Aligned Moving Average and Cumulative High Low Index Combination Strategy

Overview

This strategy mainly combines the High Low Index, Moving Average Index and Super Trend Index to determine the market trend and open positions.

Strategy Logic

-

The High Low Index judges whether the latest price over a certain period has made a new high or new low, and accumulates the score. When the score rises, it represents the strengthening of bullish forces. When the score falls, it represents the strengthening of bearish forces.

-

The Moving Average Index judges whether the price is in an upward ladder-shaped uptrend or a downward ladder-shaped downtrend. When the moving average shows a ladder-shaped rise, it represents the strengthening of bullish forces. When it shows a ladder-shaped decline, it represents the strengthening of bearish forces.

-

Combine the judgments of the High Low Index and the Moving Average Index to determine the market trend, and then find trading opportunities combined with the direction of the Super Trend Index. Specifically, when both the High Low Index and the Moving Average Index show strengthening bullish forces and the direction of the Super Trend Index is downward, open long positions. When both indices show strengthening bearish forces and the direction of the Super Trend Index is upward, open short positions.

Advantages

-

The High Low Index can effectively judge the price movement and changes in momentum. The Moving Average Index can effectively determine the price trend. The combination of both can more accurately determine the market direction.

-

Opening positions combined with the Super Trend Index can avoid premature or late opening of positions. The Super Trend Index can effectively identify price reversal points.

-

Multiple indicators verify each other and reduce false signals.

Risks

-

Incorrect signals from the High Low Index and Moving Average Index may lead to loss-making positions.

-

Insufficient participation and improper parameter settings of the Super Trend Index may generate incorrect signals.

-

Rapid trend reversals and improper stop loss settings may lead to large losses.

-

Risks can be reduced by optimizing indicator parameters, adjusting stop loss price levels, etc.

Optimization

-

Test different types of moving average indicators to find the optimal combination of parameters.

-

Optimize the parameters of the High Low Index and Moving Average Index to make the signals more stable and reliable.

-

Incorporate other indicators for verification, such as MACD, KD, etc., to reduce false signals.

-

Incorporate machine learning algorithms to automatically optimize parameters and signal weights.

-

Incorporate sentiment analysis to avoid trading less popular products.

Conclusion

This strategy determines market trends and momentum through the High Low Index and Moving Average Index, and then filters the signals using the Super Trend Index, opening positions when bullish and bearish forces confront each other and the Super Trend Index reverses. Its advantages lie in multiple signal verification and timely opening of positions, which can effectively control risks. Existing problems include false signals and trend misjudgment. Various improvements can be made through parameter optimization, stop loss settings, signal filtering, etc. to make the strategy more robust and reliable.

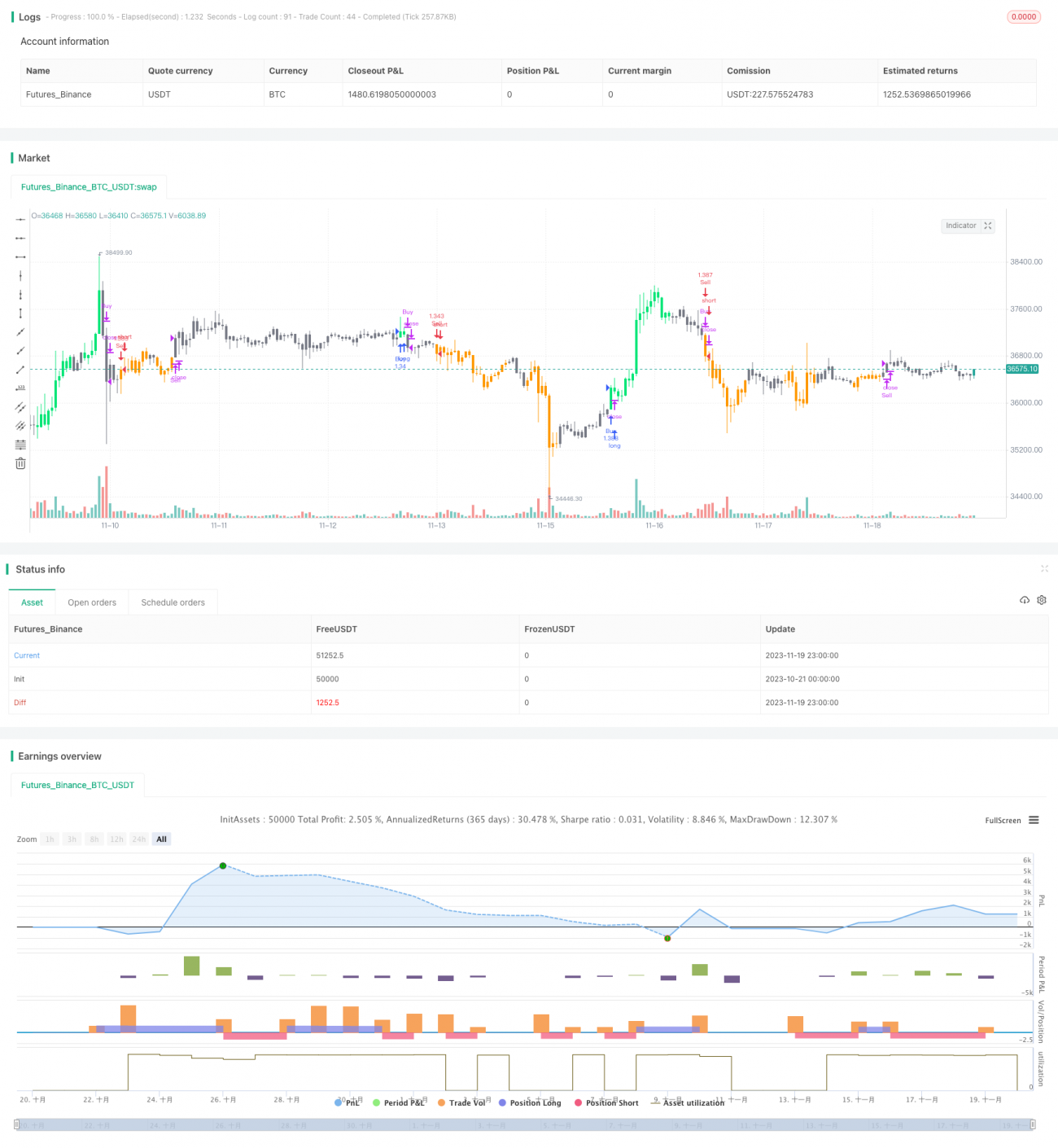

/*backtest

start: 2023-10-21 00:00:00

end: 2023-11-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1