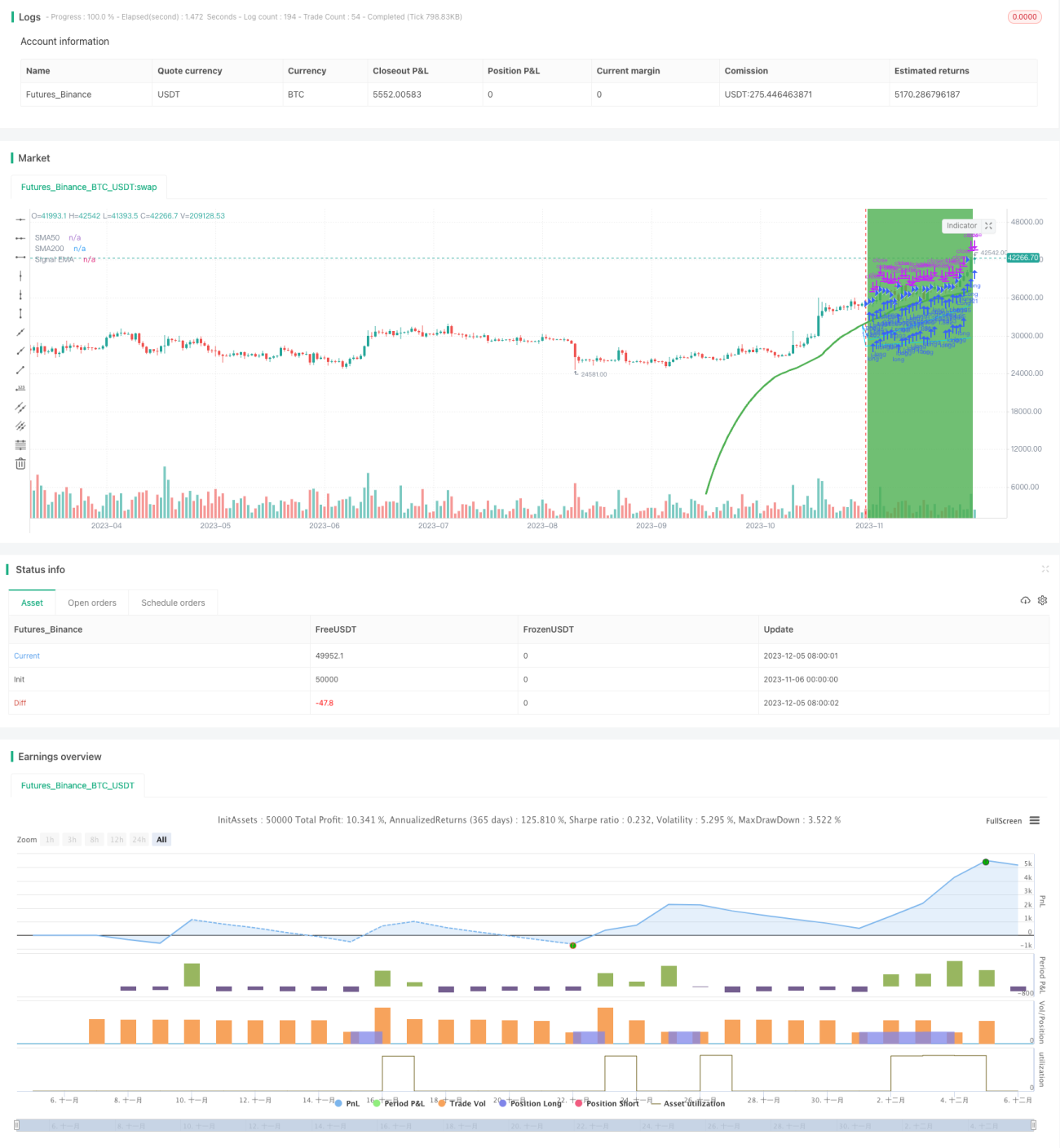

概述

本策略基于BTC的50日移动平均线和200日移动平均线的金叉死叉信号,结合额外的技术指标判断来发出买入和卖出信号。该策略主要适用于BTC/USDT这种具有明显趋势性特征的币对。

策略原理

当50日移动平均线上方突破200日移动平均线而形成“金叉”时,表示BTC进入多头市场,产生买入信号。而当50日移动平均向下突破200日移动平均线而形成“死叉”时,表示BTC进入空头市场,产生卖出信号。

该策略除了基本的移动平均线“金叉”和“死叉”信号判断以外,还加入了一些额外的技术指标来辅助判断,这些指标包括:

-

EMA指标:计算一个 length+offset 的 EMA 指标,当其上涨时表明目前处于多头市场,可以买入。

-

比较移动平均线与EMA的数值关系:如果EMA值高于50日移动平均线,则产生买入判断。

-

检查价格比上一根K线的低点下跌1%以上,如果满足则产生卖出信号。

通过组合运用上述几个指标,可以过滤掉一些错误信号,使策略交易决策更加可靠。

优势分析

该策略具有以下几个优势:

-

使用移动平均线作为主要交易信号,可过滤市场噪音,识别趋势方向。

-

结合EMA等多种辅助技术指标,可以增强信号的可靠性,过滤假信号。

-

采用适当的止损策略,可以有效控制单笔损失。

-

较为简单的交易逻辑,容易理解实现,适合量化交易初学者。

-

可配置参数较多,可以按照自己的偏好进行调整。

风险分析

该策略也存在一些风险需要注意:

-

移动平均线本身滞后性较强,可能错过价格快速反转的机会。

-

辅助指标增加了规则数量,也提高了产生错误信号的概率。

-

止损设置不当可能导致亏损扩大。

-

参数设置(如移动平均线长度等)不当也会影响策略效果。

对应解决方法:

-

适当缩短移动平均线周期,增大参数优化范围。

-

增加回测数据量,检查信号质量。

-

适当放宽止损幅度,同时设置盈利止盈。

-

增加参数优化,寻找最佳参数组合。

优化方向

该策略还可从以下几个方向进行优化:

-

增加机器学习算法,实现参数的自动优化。

-

加入更多辅助指标,构建多个子策略,通过投票机制产生决策。

-

尝试 Breakout 策略,识别价格突破。

-

利用深度学习预测价格趋势。

-

优化止损机制,实现动态跟踪止损。

以上优化可以提高决策的准确性,增强策略的盈利能力和稳定性。

总结

本策略主要基于BTC的移动平均线交叉进行交易决策,辅以EMA等技术指标来过滤信号。该策略具有较强的趋势跟踪能力,可配置性也较高,适合作为量化交易的入门策略。但也存在一定的滞后性风险,需要注意防范。接下来的优化方向可以从机器学习、集成策略、止损策略等多个层面进行。

/*backtest

start: 2023-11-06 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('JayJay BTC Signal', overlay=true, initial_capital=100, currency='USD', default_qty_value=100, default_qty_type=strategy.percent_of_equity, commission_value=0, calc_on_every_tick=true)

securityNoRepaint(sym, tf, src) => request.security(sym, tf, src[barstate.isrealtime ? 1 : 0])[barstate.isrealtime ? 0 : 1]- 1