Fast RSI Gap Trading Strategy for Cryptocurrencies

Overview:

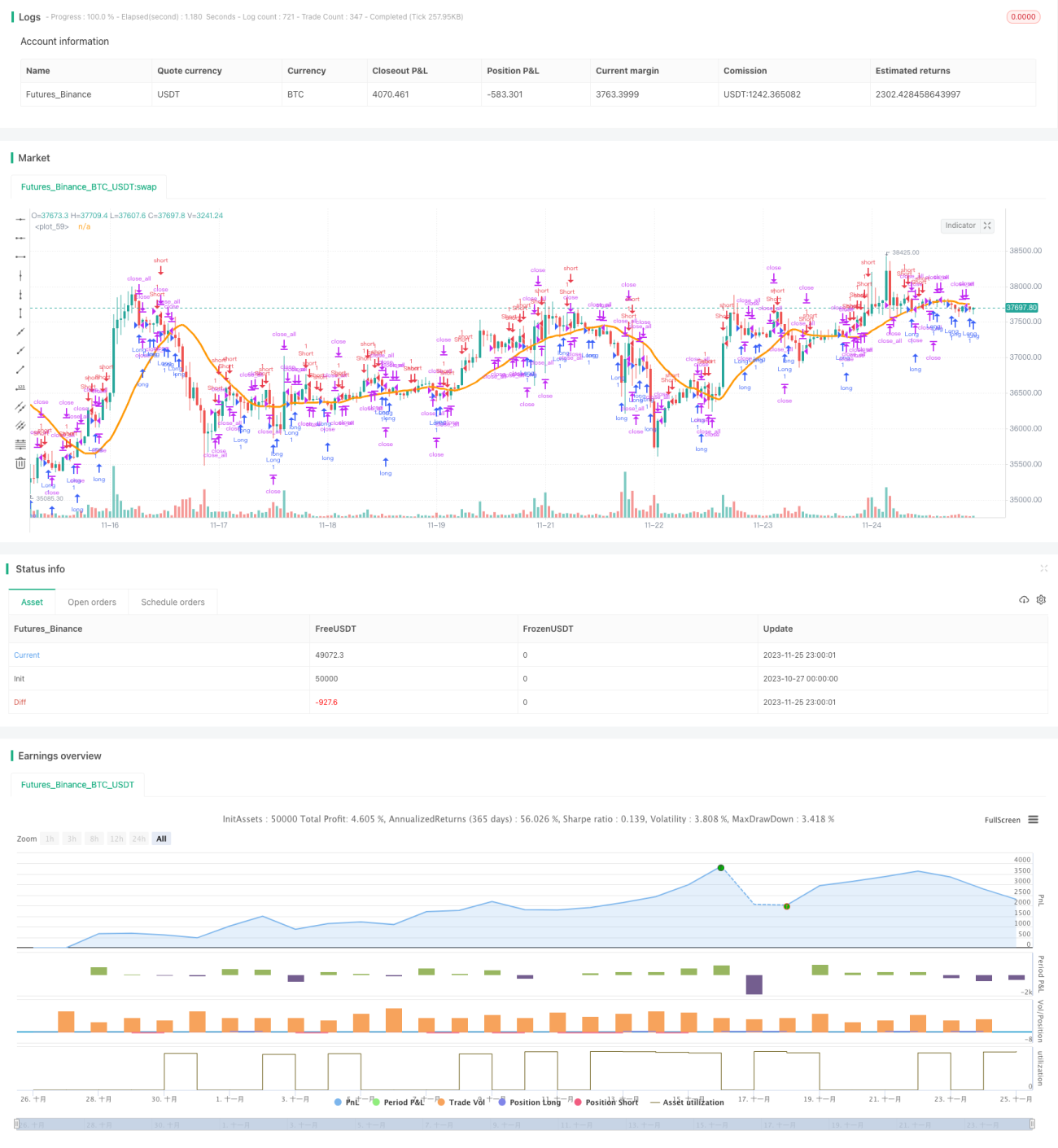

This is a fast RSI gap trading strategy designed for cryptocurrency markets. It utilizes both fast RSI indicators and gap patterns on candlestick charts to locate trading opportunities.

Principles:

The strategy uses two main techniques: fast RSI indicators and gap patterns.

Firstly, it calculates a fast RSI indicator based on only 7 candlesticks. This makes the RSI more sensitive in order to quickly detect overbought/oversold conditions. The RSI upper limit is set at 70 and lower limit at 30. Above 70 is considered overbought while below 30 oversold.

Secondly, it detects gap patterns on candlestick charts. Gaps refer to empty spaces between the current opening price and the previous closing price. Gaps signal high volatility and potential trend reversals.

When a down gap appears while the fast RSI shows oversold condition, go long. When an up gap emerges while the fast RSI indicates overbought status, go short.

In addition, the strategy utilizes other filters including SMA and Min/Max indicators to avoid false signals. Only when passing the filters will actual trading signals be triggered.

Advantages:

The biggest advantage of this strategy is catching ultra fast overbought/oversold turns and gap reversal opportunities. It is especially suitable for highly volatile crypto markets to seize quick trend shifts. Compared to regular RSI, the fast RSI reacts much quicker fitting the high frequency nature of crypto trading. The additional filters also help to remove false signals and improve reliability.

Risks:

The main risks facing the strategy include:

-

The fast RSI may be overly sensitive, causing excessive false signals.

-

The gaps may just be normal price swings instead of real reversals. The strategy could suffer stop loss risks.

-

During low volatility periods, positions may be kept idle for extended times.

-

Improper parameter settings like Min/Max period could lead to diluted signals and low efficiency.

Accordingly, the following methods could help mitigate the above risks:

-

Adjust fast RSI parameters and increase RSI period to make it less sensitive.

-

Apply dynamic stop loss to lock in profits. Avoid chasing gap spikes.

-

Optimize strategy participation rate. Limit involvement during low volatility environments.

-

Continually backtest and optimize parameters to ensure robust settings.

Enhancement:

The main optimization directions include:

-

Explore other indicators like MACD, KDJ combined with gaps to enhance precision.

-

Build adaptive stop loss mechanisms based on market volatility.

-

Incorporate volume indicators like OBV to confirm reversal after gaps.

-

Optimize filter parameters like Min/Max period to discover best settings to lower false signals.

-

Research adaptiveness of parameters across different crypto assets.

These efforts could significantly improve the strategy’s stability, adaptiveness and reliability.

Conclusion:

In summary, the fast RSI gap trading strategy is an efficient approach designed explicitly for volatile crypto markets. By continuous testing and enhancement, it has the potential to reliably catch quick market reversals and achieve consistent profitability.

- 1