Multi Moving Average Crossover Trading Strategy

Strategy Overview

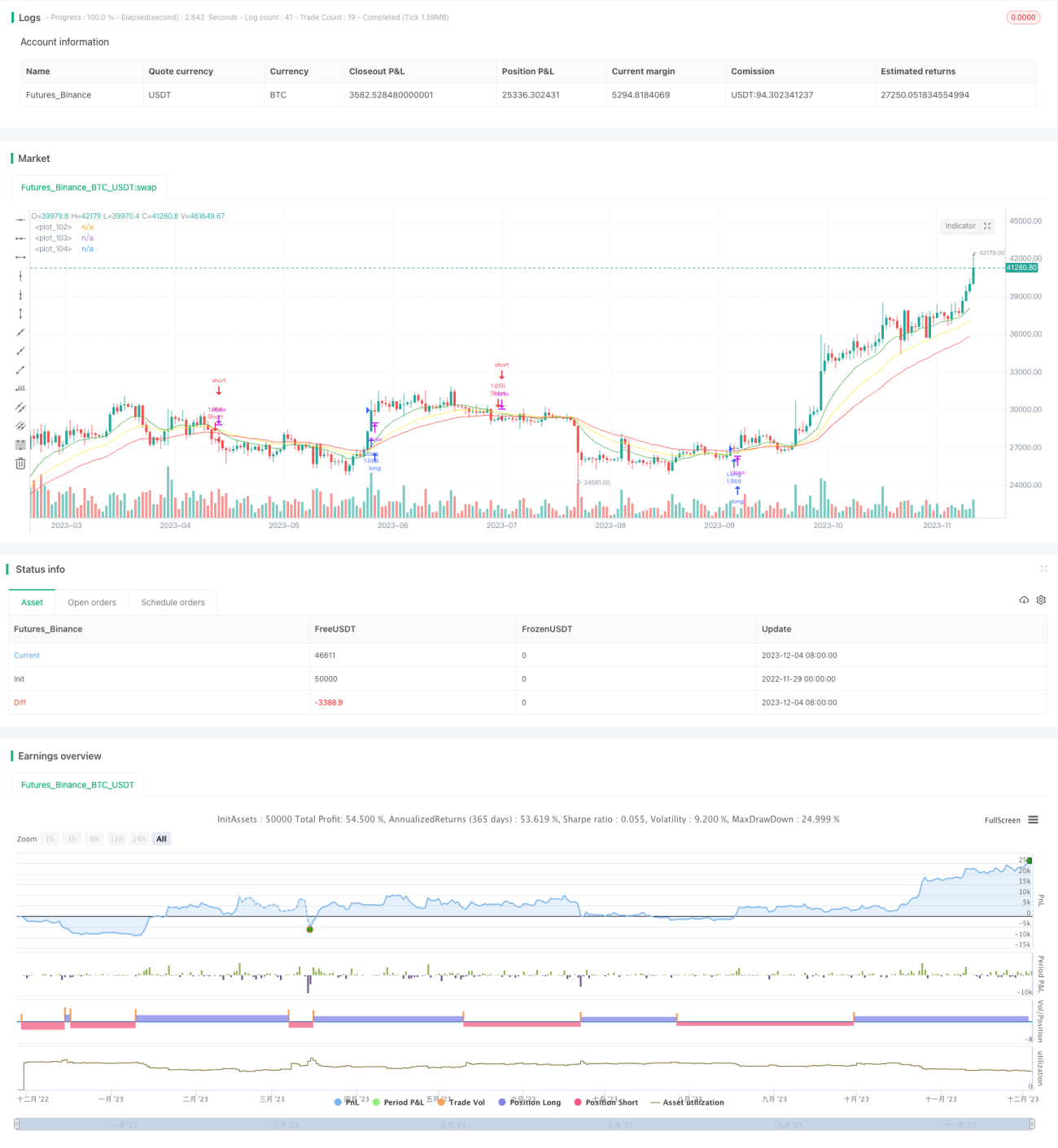

This strategy generates trading signals based on multiple moving average indicators. It monitors short-term, medium-term and long-term moving averages simultaneously, and generates trading signals according to their crossover situations to determine trend direction.

Strategy Name

Multi Moving Average Crossover Strategy

Strategy Logic

This strategy employs 3 moving averages with different periods, including 7-day, 13-day and 21-day lines. The trading logic is based on the following points:

- When the short-term 7-day MA crosses over the medium-term 13-day MA upwards, while the long-term 21-day MA is in an upward trend, a long signal is generated.

- When the short-term 7-day MA crosses below the medium-term 13-day MA downwards, while the long-term 21-day MA is in a downward trend, a short signal is generated.

By combining moving averages across different timeframes, the strategy can judge market trends more precisely and avoid false trades.

Advantages

- Using multiple MA lines can better determine market moves and avoid being misguided by false breakouts or short-term fluctuations in the market.

- Signals are only generated when the trend is clear, thus reducing unnecessary trades and lowering transaction costs.

- Flexible parameter settings - the periods of the MAs can be adjusted based on personal preference to suit different products and market environments.

Risks

- Frequent false signals may occur in a ranging, choppy market.

- MAs as trend-following indicators cannot accurately locate turning points.

- Delayed signal by MA crossovers may miss part of the profits.

- Risks can be reduced by introducing other technical indicators for signal validation and optimizing MA parameters.

Optimization Directions

- Consider incorporating volatility indicators to gauge trend strength and avoid trading in choppy markets.

- Try applying machine learning models to auto-optimize MA parameters.

- Add stop loss strategies to cut losses in time when drawdowns expand.

- Use limit orders when MA crossover happens to reduce slippage.

Conclusion

This strategy combines short-term, medium-term and long-term MAs to determine market trend based on their crossover relations, making it a relatively stable and efficient trend-following strategy. Further improvements in indicator parameters, stop loss mechanisms and order placement can help increase win rate and profitability.

- 1