Reversal Closing Price Breakout Strategy with Oscillating Stop Loss

Overview

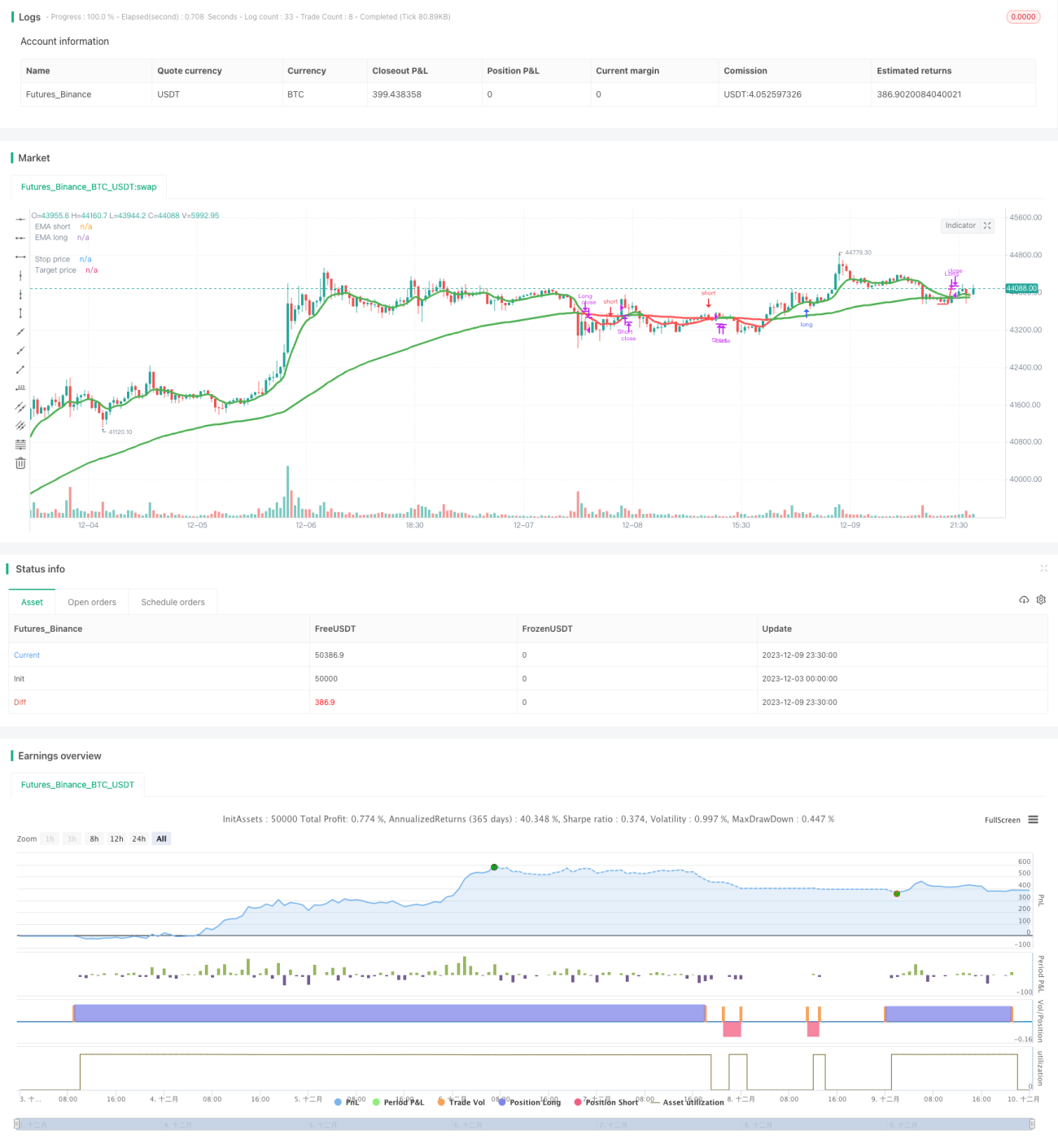

This strategy utilizes the price breakout signals and oscillating stop loss mechanism for risk management. It goes long when price breaks out the resistance and goes short when price breaks the support. At the same time, oscillating stop loss and profit taking stops are applied for better risk control.

Strategy Logic

The strategy is based on the following key points:

-

Using MA to determine the trend direction. Fast and slow MAs are plotted, fast MA crossing above slow MA signals bull trend, while crossing below signals bear trend.

-

Resistance breakout long signal. When price surges and breaks recent swing high, it is considered breaking resistance level, going long.

-

Support breakout short signal. When price drops and breaks recent swing low, it is considered breaking support level, going short.

-

Oscillating stop loss. After entry, stop loss line is set and keeps adjusting based on price fluctuation, forming an oscillating stop loss mechanism.

-

Stop loss and take profit exit. Stop loss exit controls risk, take profit lock in gains.

Specifically, it uses the average of high and low prices as the source, plots fast and slow EMAs to determine trends. When fast EMA goes above slow EMA and resistance breakout signal emerges, it goes long. When fast EMA drops below slow EMA and support breakout shows up, it goes short. After entry, the lowest price in certain periods is set as the stop loss line, keeps adjusting as price rises. Take profit line is plotted to lock in gains. The strategy effectively controls risk meanwhile profit from trends.

Advantage Analysis

The advantages of this strategy include:

-

Steady profitability. Following trends can make stable gains from long-term trends.

-

Excellent risk control. Oscillating stop and protective stop quickly cut losses.

-

Accurate signals. Resistance breakout long and support breakout short provide reliable signals.

-

Simple rules. Indicators and signals are straightforward, easy to follow.

-

Market adaptive. Works well across different products and market conditions.

Risk Analysis

Some risks to note for this strategy:

-

Breakout failure risk. Price may have throwback or pullback after initial breakout, triggering stop loss.

-

Parameter optimization risk. Bad parameter tuning leads to too many or too few signals. Optimization needs prudence.

-

Indicator failure risk. In extreme conditions, EMAs may stop working or lag behind price.

-

Trend reversal risk. Holding position against trend brings accumulating losses when trend reverses.

Proper parameter tuning, wide stop loss, strictly following rules can largely mitigate above risks.

Optimization Directions

The strategy can be further improved from the following aspects:

-

Timeframe optimization. Adjust calculation periods of MAs and price patterns, find best combinations.

-

Adaptability optimization. Tune parameters for different products.

-

Stop loss optimization. Test more advanced stop loss methods like trailing stop, Chandelier stop.

-

Take profit optimization. Adopt adaptive or exponential profit taking exits for better reward.

-

Add filters. Add volume, volatility filters to avoid false breakouts.

-

Enhance entry signals. Combine more indicators or patterns to confirm entries.

Conclusion

This is an effective breakout strategy with good risk control, stable profit model and straightforward logic flow. Fine-tuning and modular enhancement can make it more robust and adaptive to complex markets. It has great application potentials across more products.

- 1