ICHIMOKU Cloud and STOCH Indicator Based Trend Tracking Strategy

Overview

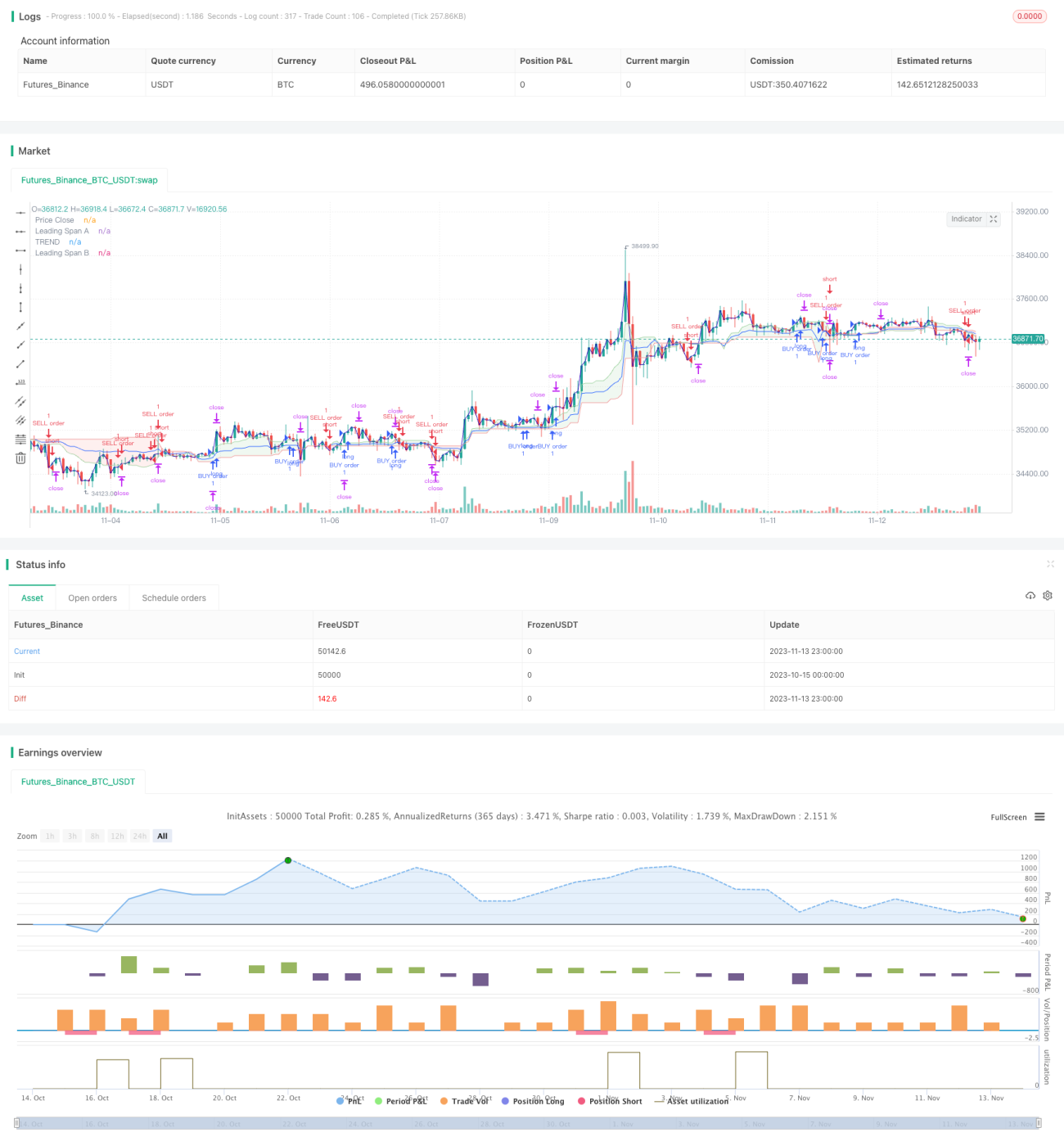

This strategy is based on the ICHIMOKU cloud chart pattern indicator and the STOCH random indicator to determine and track trends. The strategy name is "ICHIMOKU Cloud Stoch Trend Tracking Strategy".

Strategy Principle

The strategy mainly judges the current trend direction and overbought/oversold situations through the ICHIMOKU cloud chart and the STOCH indicator.

When the Conversion Line crosses above the Base Line and the Stoch indicator bounces back from the oversold area, it is considered a bullish trend and the strategy takes a bullish direction. When the Conversion Line crosses below the Base Line and the Stoch indicator falls back from the overbought area, it is considered a bearish trend and the strategy takes a bearish direction.

In the code, the Conversion Line is defined as the average of the highest and lowest prices of the last N1 bars; The Base Line is defined as the average of the highest and lowest prices of the last N2 bars. A bullish signal is generated when the conversion line crosses above the base line.

The Stoch indicator defines overbought and oversold threshold lines, as well as smoothing parameters K and D. A bullish signal is generated when the Stoch bounces back from the oversold area, and a bearish signal is generated when it falls back from the overbought area.

By combining the two indicators, the strategy determines the trend direction.

Advantage Analysis

The strategy combines chart pattern indicators and overbought/oversold indicators to effectively determine the trend direction.

Compared to using a single trend judgment indicator, this strategy comprehensively considers both trend and overrun situations, and can more accurately determine entry timing.

The ICHIMOKU cloud chart can identify medium and long term trends, while the Stoch indicator can discover short-term overbought/oversold situations. The two complement each other to form systematic judgments.

Risk Analysis

The main risks of this strategy are:

-

The risk of indicator failure in case of black swan events.

-

There is some lag, which may miss part of the trend or reverse opening positions.

-

The combined multiple factors judgment has some subjectivity, and improper parameter settings may cause mistakes.

-

High trading frequency may impact profits due to transaction costs.

Corresponding optimization measures:

-

Combine news events to avoid blind trading during major policy events.

-

Appropriately shorten cycle parameters to reduce lag probability.

-

Optimize parameters through backtesting to improve scientific settings.

-

Appropriately increase take profit and stop loss ranges to reduce trading frequency.

Optimization Directions

The main optimization directions for this strategy are:

-

Optimize the cycle parameters of the ICHIMOKU conversion line and base line to better fit different market characteristics.

-

Optimize the K, D smoothing parameters and overbought/oversold threshold values of the Stoch indicator.

-

Increase other indicators to form a multifactor model and improve system reliability.

-

Optimize take profit and stop loss points to reduce trading frequency while ensuring profitability.

-

Add a module to judge emergencies and avoid failure during major events.

Summary

This strategy combines ICHIMOKU cloud charts and Stoch indicators to make comprehensive judgments on trend direction and overbought/oversold situations, which can effectively track trending markets. By considering chart patterns and quantitative indicators, the strategy is more systematic. Future optimizations may include adjusting parameters, adding other indicators, adding emergency judgment modules, etc.

- 1