Bitcoin Quantitative Band Trading Strategy Based on Multiple Timeframes

1

Follow

1802

Followers

Overview

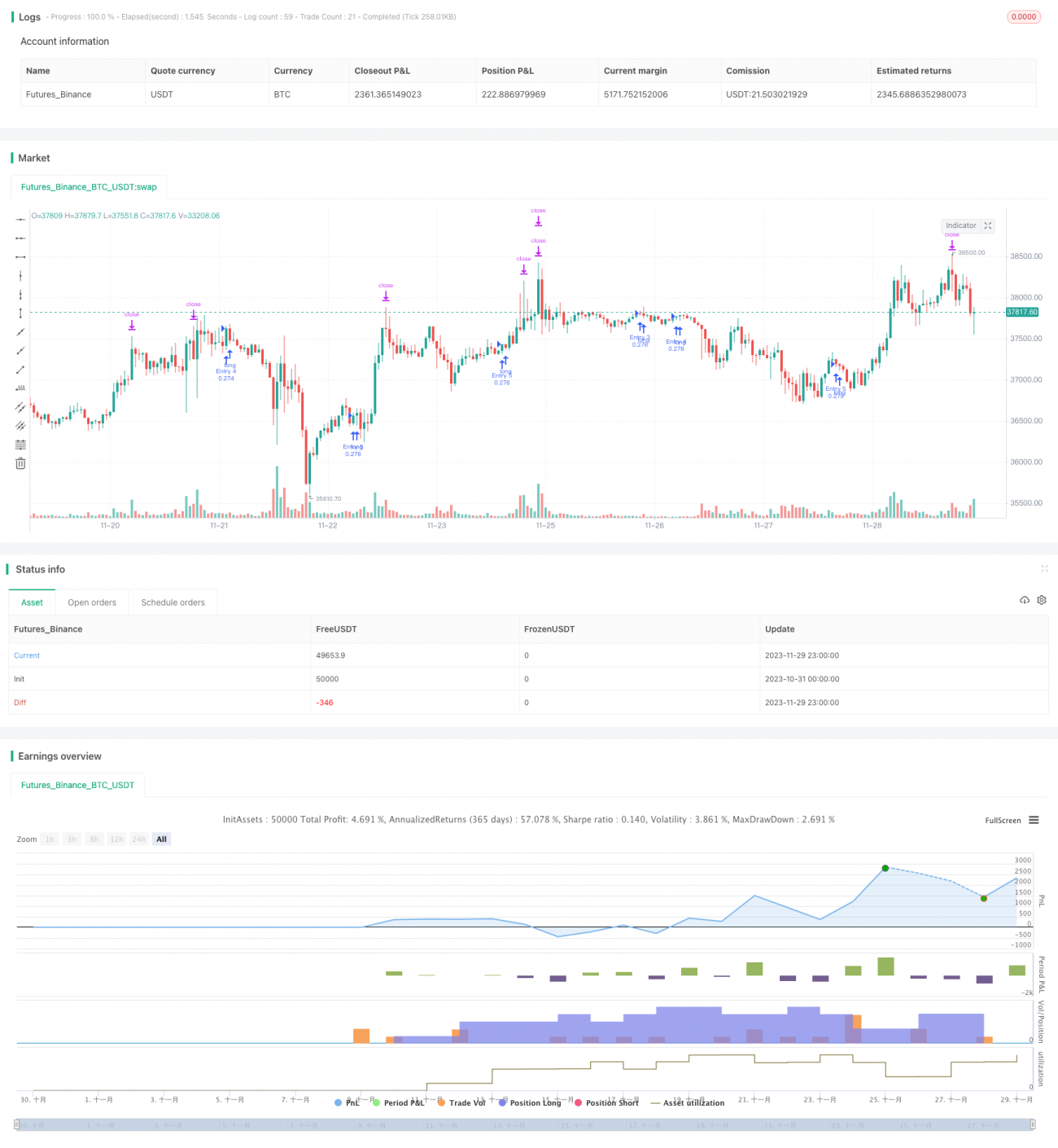

This strategy identifies the price bands of Bitcoin by combining quantitative indicators across different timeframes, and conducts trend tracking trades. It adopts the 5-minute timeframe and aims for long-term holding of bands for profit.

Strategy Logic

- The RSI indicator calculated based on the daily timeframe weighs based on trading volume to filter false breakouts.

- The daily RSI indicator is smoothed by an EMA to build a quantitative band indicator.

- The 5-minute timeframe uses a combination of Linear Regression and HMA indicators to generate trading signals.

- By combining the quantitative band indicator and trading signals across timeframes, the strategy identifies mid-to-long-term price bands.

Advantage Analysis

- The volume-weighted RSI indicator can effectively identify true bands and filter false breakouts.

- The HMA indicator is more sensitive to price changes and can capture turns timely.

- Combining multiple timeframes leads to more accurate identification of mid-to-long-term bands.

- Trading on the 5-minute timeframe allows higher operation frequency.

- As a band tracking strategy, it does not require accurate picking of points and can hold for longer periods.

Risk Analysis

- Quantitative indicators may generate false signals, fundamental analysis is recommended.

- Bands may see midway reversals, stop-loss mechanisms should be in place.

- Signal delays may lead to missing best entry points.

- Profitable bands need longer holding periods, requiring capital pressure tolerance.

Optimization Directions

- Test effectiveness of RSI indicators with different parameters.

- Try introducing other auxiliary band indicators.

- Optimize HMA indicator length parameters.

- Add stop loss and take profit strategies.

- Adjust holding cycle for band trades.

Conclusion

This strategy effectively captures Bitcoin's mid-to-long-term trends by coupling timeframes and band tracking. Compared to short-term trading, mid-to-long-term band trading sees smaller drawdowns and greater profit potential. Next steps involve further enhancing profitability and stability through parameter tuning and risk management additions.

Source

Pine

/*backtest

start: 2023-10-31 00:00:00

end: 2023-11-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title='Pyramiding BTC 5 min', overlay=true, pyramiding=5, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=20, commission_type=strategy.commission.percent, commission_value=0.075)

//the pyramide based on this script https://www.tradingview.com/script/7NNJ0sXB-Pyramiding-Entries-On-Early-Trends-by-Coinrule/Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1