Dual Moving Average Arbitrage Strategy

Overview

This is an arbitrage strategy that utilizes dual moving average formations to make arbitrage trades. It combines the 123 reversal pattern and Finite Volume Elements (FVE) sub-strategies and makes arbitrage trades when they both give buy or sell signals simultaneously.

Strategy Logic

123 Reversal Pattern

This sub-strategy is from the book "How I Tripled My Money in the Futures Market" by Ulf Jensen. It gives signals under these conditions:

- Go long when close price rises for 2 consecutive days and 9-day slow stoch is below 50.

- Go short when close price falls for 2 consecutive days and 9-day fast stoch is above 50.

Finite Volume Elements (FVE)

FVE is a pure volume indicator. It judges if money is flowing in or out based on price movement range and trading volume.

It gives signals when the latest two bars of FVE indicator rise or fall together.

Advantage Analysis

This strategy combines two types of indicators to determine market trend and money flow, which can effectively avoid false signals. Also, both sub-strategies have some reversal characteristics, so arbitrage trades can make profits.

In addition, the dual moving average formation represents consistency between short-term and medium-term trends, thus having greater stability.

Risk Analysis

This strategy relies on moving average formations, which can easily generate false signals and lead to losses when the market fluctuates. Reversal failure is also a common risk.

Risks can be reduced by properly tweaking parameters to make the strategy more robust, or by setting stop loss to control risks.

Optimization Directions

More types of moving averages can be tested to find the optimal match. Other assist indicators like strength index and volatility index can also be introduced to avoid false signals.

In addition, research can be done on how to dynamically adjust parameters based on market conditions to improve adaptability. Machine learning and neural networks can also be explored for parameter self-adaptivity.

Summary

This dual moving average arbitrage strategy integrates two reversal-type indicators for judgement, which can mitigate risks to some extent. But reliance on moving average formations means further optimization is needed to make the strategy more robust. Overall, it provides a basic framework for short-term arbitrage trading and is worth further research.

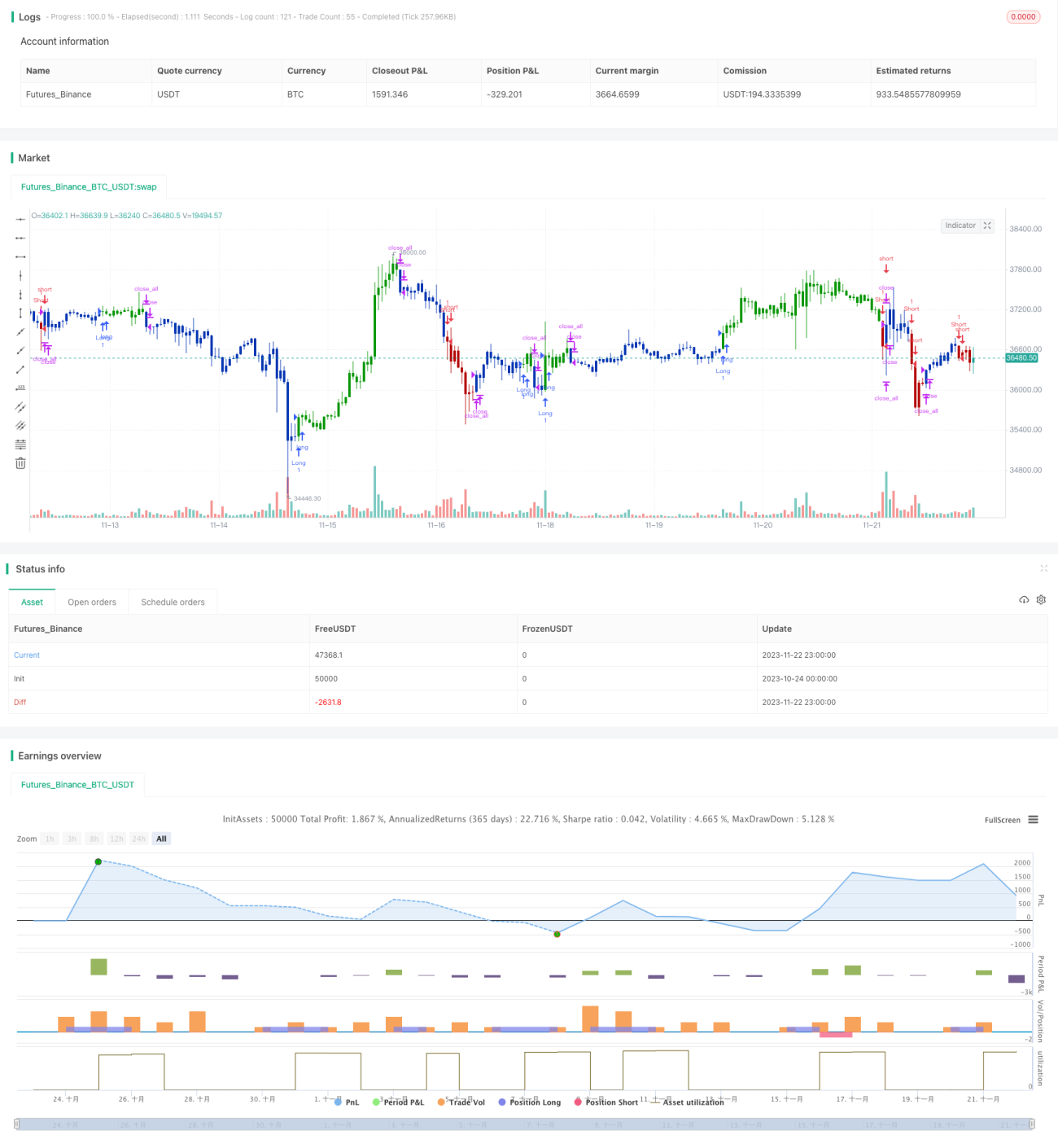

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/08/2020

// This is combo strategies for get a cumulative signal. - 1