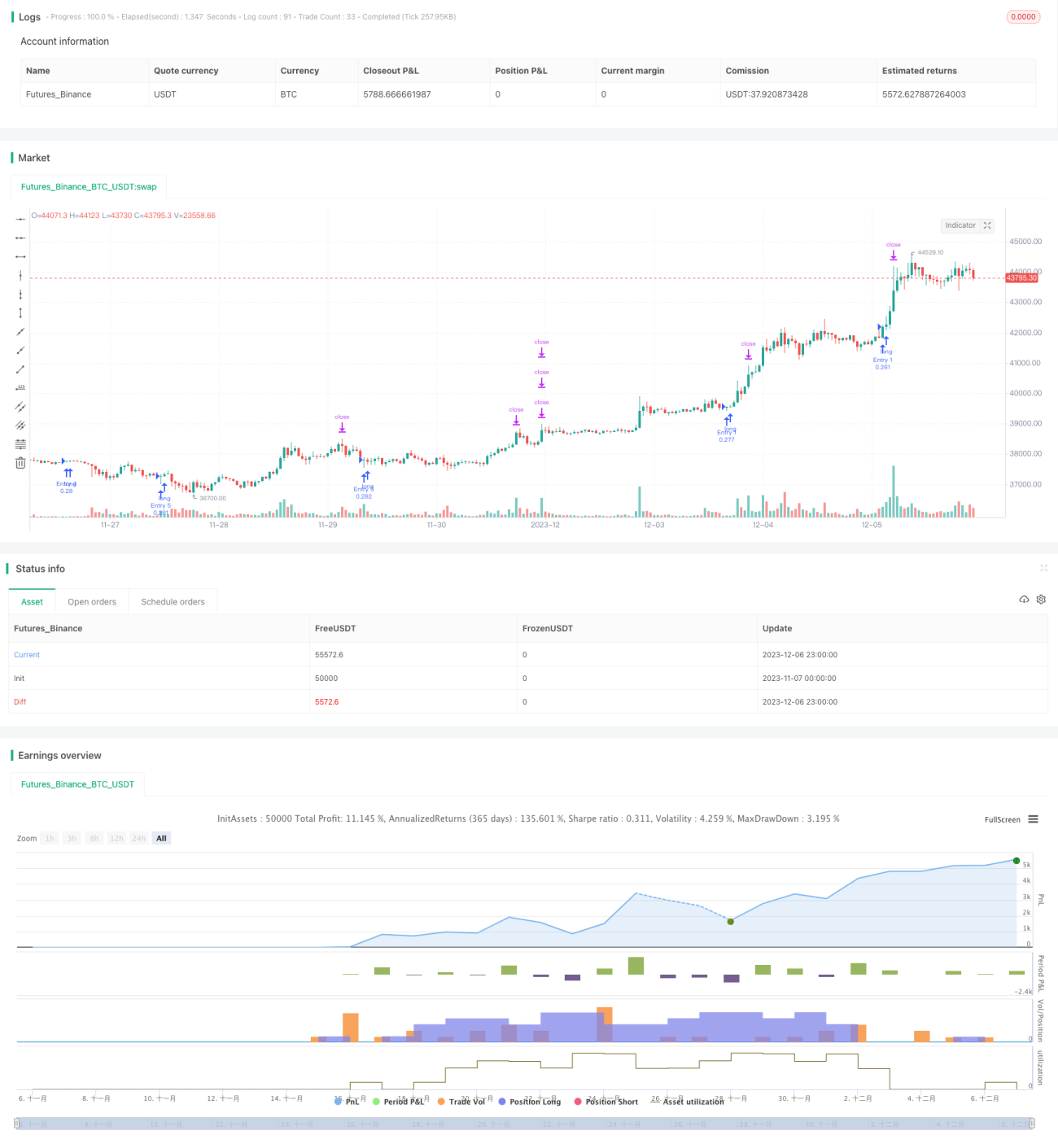

概述

该策略名为“OBV金字塔”,基于OBV指标设计开仓策略,并采用金字塔加仓方式,在趋势出现后,分批多次加仓,追踪趋势进行获利。

策略原理

该策略使用OBV指标判断趋势方向。OBV指标基于成交量变化判断价格趋势,成交量的变化反映市场参与者的态度。当OBV上穿0轴表示买盘力道增强,多头趋势形成;当OBV下穿0轴表示卖盘力道增强,空头趋势形成。

该策略通过判断OBV是否上穿0轴,来确认多头趋势的形成。在多头趋势形成时,设定金字塔式加仓规则,最多可加仓7次。通过追踪趋势进行获利,设置止盈止损退出机制。

优势分析

该策略最大优势是能捕捉趋势,通过金字塔加仓方式追踪趋势运行,获利潜力大。另外,策略风险控制到位,有止盈止损设置。

具体来说,优势主要体现在:

- 使用OBV判断趋势方向准确;

- 金字塔加仓方式能够追踪趋势获利;

- 设置止盈止损能控制风险;

- 策略逻辑简单清晰易于理解。

风险分析

该策略主要风险来自两方面:

- OBV判断失误,造成错失良机或错误建仓;

- 加仓过多,风险扩大。

对应解决方法:

- 优化OBV参数,确保判断准确;

- 适当控制加仓次数,确保风险可控。

优化方向

该策略主要可优化方向:

- OBV参数优化,提高判断准确率;

- 加仓次数和金额优化;

- 止盈止损点位优化;

- 结合其他指标判断,避免OBV单一判断风险。

优化这些内容后,可以使策略更稳定、更可控、更具备扩展性。

总结

该策略整体来说非常实用。它使用OBV指标判断趋势方向,然后通过金字塔加仓追踪趋势运行。策略逻辑简洁清晰,易于理解和回测。有一定的实战运用价值。通过对参数、止盈止损、加仓方式等的深入优化,策略效果能够得到进一步提升,值得进一步研究。

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1