Cross Moving Average Golden Cross Death Cross Strategy

This is a very classic moving average golden cross death cross strategy. The strategy utilizes two moving averages, TENKAN and KIJUN, with different time periods to form golden cross and death cross signals for long and short trades.

Strategy Logic

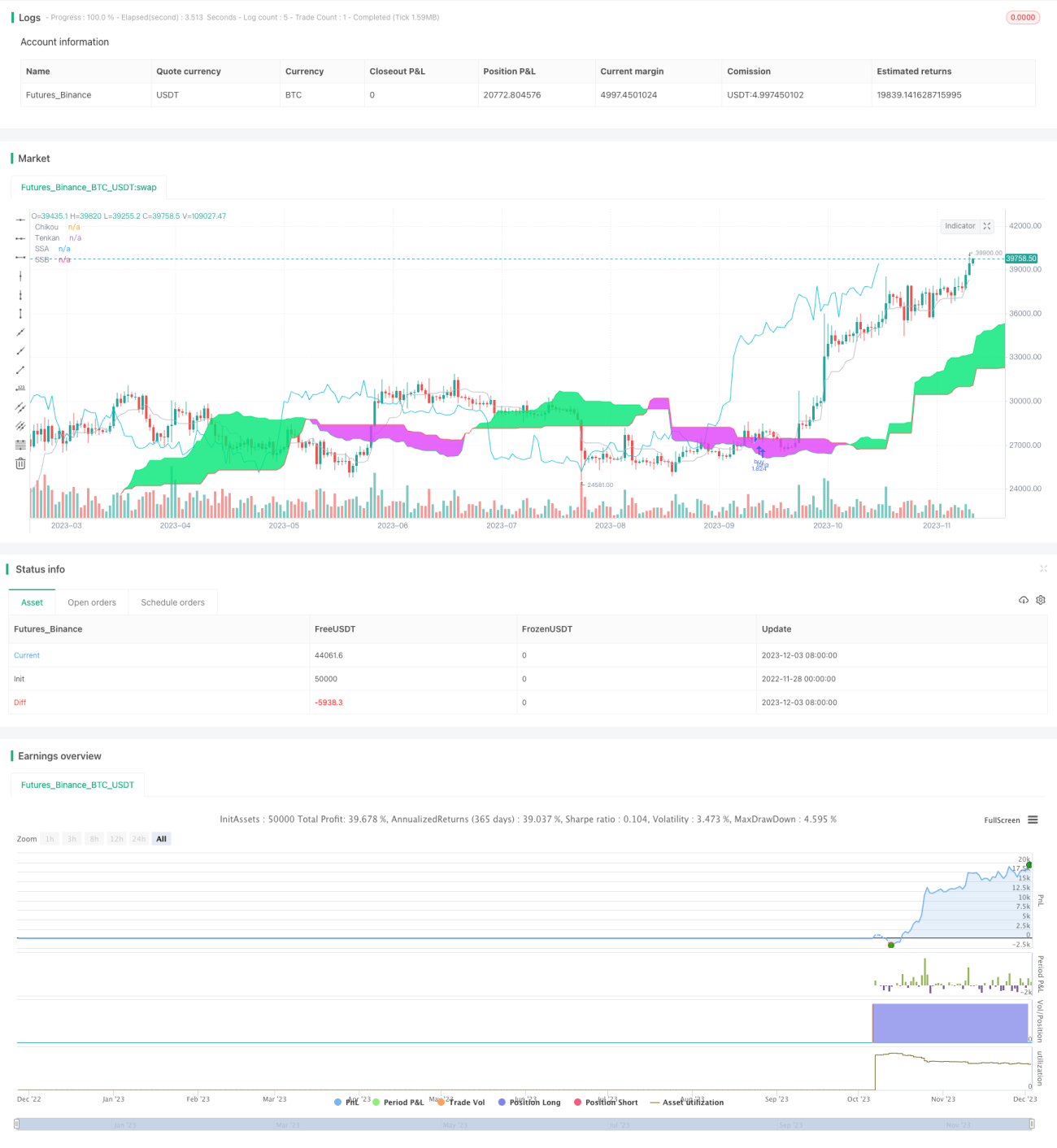

The strategy is mainly based on a Japanese stock technical analysis method called Ichimoku Kinko Hyo, using multiple moving averages like the TENKAN and KIJUN lines to determine the market trend direction.

Firstly, the TENKAN line is a 9-day line representing the short-term trend; the KIJUN line is a 26-day line representing the medium-term trend. When the TENKAN line crosses above the KIJUN line, a buy signal is generated. When the TENKAN line falls below the KIJUN line, a sell signal is generated. This forms the classic moving average golden cross and death cross strategy.

Secondly, the strategy also introduces the Senkou Span A (SSA) line and the Senkou Span B (SSB) line. The SSA line is the average of TENKAN and KIJUN lines while the SSB line is a 52-day moving average. Together they form the "Kumo" (cloud) bands that determine the long-term trend direction - price above the cloud signifies an uptrend while price below the cloud signifies a downtrend.

Lastly, to filter fake signals, this strategy also examines the position of price compared to the Chikou Span (the closing price delayed by 26 days) – only generating buy signals when the price is below Chikou and sell signals when the price is above Chikou.

Benefits

This is a very typical moving average strategy. The main advantages lie in:

-

Using two moving averages of different periods effectively judges short-term and medium-term trend directions simultaneously.

-

Long-term trends are determined with the Kumo bands to avoid buying in long-term bear markets.

-

Comparing prices with the delayed Chikou line filters out a lot of fake signals and reduces unnecessary trades.

By skillfully utilizing various functions of moving averages, this strategy can follow trends across short, medium and long timeframes.

Risks

The main risks of this strategy include:

-

Moving average strategies tend to produce many fake signals. Frequent trading caused by inaccurate parameters may lead to losses.

-

This strategy focuses heavily on technicals without considering fundamentals. Major changes in business performance or market policies may invalidate the technical signals.

-

No stop loss mechanism is included. Once the market direction judgment is wrong, losses can accumulate.

Therefore, we need more advanced moving average systems, proper stop loss rules, or supplemental fundamental signals, to further refine this strategy and decrease risks.

Enhancement Opportunities

This strategy can also be improved in the following aspects:

-

Search for more stable and efficient parameter sets through more backtests.

-

Add stop loss rules. Reasonable stop loss helps effectively control maximum losses.

-

Supplement fundamental signals like earnings estimate revisions which contain insights on a company's outlook.

-

Optimize the Chikou line price comparison strategy with more stable solutions.

-

Incorporate stock selection signals. Scoring factors like PE ratio and ROE can filter lower quality stocks.

Conclusion

This is a very typical and practical moving average strategy. By simultaneously monitoring short, medium and long-term trends, utilizing various functions of moving averages, it generates trade signals with solid performance. We can further improve it by parameter tuning, adding stop loss, stock selection etc. Overall this is a promising quantitative strategy worthy of research and tracking.

- 1