Momentum Trend Following Oscillation Strategy

Overview

This strategy combines moving average, volume-price and oscillation indicators to form triple filters, aiming to capture medium-term trends and achieve good returns during trending markets.

Principles

The strategy consists of three main components:

- Moving Average Indicators

Use 20-day EMA and 60-day EMA to construct a trend filter. A buying signal is generated when the short term MA crosses above the long term MA. A selling signal is generated when the short term MA crosses below the long term MA.

- Volume-Price Indicator

Use volume over turnover to calculate VP indicator, judging capital flow directions. Rising VP suggests net inflow while declining VP suggests net outflow. VP reversals can signal trend shifts.

- Bollinger Bands

Use 20-day Donchian Channel Width to calculate Bollinger Bands Parameter, forming upper and lower bands. Prices approaching the upper band may face pullback pressure, while prices approaching the lower band may bounce back up.

Combining the three components constructs a trend-following strategy. It generates buy signals when short MA crosses above long MA, VP is in uptrend and price just left the upper band. Sell signals are generated when short MA crosses below long MA, VP is in downtrend and price just left the lower band.

Advantages

The strategy has the following advantages:

-

Triple indicator filters help avoid false breaks.

-

Considering trend, capital flow and overbought/oversold improves signal reliability.

-

Optimized parameters suitable for different periods and products.

-

Controllable drawdowns and steady returns.

-

Clear logic and flexible parameter tuning.

Risks

There are also some risks:

-

Trend reversal risks. Trend changes may cause stop loss.

-

VP lagging issue. VP lags price changes and may miss entry or exit points.

-

Difficult parameter tuning. Parameters need adjustments for different products and timeframes.

-

Drawdown control needs improvement. Further optimize with dynamic stops or position sizing.

Enhancement Directions

The strategy can be improved in the following aspects:

-

Add stop loss methods like trailing stop to further control drawdowns.

-

Add position sizing module to dynamically adjust sizes based on volatility.

-

Optimize parameters to find best sets for different products and periods.

-

Increase machine learning models to improve signal accuracy.

-

Incorporate sentiment and news analytics to judge sudden events.

Conclusion

The strategy combines MA, VP and Bollinger Band indicators to perform well in catching medium-term trends. Further improvements in stop loss, position sizing and parameter tuning can achieve better results. The logic is clear and parameters are flexible for customization.

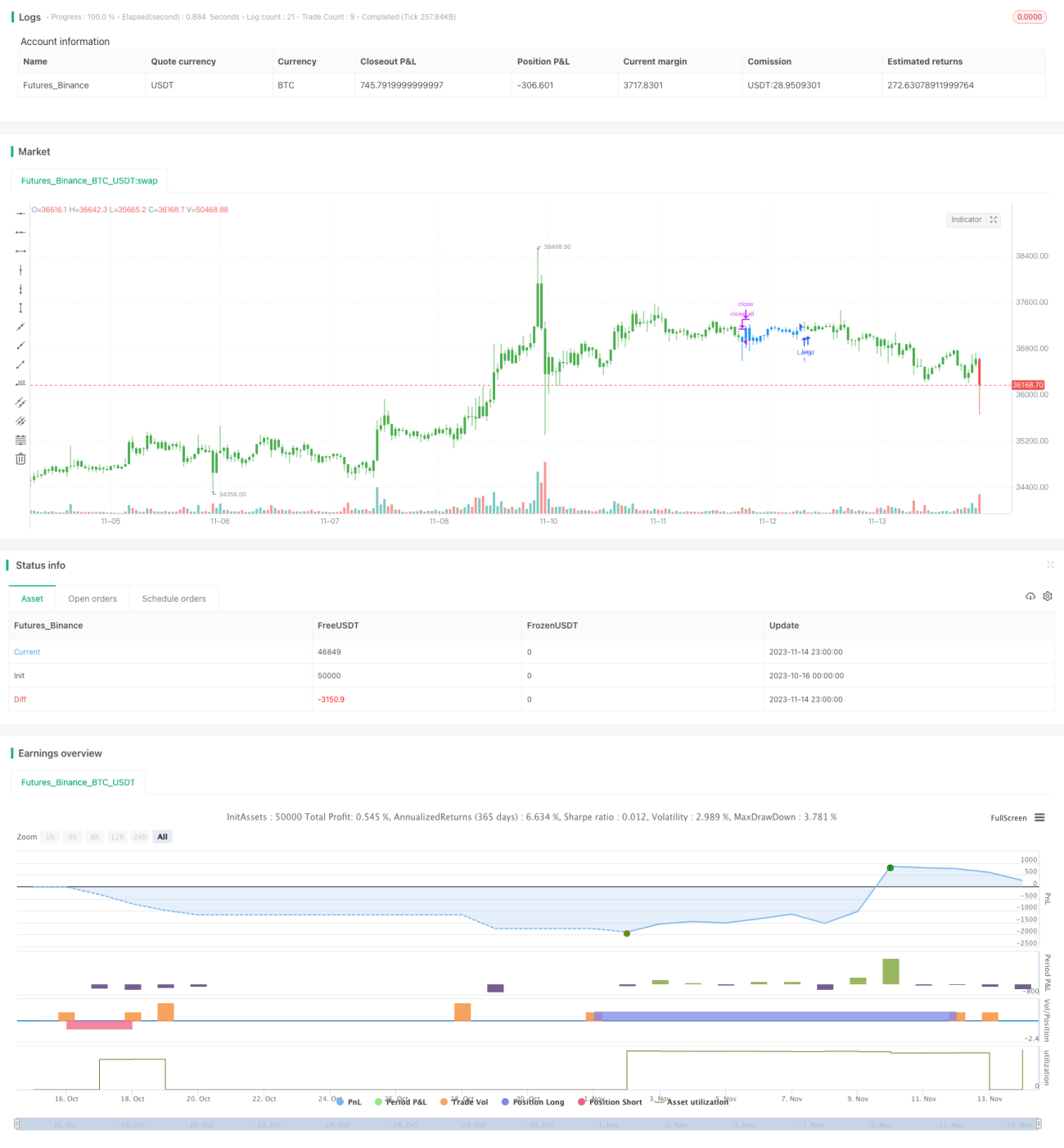

/*backtest

start: 2023-10-16 00:00:00

end: 2023-11-15 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 29/04/2019

// This is combo strategies for get - 1