Speculation Gulf : Trend Follow Strategy Based on SAR

Overview

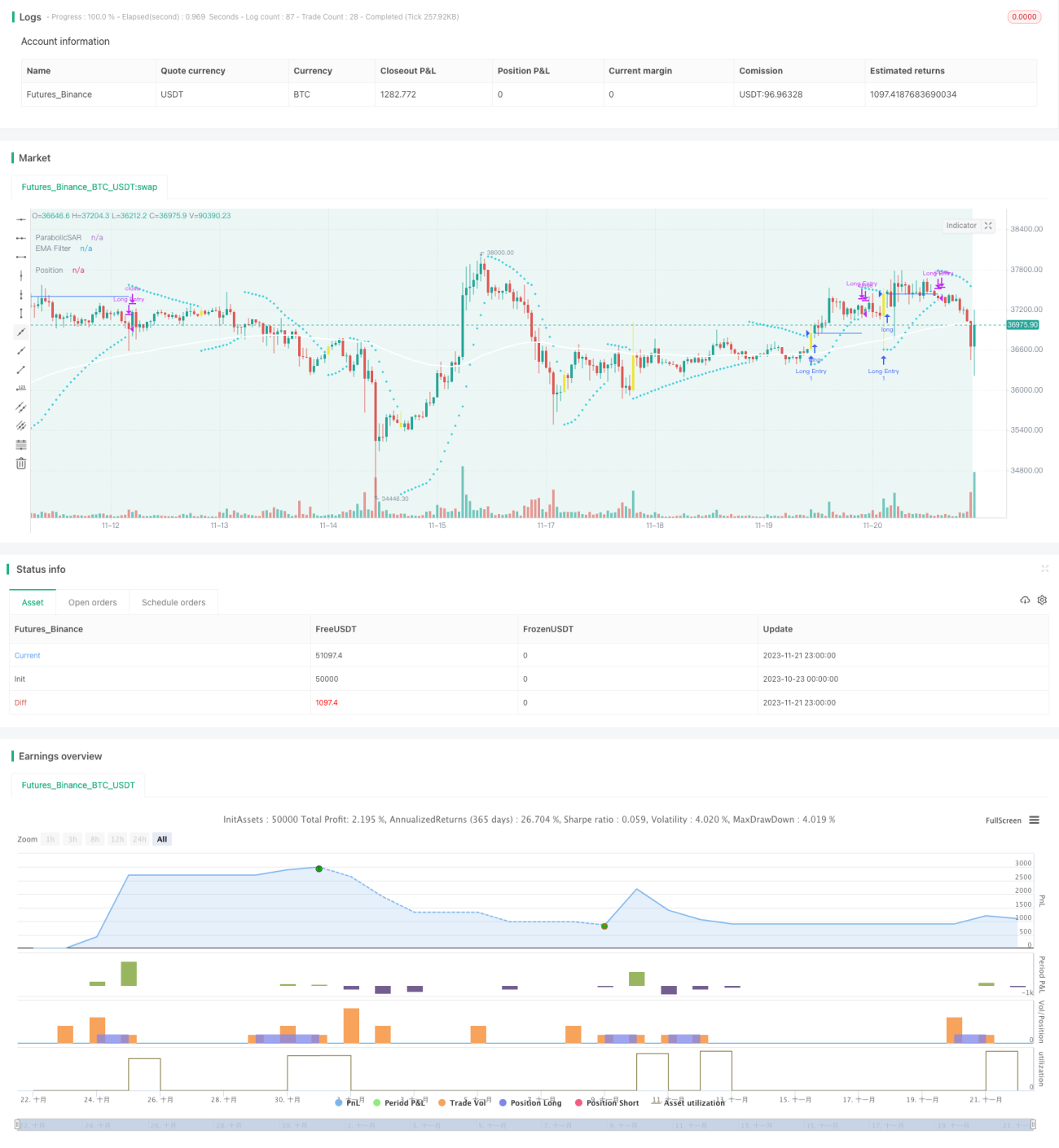

The Speculation Gulf strategy is a quantitative trading strategy that tracks trends. It uses the SAR Parabolic curve as the main trading signal, with additional EMA, Squeeze Momentum and Volatility Oscillator filters to identify trend reversal points with SAR parameters, and achieve low-risk trend tracking. This strategy is well suited for medium-to-long term investing.

Strategy Logic

The strategy uses Parabolic SAR as the primary trading signal indicator. SAR can effectively determine price trend reversal points. When the SAR sign changes, it means the trend has reversed. This strategy generally generates buy or sell signals when the SAR flips.

In addition, the strategy also provides a SAR breakout option - generating signals when the price breaks through the last SAR value before SAR fully flips. This further improves the sensitivity of the strategy.

To filter false signals, the strategy also introduces EMA, Squeeze Momentum and Volatility Oscillator as three auxiliary filters, which can be used alone or in combination to confirm the reliability of price trends and trading signals.

Finally, the strategy provides three types of stop loss methods - fixed stop loss, fixed take profit and risk reward ratio stop loss. This allows the strategy to flexibly adapt to the characteristics of different types of trading instruments.

Advantage Analysis

-

SAR can accurately determine price trend reversals and timely capture new price trends, suitable for medium and long term trend tracking.

-

Multiple filters reduce the probability of false breakouts and improve signal reliability.

-

Simple and flexible configuration, customizable parameters to suit different trading instruments.

-

Provides multiple types of take profit and stop loss to balance risk and reward.

-

Can directly connect to trading bots for automated trading.

Risk Analysis

-

In non-trending markets, there may be increased occurrences of false signals and ineffective trades.

-

Improper SAR parameter settings also affect the accuracy of signal judgments.

-

As a trend following strategy, significant fluctuations in the market can easily hit the stop loss line.

To address the above risks, appropriately adjust the SAR parameters or filter parameters to reduce the probability of invalid trades. Stop loss limits can also be moderately relaxed to withstand greater market fluctuations.

Optimization Directions

-

SAR Parameter Optimization. Optimize the SAR increment and step parameters through historical backtest data to obtain a more stable and efficient trading strategy.

-

Introduce Trend Judgment Indicators. Add auxiliary trend judgment indicators like MACD and DMI to improve trend judgment capabilities.

-

Optimize risk-return ratio. Adjust fixed stop loss percentage and risk-return ratio to take on higher risks for higher returns.

-

Support more instruments. Currently only crypto is supported, can be extended to support Forex, commodity and securities trading instruments.

Conclusion

The Speculation Gulf strategy is a very practical trend following quantitative strategy. It has responsive signals, reliable judgments and can achieve long-term steady returns through stop loss management. With appropriate parameter and rules optimization, the efficiency of the strategy can be further improved. This is an efficient quantitative strategy worth using long term.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1