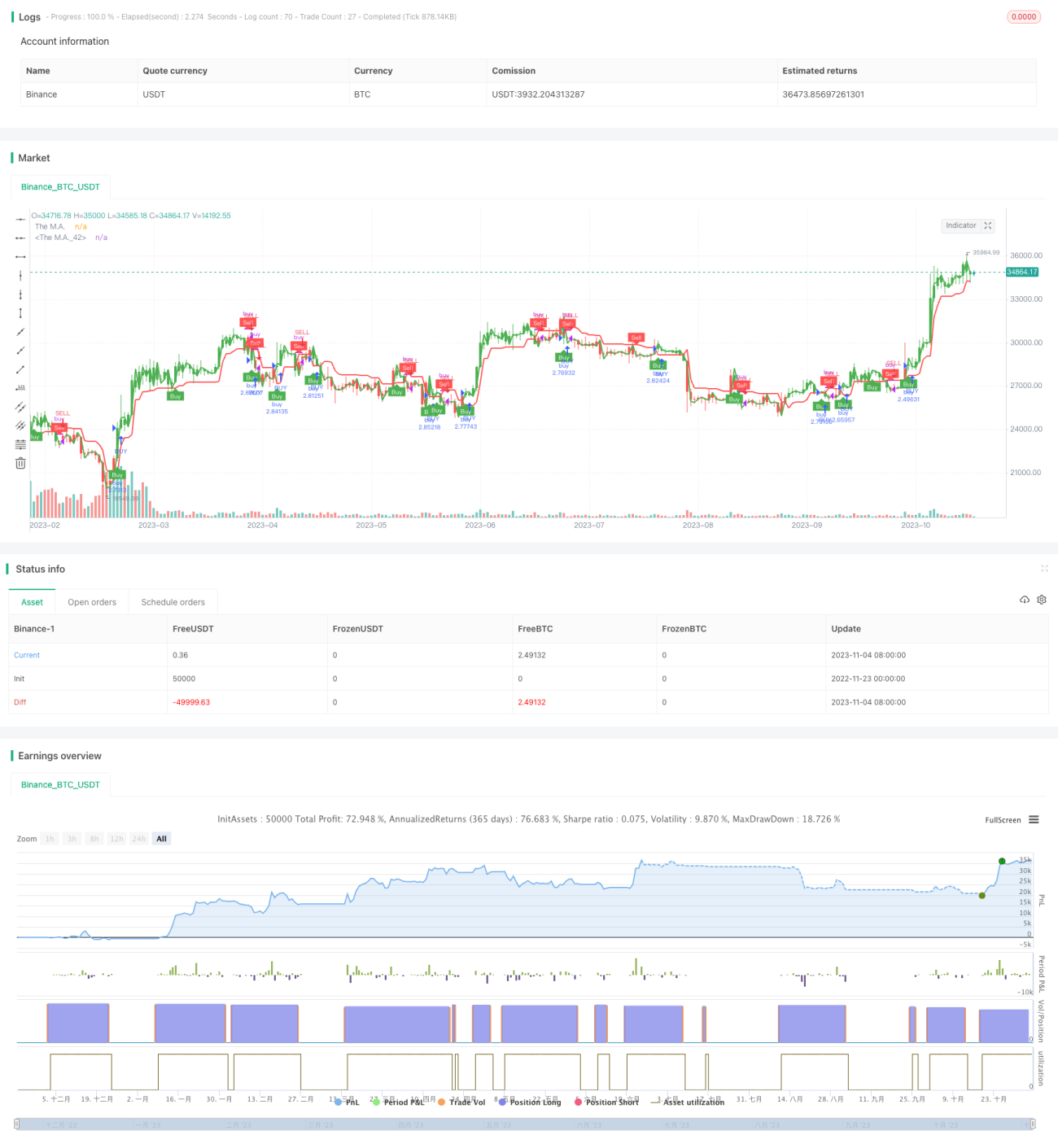

概述

该策略的核心思想是利用动态移动平均线进行趋势跟踪,设置止损止盈,并结合海克林蜡烛技术指示做多空信号判断。ATR指标用于计算动态移动平均线和止损位置。

策略原理

该策略首先计算ATR指标,然后结合输入的价格源和参数,计算出动态移动平均线。当价格高于/低于动态移动平均线时产生做多/空信号。同时设置止损止盈位置,跟踪价格变动实时更新。

具体来说,首先计算ATR指标及参数nLoss。然后计算当前周期价格及上一周期的止损位置,比较两者更新止损线。当价格突破上一周期止损线时产生做多/空信号pos和相应颜色;交易信号产生时,画出箭头标记。最后根据止损止盈逻辑平仓。

优势分析

该策略最大的优势在于利用动态移动平均线实时跟踪价格变化。这比传统固定移动平均线更能捕捉趋势,降低止损可能性。另外结合ATR止损,可以根据市场波动幅度灵活调整止损位置,有效控制风险。

风险及解决方法

该策略主要风险在于价格可能会有较大跳空,从而突破止损线产生错误信号。此外,条件设置不当也可能导致过于频繁交易。

解决方法是优化移动平均线期数,调整ATR和止损系数大小,降低错误信号概率。另外可以设置过滤条件,避免过于密集交易。

优化方向

该策略可以从以下方面进行优化:

-

测试不同类型和周期的移动平均线,找到最佳参数组合

-

优化ATR周期参数,平衡止损灵敏度

-

添加额外过滤条件和指标,提高信号质量

-

调整止损止盈数值,优化收益风险比

总结

本策略核心思路是动态移动平均线实时跟踪价格变化,运用ATR指标动态设置止损位置,在跟踪趋势的同时严格控制风险。通过参数优化和规则修正,可以将该策略调教成一个非常实用的量化系统。

策略源码

Pine

/*backtest

start: 2022-11-23 00:00:00

end: 2023-11-05 05:20:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BTC_USDT","stocks":0}]

*/

//@version=5

strategy(title='UT Bot v5', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

//Edited and converted to @version=5 by SeaSide420 for Paperina策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1