概述

该策略利用指标MACD的快线和慢线的交叉信号,结合其他多个指标进行综合判断,在瞬时时机捕捉到指数移动平均线的突破信号,做出买入或卖出决策,属于短线交易策略。

策略原理

-

使用MACD的快线和慢线交叉作为主要交易信号。当快线上穿慢线时看涨入场,当快线下穿慢线时看跌入场。

-

结合RSI指标判断是否过买过卖。RSI低于中线时看涨,RSI高于中线时看跌。

-

计算当前收盘价与一定周期内的SMA均线作比较,收盘价低于SMA时看涨,收盘价高于SMA时看跌。

-

计算一定周期内的Highest值的0.5 Fibonacci位,作为看涨的阻力位。计算一定周期内的Lowest值的0.5 Fibonacci位,作为看跌的支撑位。

-

当满足快线上穿和价格低于支撑位时看涨入场,当满足快线下穿和价格高于阻力位时看跌入场。

-

采用逐步移动止损方式。入场后开始时止损位固定为开仓价格的一定百分比,当亏损达到一定比例后改为小幅逐步追踪止损。

策略优势

-

策略充分利用MACD的交叉信号,这是一种经典且有效的技术指标交易信号。

-

结合RSI、SMA等多个指标进行确认,可以过滤假信号,提高信号的可靠性。

-

计算动态支持阻力位,进行突破交易,可以捕捉较大行情。

-

采用逐步移动止损方式,既可锁住大部分利润,也可控制风险。

-

策略交易逻辑清晰简单,容易理解掌握,适合新手学习。

策略风险

-

MACD指标存在滞后问题,可能会错过行情最佳买点卖点。

-

多指标组合判断增加了策略复杂度,容易出现指标冲突的情况。

-

动态计算支持阻力位存在错误突破的风险。

-

移动止损在大行情中可能过早止损,无法持续获利。

-

策略参数需要反复测试优化,不合适的参数会影响策略效果。

策略优化方向

-

可以测试不同参数组合,优化MACD周期参数。

-

可以引入更多指标,如布林线、KDJ等进行多维度分析。

-

可以结合更多因素判断支持阻力位的合理性。

-

可以研究更先进的移动止损机制,如时间止损、振荡止损等。

-

可以加入自动参数优化模块,实现参数的自动寻优。

总结

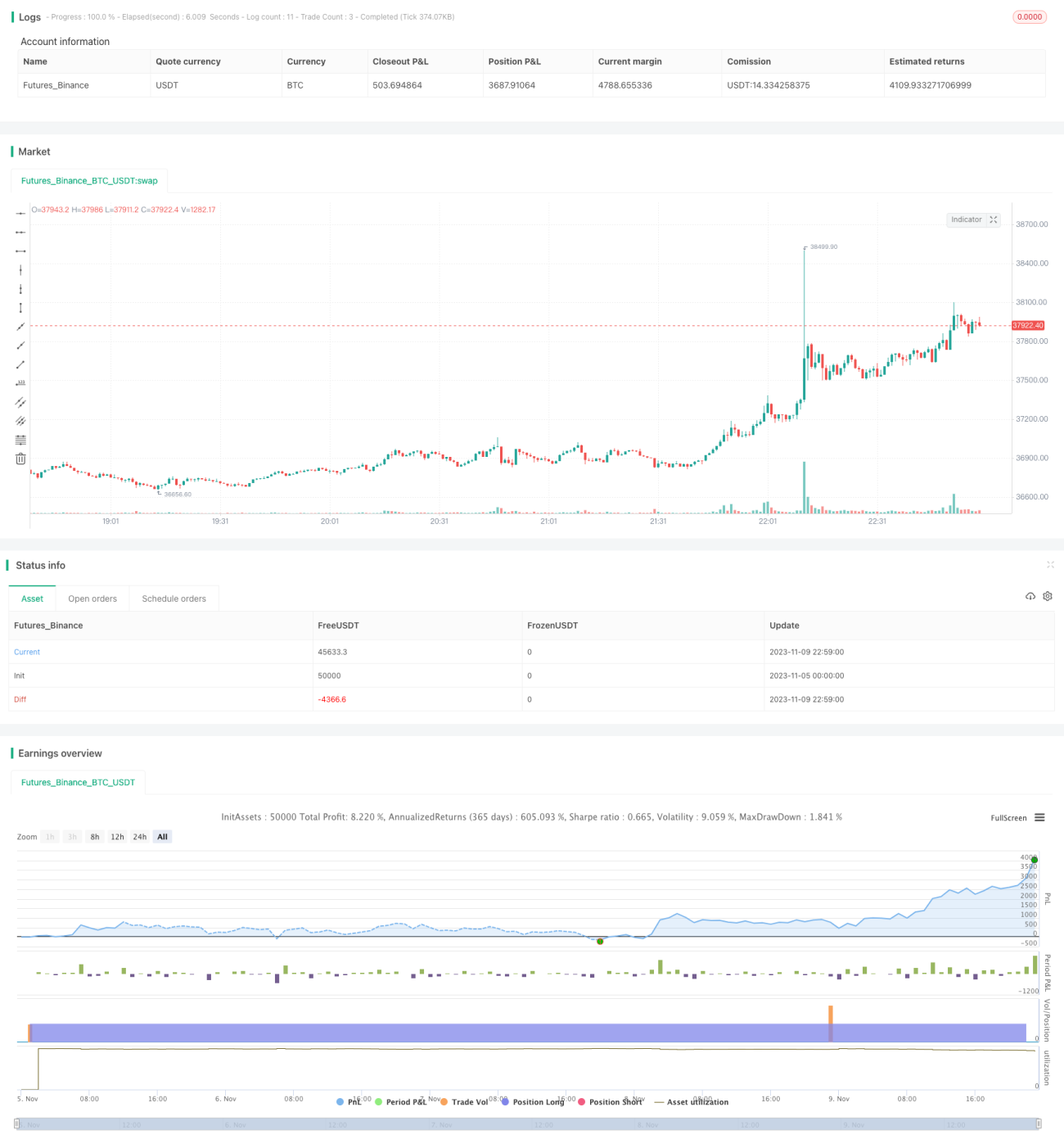

该策略综合运用MACD、RSI、SMA等多个指标,在瞬时时机捕捉到指数移动平均线的突破信号,属于典型的短线突破交易策略。策略信号生成有一定的滞后性,但可以通过参数优化提高准确率。总体来说,该策略交易逻辑简单清晰,容易掌握,表现稳健,适合大多数人学习使用,值得进一步的测试和优化。

- 1