Alpha Trend Strategy with Trailing Stop Loss

Overview

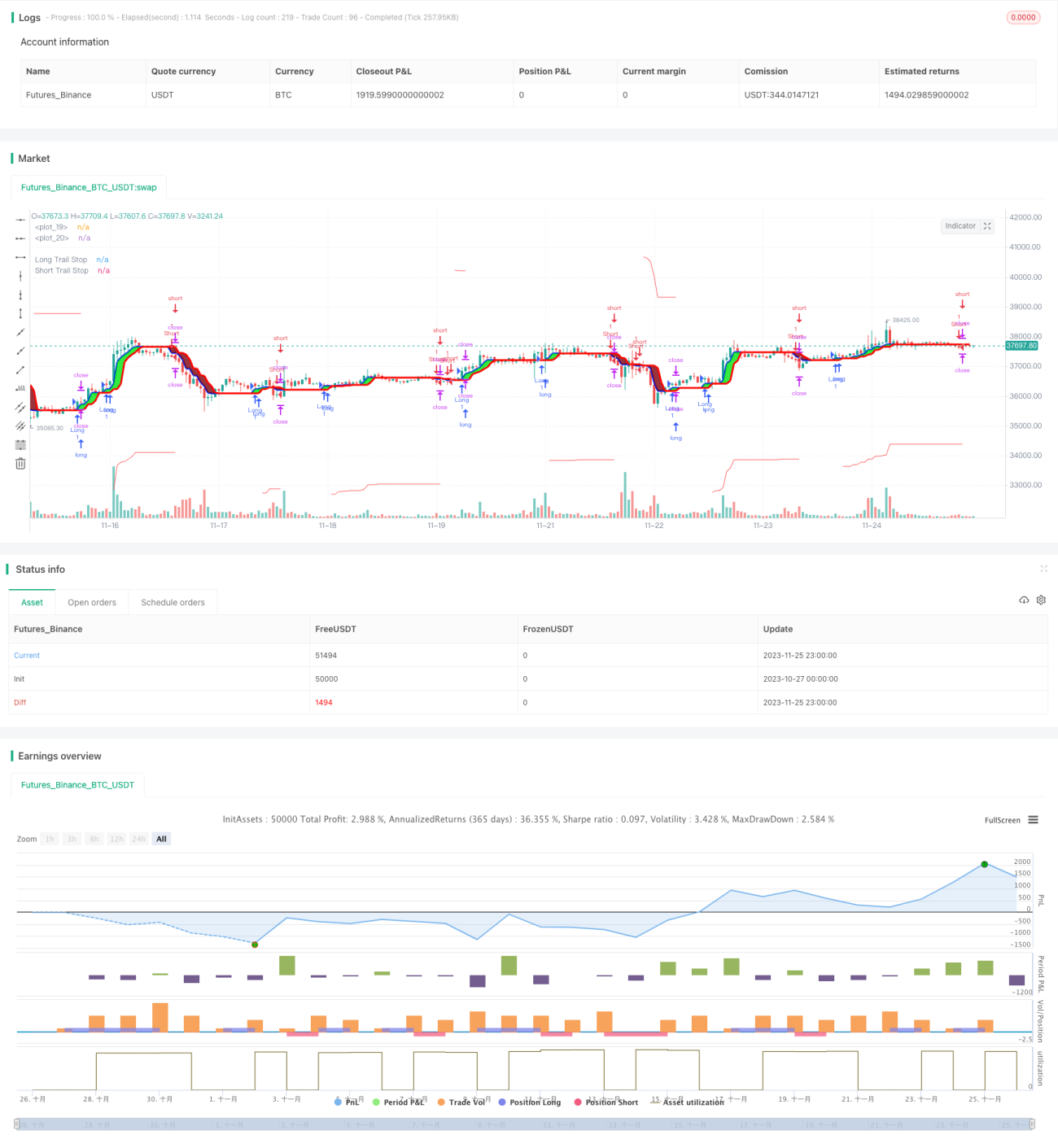

The Alpha Trend Strategy with Trailing Stop Loss is an enhanced version of the Alpha Trend Strategy by incorporating a trailing stop loss mechanism, which can control risks more effectively and improve overall returns.

Strategy Logic

The strategy first uses the Alpha indicator to determine price trends. When the Alpha indicator goes up, it is a bullish signal. When the Alpha indicator goes down, it is a bearish signal. The strategy generates buy and sell signals based on the golden cross and dead cross of the Alpha indicator.

Meanwhile, a trailing stop loss mechanism is enabled. The trailing stop loss level defaults to 10% of the closing price of the day. When holding long positions, if the price falls below the stop loss level, the strategy will exit the position to stop loss. Similarly for short positions. This helps better lock in profits and reduce risks.

Advantage Analysis

-

The Alpha trend has stronger capabilities of determining price trends than simple moving averages and other indicators.

-

By enabling trailing stop loss, single-trade loss can be effectively controlled, lowering risks.

-

This strategy has strong risk control abilities. Even in unfavorable market conditions, losses can still be minimized.

-

With fewer reference inputs, this strategy is efficient to calculate, suitable for high frequency trading.

Risk Analysis

-

In sideways range-bound markets, the strategy may generate many unnecessary trading signals, increasing trading costs and slippage losses.

-

When enabling trailing stop loss, the stop loss percentage needs to set appropriately. An excessively high or low percentage will both be unfavorable for the strategy's profitability.

-

In violently fluctuating prices, the probability of stop loss being triggered will significantly rise, increasing the risk of being locked in positions.

-

When optimizing the stop loss parameters, various factors including the underlying's characteristics and trading frequency should be considered, not just pursuing maximum returns.

The above risks could be alleviated by adjusting the Alpha indicator parameters, setting DYNAMIC stop loss, shortening trading cycle lengths, etc.

Optimization Directions

-

Different indicator parameters can be tested to find more suitable Alpha indicator parameter combinations.

-

Attempt to set stop loss percentages dynamically based on ATR to better adapt to market fluctuations.

-

Combine with other indicators such as MACD, KD to filter out some false signals.

-

Parameters can be automatically optimized based on live trading and backtesting results, using machine learning techniques to improve the intelligence of parameter selection.

Conclusion

The Alpha Trend Strategy with Trailing Stop Loss combines trend determination and risk control. It can effectively identify price trends and lock in profits to reduce risks. Compared to simple trend tracking strategies, this strategy can obtain higher steady returns. With various aspects of optimization, it has the potential to achieve even better performance.

/*backtest

start: 2023-10-27 00:00:00

end: 2023-11-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// author © KivancOzbilgic

// developer © KivancOzbilgic

//@version=5- 1