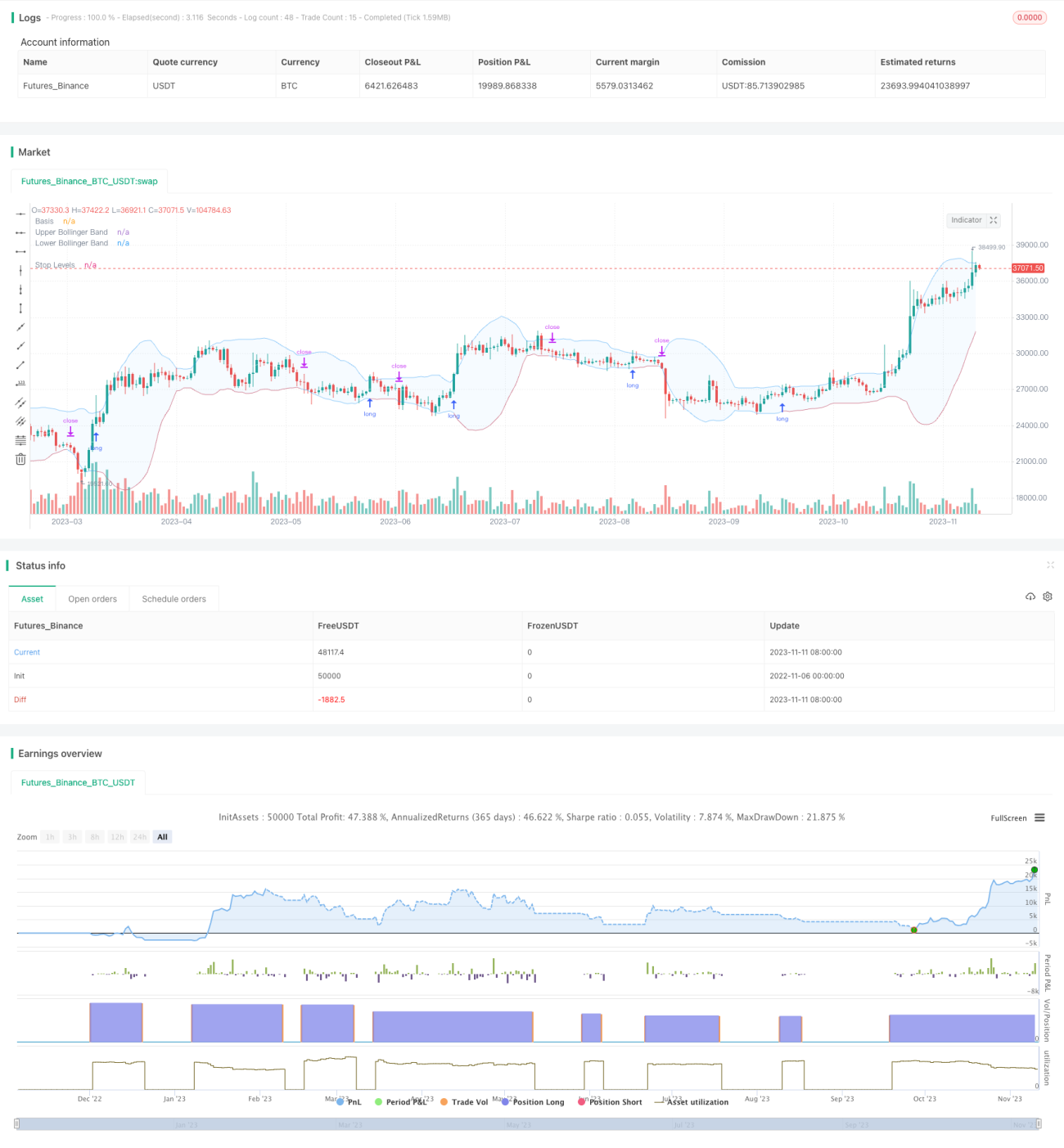

This strategy utilizes the dynamic upper and lower bands of Bollinger Bands to go long when the price breaks above the upper band and close position when the price falls below the lower band. Unlike traditional breakout strategies with fixed levels, the bands of Bollinger Bands change dynamically based on historical volatility, making it better at identifying overbought and oversold conditions.

Strategy Logic

The strategy relies primarily on the Bollinger Bands indicator to identify breakouts. The Bollinger Bands consist of three lines:

- Middle Line: n-period moving average

- Upper Band: Middle Line + k * n-period standard deviation

- Lower Band: Middle Line - k * n-period standard deviation

When the price rises above the upper band, the market is considered overbought, and a long position can be initiated. When the price falls below the lower band, the market is oversold, and the position should be closed.

The strategy allows customization of the Bollinger Bands parameters: the moving average period n and the standard deviation multiplier k. The default values are 20 periods for the moving average and 2 for the standard deviation multiplier.

The strategy checks if the closing price breaks above the upper band after each trading day. If it does, a long signal is triggered on the next day's opening. Once long, the strategy monitors if the price breaks below the lower band in real-time and closes the position if it does.

The strategy also incorporates a moving average filter that only generates buy signals when the price is above the moving average line. The moving average can be set on the current or higher timeframe to better control entry timing.

Two stop loss choices are provided: fixed percentage stop loss or trailing the lower band. The latter gives more room for profits to run.

Advantages of the Strategy

- Utilize Bollinger Bands to judge overbought/oversold levels

- Moving average filter avoids trading against the trend

- Customizable Bollinger Bands parameters suit different periods

- Choice between two stop loss methods

- Backtesting allows parameter optimization and out-of-sample verification

Risks of the Strategy

- Bollinger Bands cannot fully determine overbought/oversold

- Moving average filter may miss faster breakouts

- Fixed stop loss can be too conservative, trailing stop may be too aggressive

- Parameters need optimization for different products and timeframes

- Unable to limit loss size, need to consider money management

Optimization Directions

- Test different moving average parameter combinations

- Try different Bollinger Bands parameters

- Compare fixed percentage stop loss vs trailing lower band in terms of return

- Add money management module to limit per trade loss

- Incorporate other indicators to confirm Bollinger Bands signal

Conclusion

The strategy identifies overbought/oversold conditions using Bollinger Bands' dynamic bands, refers to moving average filters, and uses stops to protect capital. Compared to traditional fixed-level breakouts, it adapts better to market fluctuations. With further parameter optimization and risk controls, the strategy can achieve higher stability and returns. Overall, by utilizing the dynamic nature of Bollinger Bands, the strategy captures the strengths of breakout strategies and is worth live trading and long-term optimization.

- 1