Reverse Opening Engulfing Strategy

Overview

The Reverse Opening Engulfing Strategy is a simple intraday trading strategy based on the first candlestick after the opening. The core idea of this strategy is to judge the uptrend or downtrend of the first candlestick when it appears after the opening every day, and take counter operations. If the first candlestick is a red yang line, go long; if the first candlestick is a green yin line, go short. The strategy also sets up stop loss and take profit mechanisms for exiting positions.

Strategy Logic

The principle behind this strategy is the peculiarity of the first candlestick after opening. When the market opens, the forces of longs and shorts confront most intensely, and the probability of a reversal is relatively large. Judging the uptrend or downtrend of the first candlestick and taking counter operations is the core idea of this strategy.

Specifically, after the opening of a new day, the strategy will record the opening price, closing price and price change of the first candlestick. If the opening price is higher than the closing price (green yin line), it means the bears have won and we should long; if the opening price is lower than the closing price (red yang line), it means the bulls have won and we should short. By taking such counter operations, the strategy attempts to capture reversal opportunities after opening.

Meanwhile, the strategy also sets up stop loss and take profit mechanisms, including long stop loss price, long take profit price, short stop loss price and short take profit price, to control risks and profits of long and short positions, avoiding excessive losses or premature profit taking.

Advantage Analysis

The Reverse Opening Engulfing Strategy has the following advantages:

- The logic is simple and clear, easy to understand and implement.

- It utilizes the high predictive value of the opening segment to capture reversal opportunities.

- The stop loss and take profit settings can effectively control risks.

- The strategy idea has universality and is suitable for most stocks.

- The participation cost is relatively low and capital control is easy.

Risk Analysis

The Reverse Opening Engulfing Strategy also has some risks, mainly including:

- Probability of opening reversal failure. A failed reversal signal of the first candlestick may cause huge losses.

- Inability to effectively filter low-quality stocks. The strategy lacks sufficient fundamental analysis and may pick some stocks with poor fundamentals.

- Inability to effectively control systemic risks from black swan events, such as the impact of significantly negative news.

- Improper stop loss and take profit settings may lead to magnified losses or narrowed profits.

Optimization Directions

The Reverse Opening Engulfing Strategy can be optimized in the following aspects:

- Increase the validity test of opening reversal signals to avoid invalid signals, for example, combine volume analysis.

- Select stock pools by integrating fundamental and technical analysis to filter low-quality stocks.

- Add monitoring modules for major events and news to control systemic risks.

- Use genetic algorithms, machine learning and other methods to dynamically optimize stop loss and take profit settings.

Summary

The Reverse Opening Engulfing Strategy attempts to capture reversal opportunities after opening by judging the direction of the first candlestick and taking counter operations. The strategy idea is simple with low participation costs, and has some practical value. But we should also be soberly aware of the risks, and constantly improve and optimize the strategy in practice to make it more robust and reliable.

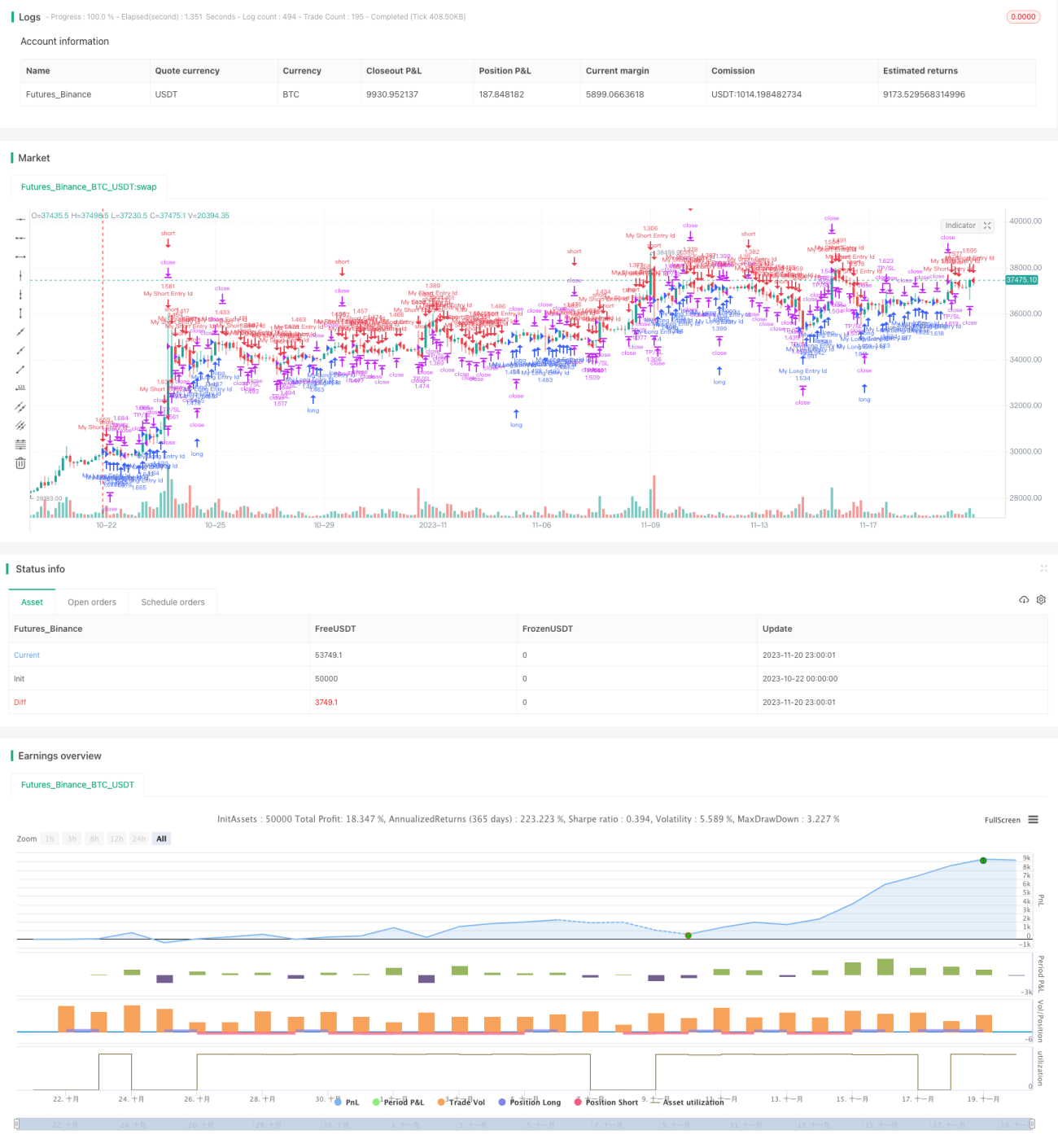

/*backtest

start: 2023-10-22 00:00:00

end: 2023-11-21 00:00:00

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © vikris

//@version=4

strategy("[VJ]First Candle Strategy", overlay = true,calc_on_every_tick = true,default_qty_type=strategy.percent_of_equity,default_qty_value=100,initial_capital=750,commission_type=strategy.commission.percent, - 1