Momentum Index ETF Trend Following Strategy

Overview

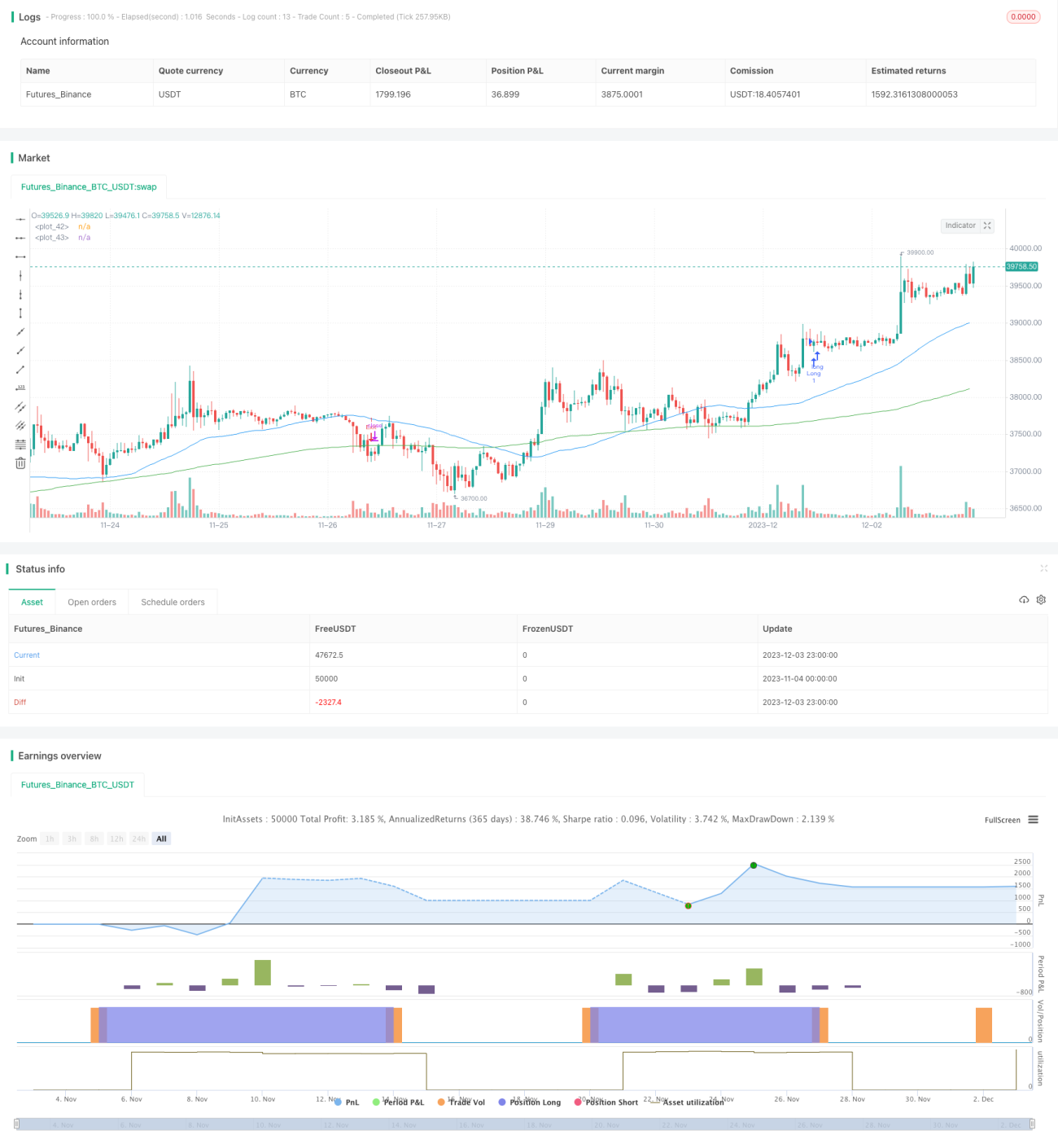

This is a momentum index ETF trend following strategy based on moving averages. It uses the crossover and slope of fast and slow moving averages to determine the trend direction for low-risk momentum trend following of index ETF assets.

Strategy Logic

The strategy uses 50-period and 150-period moving averages. When the fast moving average crosses over the slow moving average, and the slope of the fast moving average is greater than the threshold, it signals an upside trend reversal for long entry. When the fast moving average crosses below the slow moving average, or the slope of the fast moving average is less than the threshold, it signals a downside trend reversal for exiting positions.

The strategy simply utilizes the direction and slope of moving averages to determine market trend, avoiding overfitting and effectively controlling risks. Meanwhile, moving averages inherently have the ability to filter out market noise for robust signals.

Advantage Analysis

This is a low-risk momentum index ETF trend following strategy with the following advantages:

- Strong risk control ability. Moving averages filter market noise for effective risk control.

- Low implementation cost. Only simple moving averages are used, resulting in low cost and easy implementation.

- Stable profits. Index ETFs themselves have low volatility, combined with trend following, stable excess returns can be achieved.

- High adaptability. Many adjustable parameters allow optimizations for different index ETFs.

Risk Analysis

There are also some risks:

- Potentially missing quick reversals. Using moving averages to determine trends may miss out quick reversals.

- Parameter sensitive. Improper parameter settings may result in overtrading or missing opportunities.

- Performance dependence on market conditions. May underperform in choppy/sideway markets.

Solutions:

- Incorporate other indicators to determine quick reversals.

- Test and optimize parameters.

- Dynamically adjust parameters based on changing market conditions.

Optimization Directions

There are a few areas this strategy can be further optimized:

- Utilize other indicators like MACD, KD to complement the strategy.

- Incorporate stop loss logic to further control risks.

- Optimize moving average periods to adapt more index ETFs.

- Dynamically adjust parameters to suit different market environments.

Conclusion

In conclusion, this is a low-risk, easy-to-implement momentum index ETF trend following strategy. It determines trend directions using moving average crossovers and has advantages like strong risk control, low implementation cost and stable profits. Although some flaws exist, the strategy can be further improved in many aspects to become an effective tool for index ETF asset allocation.

- 1