Solid Moving Average System Strategy

Overview

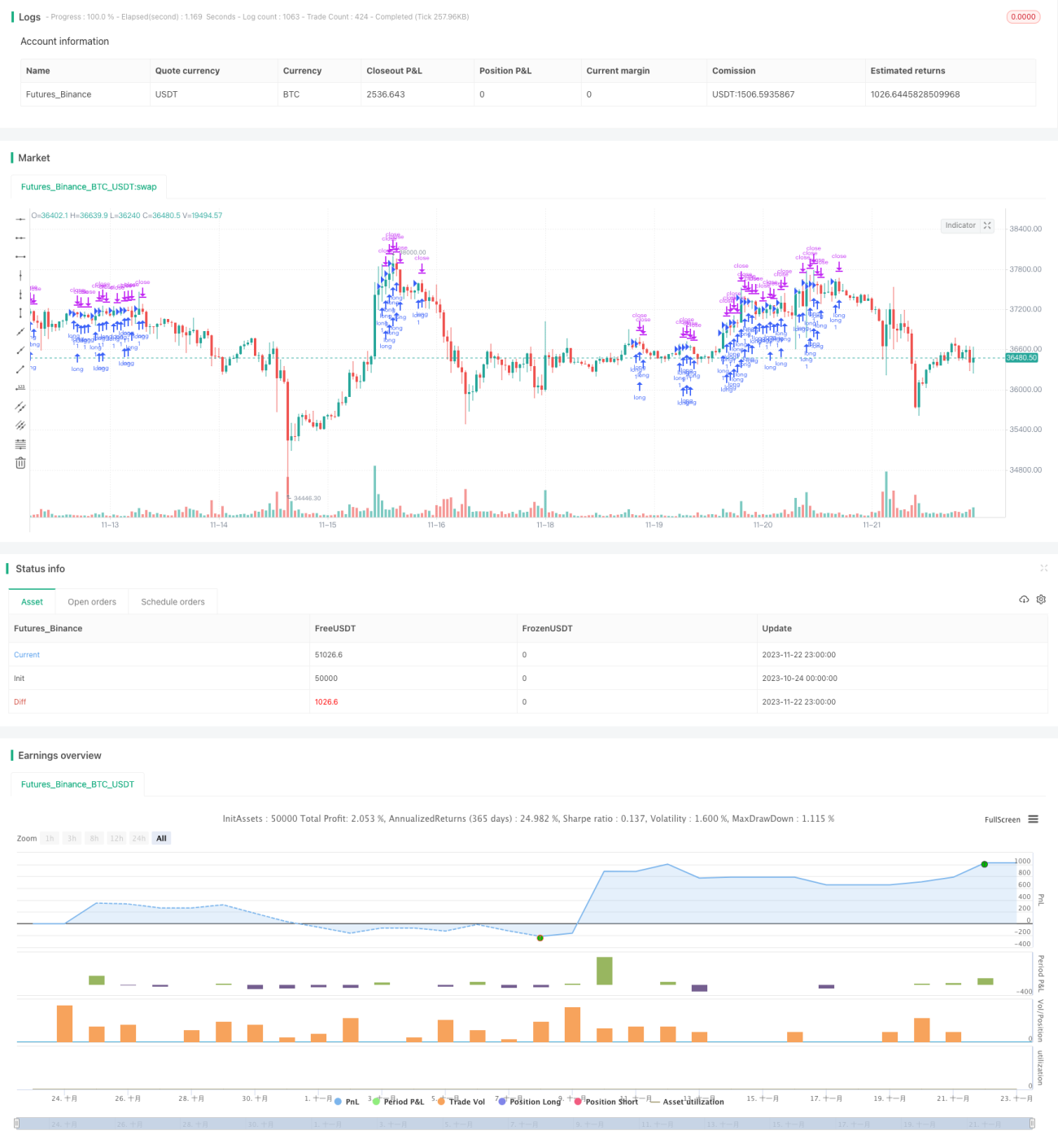

This strategy is a moving average system based on 4 SMMAs (Smoothed Moving Average) with different periods and 1 EMA indicator. It combines multiple technical analysis tools to form a trading strategy through trend judgment. This strategy is mainly suitable for high leverage EURUSD 15-minute bonds intraday trading.

Strategy Principle

The strategy uses 4 SMMAs with different parameters (3, 6, 9, 50) and 1 EMA (200) to build a multi-level moving average system. The SMMA indicator can effectively filter market noise and determine the trend direction. The EMA indicator detects long-term trends. The specific trading logic is:

When the short-period moving average (such as 3-period SMMA) crosses above the longer-period moving average (such as 200-period EMA), a buy signal is generated. When the short-period moving average crosses below the longer-period moving average, a sell signal is generated. By judging the arrangement of multiple moving averages, the trend direction is determined.

In addition, the strategy also sets stop profit and stop loss points to control risks.

Advantage Analysis

The strategy has the following advantages:

-

The multi-level moving average structure can effectively determine the trend direction and reduce false signals.

-

The SMMA indicator effectively filters market noise, and the EMA indicator detects long-term trends.

-

It is suitable for high leverage accounts to amplify trading profits.

-

Stop profit and stop loss points are set to effectively control risks.

-

Optimizes trading varieties (EURUSD) and cycles (15 minutes) to make it more advantageous.

Risk Analysis

The strategy also has the following risks:

-

The large amount of moving averages may miss short-term reversal opportunities.

-

High leverage amplifies losses while amplifying profits.

-

When the moving average generates a signal, the short-term trend may have already reversed.

-

EURUSD exchange rate may experience violent fluctuations, bringing greater risks.

In response to these risks, we can appropriately adjust the leverage ratio, optimize the parameters of the moving average, introduce other indicators to judge trend reversal, etc. for optimization.

Optimization Directions

The main optimization directions of this strategy include:

-

Evaluate the performance of different varieties and cycles and select the optimal parameters.

-

Test different combinations and quantities of moving averages.

-

Increase volume or volatility indicators to determine short-term reversal points.

-

Increase dynamic adjustment of stop profit and stop loss range.

-

Add ENU indicator to determine reversal point.

Through multi-faceted testing and optimization, the stability and profitability of the strategy can be greatly improved.

Summary

This moving average strategy integrates the advantages of moving average indicators to form a robust trend judgment system. It optimizes trading varieties and cycles and is very suitable for high leverage intraday trading. Through parameter adjustment and optimization testing, this strategy can become an efficient and reliable algorithm trading strategy.

- 1