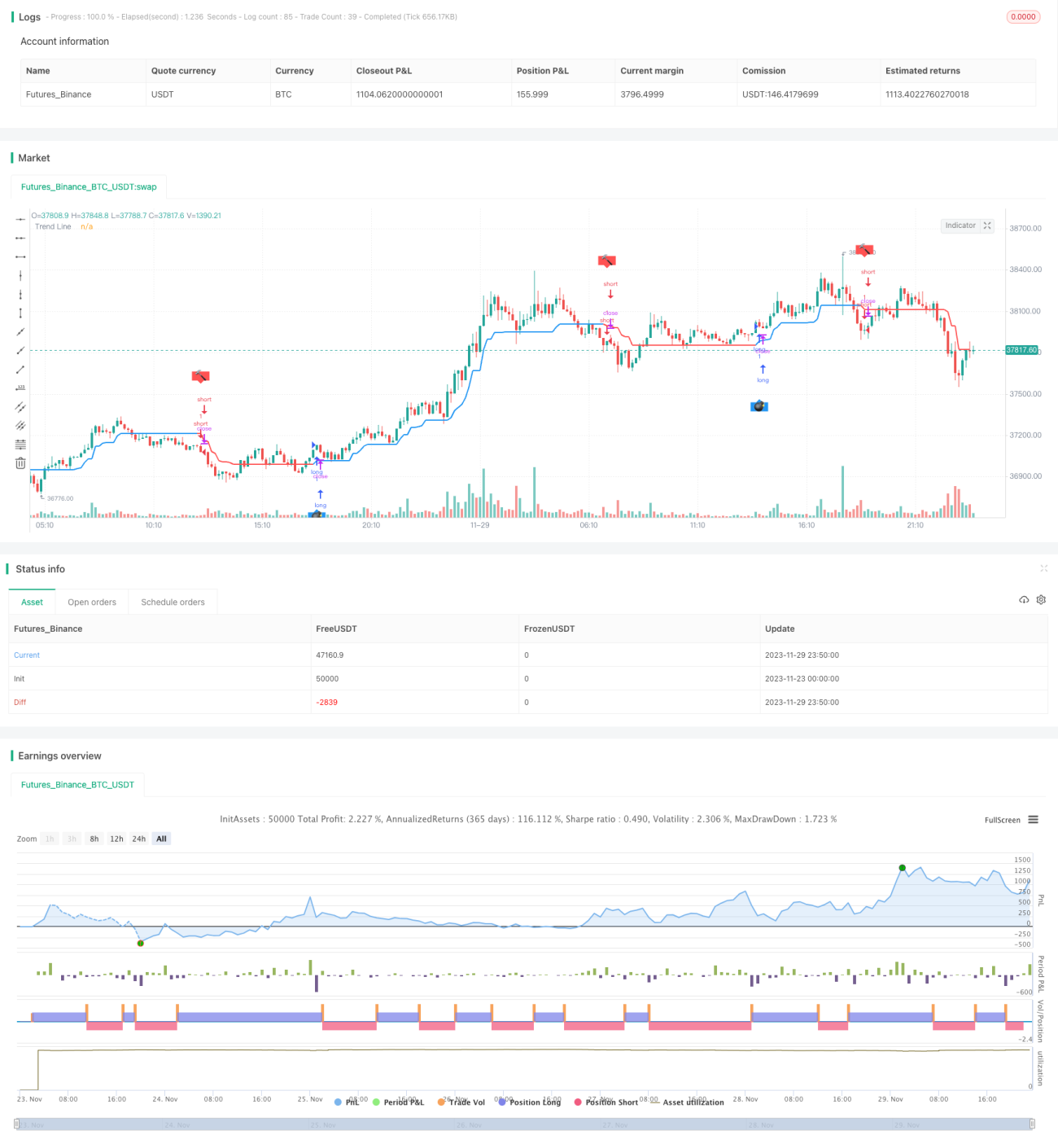

Follow Line Strategy

Overview

The Follow Line strategy is a trend tracking strategy based on Bollinger Bands and Average True Range (ATR). It dynamically adjusts the trend judgment line to track the trend by shifting it up when price breaks above Bollinger Bands upper band and shifting it down when price breaks below Bollinger Bands lower band.

Strategy Logic

The strategy first calculates the upper and lower bands of Bollinger Bands, as well as Average True Range. Then it judges whether price breaks above the Bollinger upper band or below the lower band.

When price breaks above the upper band, if ATR filter is enabled, the trend line is set to the lowest price minus ATR. If ATR filter is disabled, the trend line is set directly to the lowest price.

When price breaks below the lower band, if ATR filter is enabled, the trend line is set to the highest price plus ATR. If ATR filter is disabled, the trend line is set directly to the highest price.

Thus, the trend judgment line can be dynamically adjusted based on the price breakouts of Bollinger Bands to track the trend.

When current trend line is higher than previous one, it indicates an upward trend. When current trend line is lower than previous one, it indicates a downward trend.

Trading signals can then be generated based on the trend judgment to go long or short.

Advantages Analysis

- Dynamically adjusting trend line can flexibly capture price trends

- Combining with Bollinger Bands can timely judge trend reversal on band breakouts

- Introducing ATR filter can avoid some false breakout signals

Risk Analysis

- Improper BB parameters may cause frequent false breakouts

- Excessive ATR parameter may miss trend reversal opportunities

- Need to consider stop loss to prevent losses from extreme moves

Some risks can be mitigated via parameter tuning, introducing stop loss. Can also combine with other indicators for signal filtering to improve breakout validity.

Optimization Directions

- Optimize BB and ATR parameters to find best configurations

- Add other indicators to filter false breakouts

- Select BB and ATR periods based on specific trading instruments

Conclusion

The Follow Line strategy aims to capture price trends in volatile markets. It is an effective trend tracking strategy. Proper parameter tuning and optimizations can lead to decent profits. However, risks need to be managed via stop loss and preventing false breakouts. It is recommended to combine this strategy with other indicators or strategies to further improve profitability.

/*backtest

start: 2023-11-23 00:00:00

end: 2023-11-30 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Dreadblitz

//@version=4

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒ //- 1