Golden Ratio Mean Reversion Trend Trading Strategy

Overview

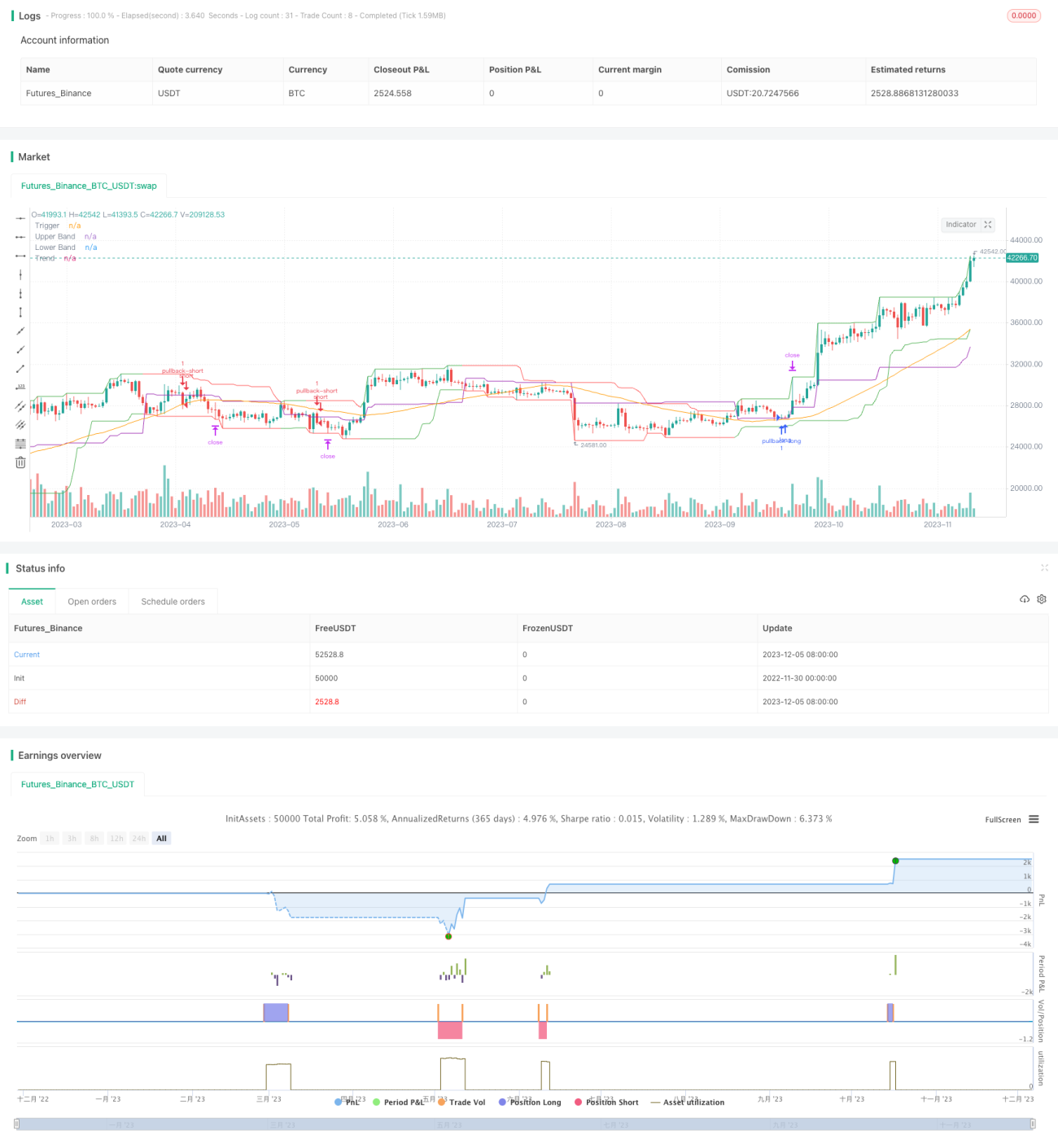

The golden ratio mean reversion trend trading strategy identifies stronger trend directions using channel indicators and moving averages, and opens positions in the trend direction after prices pullback to a certain ratio. This strategy is suitable for markets with stronger trend characteristics and can perform well in trending markets.

Strategy Logic

The core indicators of this strategy include channel indicators, moving averages and pullback trigger lines. Specifically:

- The channel indicator is calculated from highest high and lowest low to identify the price channel.

- The moving average is used to determine the overall trend direction of prices.

- The pullback trigger line then opens positions after prices bounce back from the channel boundary by a certain ratio.

When price touches the bottom of the channel, the strategy records the lowest point as a reference point and sets allow sell signal. When prices rise, once the rise reaches the pullback ratio, short positions will be opened around the rebound point.

Conversely, when price reaches the top of the channel, the strategy records the highest point as a reference point and sets allow buy signal. When prices fall, if the decline meets the pullback ratio requirement, long positions are opened around that point.

Therefore, the trading logic of this strategy is to track the price channel and intervene in the existing trend when reversal signals appear. This belongs to a common routine of mean reversion trend trading strategies.

Advantage Analysis

The main advantages of this strategy are:

- It can perform well in strong trending markets.

- The aggressiveness of entering trades can be adjusted through the pullback ratio parameter.

- Reasonable drawdown control can limit single trade loss.

Specifically, because the strategy mainly opens positions at trend reversal points, it works better in markets with larger price fluctuations and more obvious trends. In addition, adjusting the pullback ratio parameter can control the aggressiveness level of the strategy to follow trends. Finally, stop loss can control single trade loss very well.

Risk Analysis

The main risks of this strategy also include:

- The strategy is sensitive to the trend characteristics of the trading instruments.

- Improper pullback ratio settings may lead to over-aggressiveness or over-conservativeness.

- Position holding time may be too long, overnight risk needs attention.

Specifically, if the trading instrument used in the strategy has weaker trend and smaller fluctuation, the performance may be compromised. In addition, too large or too small pullback ratio will affect strategy performance. Finally, as the position holding time span of the strategy may be longer, overnight risk control also needs attention.

To avoid the above risks, consider optimizing the following aspects:

- Select trading instruments with more obvious trend characteristics.

- Adjust the pullback ratio parameter to find the best parameter combination.

- Set profit taking exits to reasonably control holding time.

Conclusion

The golden ratio mean reversion trend trading strategy judges price trends and pullback signals through simple indicators, opens positions to track trends in strong markets, and belongs to a typical trend system. This strategy has large parameter tuning space, can adapt to more market environments through optimization, and the risk control is also reasonable. Therefore, it is a strategy idea worth verifying and improving in live trading.

/*backtest

start: 2022-11-30 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//

// A port of the TradeStation EasyLanguage code for a mean-revision strategy described at

// http://traders.com/Documentation/FEEDbk_docs/2017/01/TradersTips.html- 1