Trend Following Strategy Based on Time Series Decomposition and Volume Weighted Bollinger Bands

1

Follow

1802

Followers

Overview

This strategy integrates time series decomposition, volume weighted average price, Bollinger Bands and delta(OBV-PVT) 4 technical indicators to make multidimensional judgments on price trends, overbought and oversold conditions.

Principles

- Use time series decomposition to remove noise and periodicity in prices for more accurate trend judgment;

- Calculate volume weighted new price based on the trend line;

- Calculate the Bollinger Bands Percentage Width (BB%B) of closing price to determine overbought and oversold conditions;

- Calculate the BB%B of Delta(OBV-PVT) as a measure of price-volume divergence;

- Generate trading signals based on price-volume indicators crosses and Bollinger Bands overshoots and undershoots.

Advantages

- Combines price, volume and statistical features for robust judgments;

- BB%B combined with Delta(OBV-PVT) better identifies short-term overbought/oversold conditions;

- Price-volume crossover signals filter out some false signals.

Risks

- Too complex parameter tuning;

- Short-term choppiness may increase losses;

- Price-volume divergences do not completely filter false signals.

Parameters like moving averages, Bollinger Bands widths and risk-reward ratios can be optimized to reduce trading frequency while improving risk-adjusted returns per trade.

Conclusion

Integrating tools like time series decomposition, Bollinger Bands, OBV indicators, this strategy combines price-volume relationships, statistical properties and trend analysis to identify short-term reversals and catch major trends. There are also certain risks that need to be addressed through parameter tuning for optimal performance.

Source

Pine

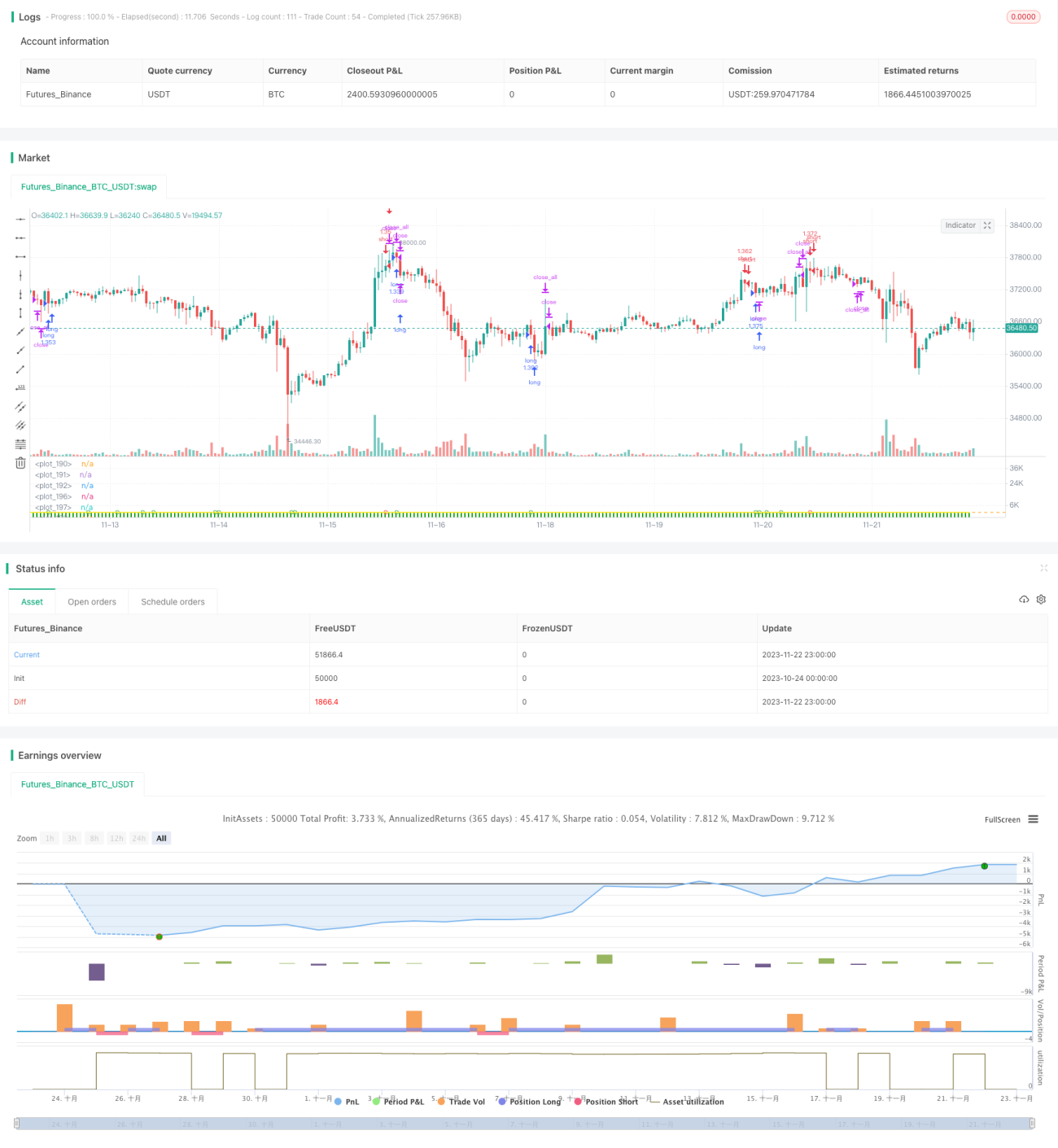

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © oakwhiz and tathal

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1